On the morning of May 7, 2026, an investor holding Coteccons shares opened the trading board and saw two numbers moving in opposite directions. The VN-Index surpassed 1,909 points, a new all-time high, gaining 0.94% in the session.CafeF CTD, meanwhile, had been flashing red since midday, closing at its floor limit, down 6.93% to VND 80,600 and shedding VND 6,000 from the previous session. Matched volume hit 2.7 million units, three times the recent two-week average. The broader market was celebrating a milestone; CTD shareholders were counting losses. The real risk lies in a layer of information that sits outside the financial statements and has gone unread by most investors.

The Growth Foundation Is Real

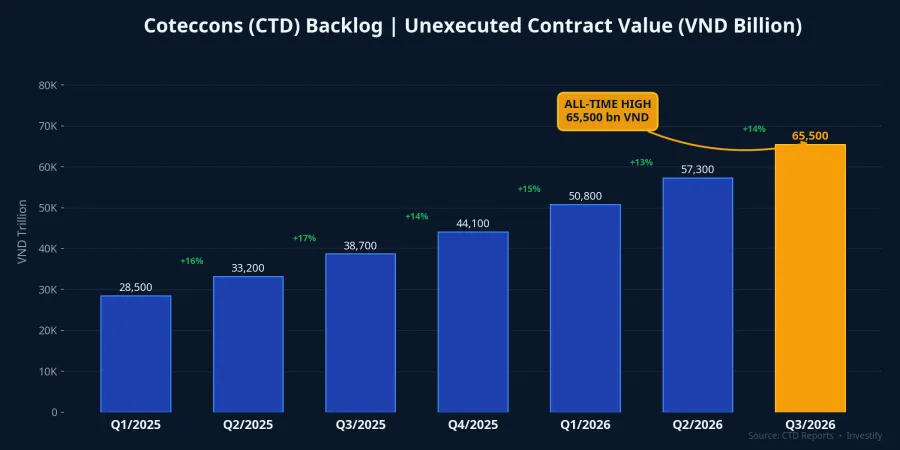

To understand why the market reacted so sharply, it helps to look at the stark contrast between the fundamentals and the price action. Coteccons had no shortage of good news that same week. The Q3 FY2026 report showed net revenue of VND 6,409 billion, up 28.12% year-on-year; after-tax profit reached VND 119 billion, more than double Q3 of the prior year.CafeF The backlog as of March 31, 2026 stood at approximately VND 65,500 billion (roughly USD 2.5 billion), an all-time high for the company.NguoiQuanSat

Coteccons was also named among Vietnamese contractors participating in the Hanoi–Quang Ninh high-speed railway construction package by VinSpeed, a project with total capital of approximately VND 147,000 billion (roughly USD 5.6 billion) that broke ground on April 12, 2026 with commercial operations targeted for 2028.NguoiQuanSat A record backlog and a position in Vingroup's largest infrastructure package are genuinely strong growth foundations. But May 7 showed that even those foundations cannot shield a stock price once the market realizes a layer of risk has been overlooked.

The Old Legal Layer: Still Unresolved

The first and longer-running dispute is the lawsuit between Coteccons and Ricons, two contractors that grew up inside the construction ecosystem built by former Chairman of Coteccons Board of Directors, Mr. Nguyen Ba Duong, before 2019. In October 2020, Mr. Duong left Coteccons following a control battle with foreign shareholder Kustocem, then built a competing ecosystem around Newtecons and Ricons to go head-to-head against his former company.NhaDauTu

VIAC Arbitration Award No. 279/23 HCM dated October 24, 2024 ordered Coteccons to pay Ricons approximately VND 170 billion, covering principal debt, late payment interest accruing from January 1, 2021 through September 24, 2024, legal fees, and arbitration costs.KinhTeChungKhoan The dispute traced back to construction contracts on the Regina projects in Hai Phong and Hung Yen, the VinFast plant, Simco, and Newtaco. All of these originated when the two sides still shared the same corporate roof. Coteccons filed to annul the award, but the application was rejected in May 2025 under Decision 84/2025/QD-PQTT.NguoiQuanSat On May 27, 2025, the Ho Chi Minh City Civil Enforcement Authority issued an order freezing VND 169,930,590,168 in a Coteccons account held at Techcombank's Sai Gon branch.CafeF The last line of resistance has closed: the funds sit in an account, no longer a contingent liability.

The New Legal Layer: Just Surfaced

What the annual report did not disclose is a second lawsuit. On May 5, 2026, Coteccons announced it had received Decision No. 1178/2026/QDST-KDTM dated April 21, 2026 from the District 5 People's Court in Ho Chi Minh City, recognizing an agreement between the parties in commercial case No. 1422/2024/TLST-KDTM, accepted on July 4, 2024.NguoiQuanSat The company has not identified the opposing party or disclosed the terms of the settlement.

Two details signal new risk. First, the gap between the court's ruling date (April 21) and Coteccons' disclosure (May 5) is two weeks, unusually long for a document that qualifies as material non-routine disclosure. Second, the case had been accepted by the court since July 2024, meaning it ran in parallel with the Ricons dispute for nearly two years without ever appearing in annual reports or prospectus filings. When information is opaque, markets tend to price for the worst case.

Why VND 170 Billion Hits Harder Than VND 170 Billion

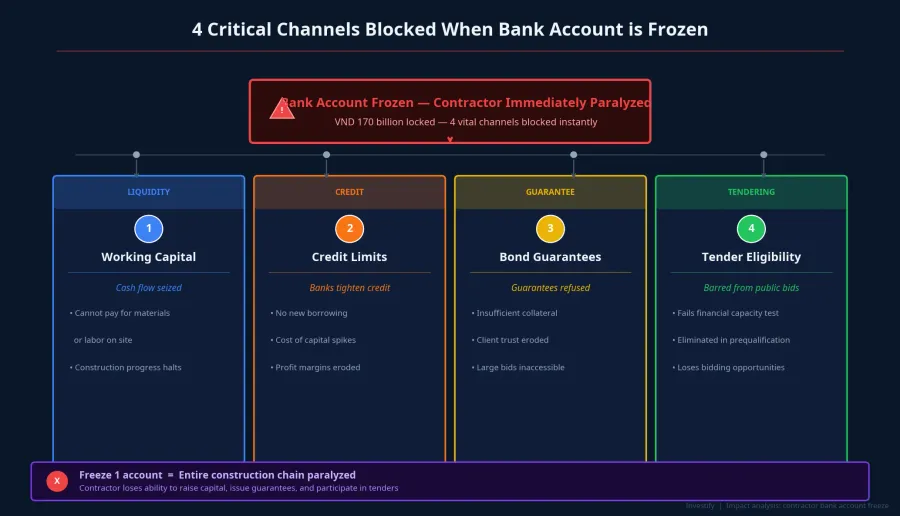

A reasonable question arises: does VND 170 billion really justify a floor-limit drop against half-year revenues approaching VND 12,000 billion? This is where many investors misread the impact of an account freeze. The damage is not in the absolute figure: it is in four operational channels blocked simultaneously.

Working capital locked. Construction contractors operate on large cash flows: paying for materials, subcontractors, and site labor before receiving progress payments from project owners. The VND 170 billion sitting in that account is not idle cash; it is liquidity earmarked for near-term obligations. Freezing it is equivalent to cutting off part of the blood supply in the same week.

Bank credit limits tightened. The freeze order enters the credit file. Banks reassess risk upward, and new or expanded credit lines come under review. For a company carrying approximately VND 65,500 billion in backlog, every basis point added to the cost of capital erodes profit margins that are already thin in the construction sector.

Contract performance guarantees become costlier. Project owners typically require performance bonds covering 5–10% of the contract value. A contractor with active legal disputes may face higher bond premiums or difficulty securing guarantees for large packages — at precisely the moment it needs a clean guarantee profile for the high-speed railway contract.

Public tender eligibility at risk. Many government procurement packages include prequalification conditions around active legal disputes. Two overlapping cases turn the legal profile into a variable that bid evaluation committees must weigh, in a period when Coteccons needs the cleanest possible record to compete for major infrastructure tenders.

Reading the Legal File Like the Financial File

Construction stocks carry a specific appeal: the backlog is a visible forward revenue indicator, and large contracts create a sense of certainty. But May 7 highlighted a sector-specific dynamic that newer investors often overlook: disputes from construction contracts can surface years after a project is complete, and when they do, they hit working capital, financing costs, guarantee capacity, and tender eligibility in a single blow.

Several checks investors can run before taking a position in construction stocks. Read the "pending litigation" section in financial statement notes and annual reports carefully, not just the earnings summary. Monitor material disclosure announcements on HOSE for court or arbitration decisions, which often appear before they reach periodic reports. Examine leadership transition history: control battles tend to leave legal legacies that linger for years. For contractors specifically, cross-referencing related parties who share a personnel or shareholder origin is a useful screening step, since disputes are most likely to arise from legacy relationships.

Coteccons' approximately VND 65,500 billion backlog and its position in the high-speed railway tender remain genuine growth foundations. The floor-limit session on May 7 does not erase that. What it does reinforce is a basic principle: for construction stocks, the legal file must be read alongside the financial file with equal weight. Two signals worth monitoring from here: whether Coteccons discloses further details about the counterparty and substance of the July 2024 lawsuit, and the actual enforcement progress on the VND 169.9 billion account freeze order.