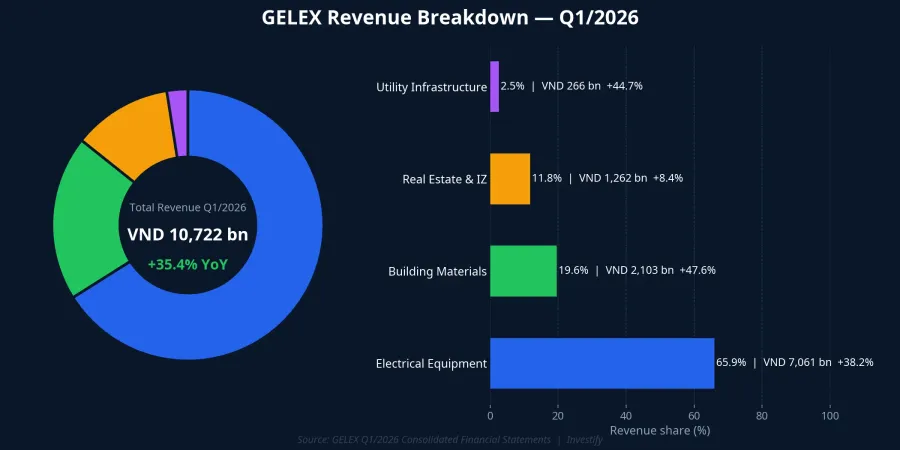

GELEX's consolidated Q1/2026 financials showed revenue of VND 10,722 billion (+35.4% YoY) and pre-tax profit (PBT) of VND 806 billion (+24.9%).Bao Phap Luat The more important number sits inside the structure: the electrical equipment segment contributed VND 7,061 billion, up 38.2% YoY and representing 65.9% of total revenue. A segment that accounts for nearly two-thirds of the company's top line, growing at 38.2%, is not a figure to skim past.

The market paid attention. On the morning of May 7, 2026, GEX (GELEX Corporation) closed at its daily ceiling price of VND 31,400 (+6.98%), while GEE (GELEX Electric) hit its ceiling at VND 122,000 (+6.83%), even as the VN-Index rose just 0.80%.Tin Nhanh Chung Khoan The spread between the GELEX group and the broader market exceeded 6 percentage points. This analysis asks: which specific numbers in the financial statements created that spread, and what variables should investors track next?

Electrical Equipment: The Segment That Defines the BCTC Narrative

Looking only at growth rates across segments, Q1/2026 seems balanced: building materials up 47.6%, utility infrastructure up 44.7%, real estate and industrial zones up 8.4%. But absolute scale is the key lens for reading GELEX.

The electrical equipment segment at VND 7,061 billion is 3.4x larger than building materials (VND 2,103 billion) and 5.6x larger than real estate and industrial zones (VND 1,262 billion).Bao Phap Luat At 65.9% of consolidated revenue, any acceleration or deceleration in this segment has a larger impact on consolidated profit than all three other segments combined. This is why any analysis of GELEX must begin here.

Against the 2026 full-year plan — VND 44,712 billion in consolidated revenue and VND 3,615 billion in PBT — Q1 completed approximately 24% of the revenue target and 22% of the profit target. That is a pace consistent with achieving the full-year plan, provided the electrical equipment segment sustains its momentum through subsequent quarters.

Who Is Driving Demand: EVN and the Transmission Grid Cycle

GELEX Electric (ticker: GEE) operates five major electrical equipment brands: CADIVI (power cables), THIBIDI (transformers), HEM (electric motors), EMIC (measurement equipment), and CFT (copper wire).The core customers for these brands are Vietnam Electricity (EVN) and its subsidiaries in transmission and distribution.

The 38.2% growth in electrical equipment was not driven by a short-term commodity price bounce. The underlying driver is the infrastructure investment cycle now opening up. Under Vietnam's revised Power Development Plan VIII, the 2025-2030 period requires total investment for power sources and transmission grids equivalent to approximately USD 136.3 billion, of which approximately USD 18.1 billion is allocated to transmission grids alone.Moi Truong & Thien Nhien The physical scope includes constructing 102,900 MVA and upgrading 23,250 MVA of 500 kV transformer capacity, 12,944 km of new 500 kV transmission lines, 105,565 MVA of new 220 kV transformer capacity, and 15,307 km of 220 kV lines.

The demand implications are specific. High-voltage transformer stations at 500 kV and 220 kV require large-capacity transformers, precisely THIBIDI's product segment. Thousands of kilometers of new high-voltage lines require power cables, precisely CADIVI's segment. When EVN and the National Power Transmission Corporation (EVNNPT) enter procurement contracting for the new phase, vendors with established manufacturing capacity, EVN-qualified product catalogs, and multi-year customer relationships will be first in line to absorb the order book.

Two caveats are worth noting. Demand for low-voltage cables from industrial zones and residential construction also contributes to CADIVI's growth. In March 2026, THIBIDI organized a cooperation workshop with the Electricite du Laos (EDL), adding an export channel.THIBIDI That said, based on available data, EVN procurement remains the decisive volume driver for large-capacity transformers and transmission cables.

GEX and GEE: Why Did Both Hit Ceiling on the Same Session?

Two stocks hitting ceiling on the same day can be explained from more than one angle. The most evidence-backed explanation is the Q1/2026 financials: with electrical equipment up 38.2%, investors repriced GEE's future cash flows, and with that came a repricing of GEX's stake in GEE. A second factor is the capital structure news: GELEX Electric's 2026 AGM approved a plan to raise charter capital from approximately VND 3,660 billion to over VND 6,404 billion through stock dividends and new issuances.Tap Chi Kinh Te Tai Chinh The broader GELEX ecosystem simultaneously announced capital-raising plans across subsidiaries following the AGM.Tap Chi Kinh Te Tai Chinh

The dilution impact from new share issuances appears to have been offset in market perception by the long-cycle growth expectations from the 2026-2030 grid cycle. Technical factors such as inflows following a consolidation period may have also played a role, though there is insufficient data to quantify this contribution. As of the May 7 morning session, GEX's market capitalization stood at approximately VND 28,300 billion. GEE carries a notably larger market cap than its parent GEX, reflecting the market's practice of pricing the electrical equipment business independently through GEE as a stand-alone listed entity.

Debt Structure: A Variable That Must Be Tracked in Parallel

The growth story in electrical equipment comes paired with a financial structure that deserves careful reading. As of March 31, 2026, GELEX's total debt was approximately VND 35,500 billion: VND 13,904 billion in short-term debt (+14.4% year-to-date) and VND 21,594 billion in long-term debt (+30.3%).Elibook/Dan Viet Finance costs in Q1 alone totaled VND 404 billion, equivalent to approximately 50% of PBT for the quarter. Part of the debt increase stems from GELEX's investment of approximately VND 8,000 billion in the Gia Binh Airport project, a long-duration infrastructure commitment outside the core electrical equipment business.Znews

This structure binds the electrical equipment growth thesis to two variables that must be monitored simultaneously. First, the actual pace of procurement contracting under the revised Power Development Plan VIII. The VND 18.1 billion transmission grid allocation only converts to real orders when EVN and EVNNPT execute specific EPC and equipment contracts. Second, GELEX's operating cash flows must be sufficient to service finance costs while funding the working capital that grows alongside rising electrical equipment revenue.

Signals to Watch Before the H1/2026 Results

The 38.2% growth in electrical equipment during Q1/2026 has a clear foundation: the power grid investment cycle is translating from plans on paper to real orders, and GELEX Electric holds the manufacturing capacity, qualified product catalogs, and customer relationships to capture a meaningful share of that demand. This is the most evidence-supported explanation for the pricing gap between the GELEX group and the broader market on May 7. The elevated debt structure and the non-core Gia Binh investment are real risks, but they are not sufficient to reverse the core thesis unless finance costs continue to escalate or EVN procurement disbursement slows significantly.

Three signals are worth tracking before the H1/2026 results are published around August: whether EVN orders in Q2 and Q3 sustain the Q1 pace; whether the finance cost-to-PBT ratio shows improvement as electrical equipment cash flows scale up, or remains near the 50% level; and how the Gia Binh investment registers in the group's investment cash flows for the remainder of the year.