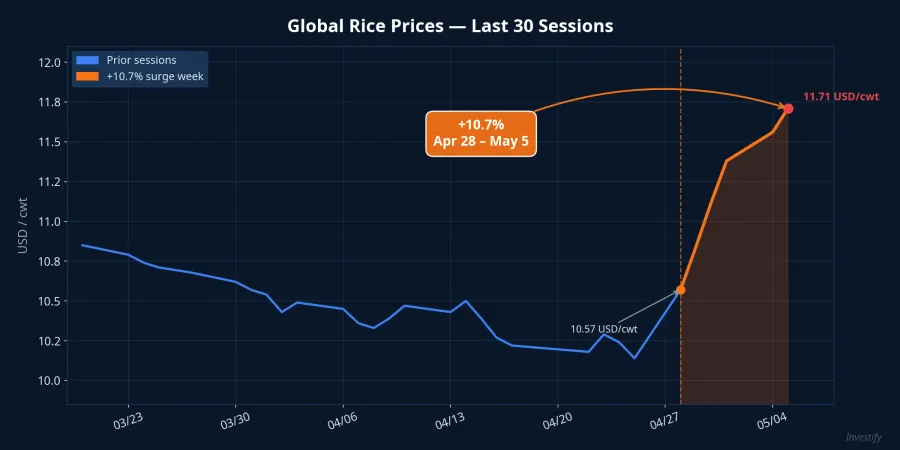

Between April 28 and May 5, 2026, global rice prices climbed from USD 10.57 to USD 11.71 per hundredweight — a gain of 10.7% in just five trading sessions. For a food commodity that typically moves slowly, that kind of amplitude in a single week is unusual. Over the same window, Brent crude traced an opposing arc: it rallied sharply on two consecutive sessions (both gaining over 5% as Hormuz tensions escalated), then fell 4.0% to USD 109.87 per barrel on May 5 after the U.S. confirmed that the Iran ceasefire remained in place, and continued declining to USD 108.78 on May 6.

These two moves are not independent. Ocean freight costs — one of three forces that pushed rice prices higher — track fuel costs directly, and that force is now reversing alongside oil. Understanding what this means for Vietnamese rice export stocks requires the full picture.

Three Forces That Converged in One Week

Freight rates followed oil prices. When Brent rallied sharply mid-week on Hormuz fears, shipping rates for rice from the Mekong Delta to the Philippines and Indonesia moved higher with a lag of a few days. Import buyers responded by front-loading purchases, driving CIF prices up. This is an exogenous force from the Middle East — and it is now reversing as ceasefire news holds.

Mekong Delta supply tightened after the winter-spring harvest. The Vietnam Food Association reported that traders began buying dry high-quality paddy as the short-cycle fresh-paddy supply wound down.VFA This is a recurring seasonal cycle that will persist until the summer-autumn harvest comes in. On its own it does not cause sharp price swings, but when it aligns with a pick-up in import demand, it amplifies the move.

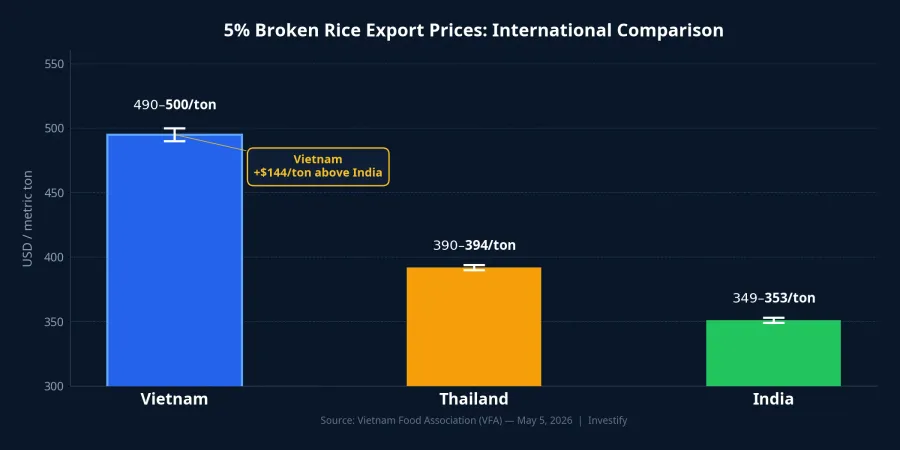

India holds the pricing role. According to the Vietnam Food Association's 2025–2026 crop-year report, India has shifted from "volume regulator" to "price setter" on the global rice market on the back of record-high output.VFA This past week, India's 5% broken rice was offered at USD 349–353 per tonne, up slightly on the week. Any adjustment in New Delhi's export policy creates an immediate and outsized move in world prices, making this the most unpredictable of the three forces.

The three forces do not carry equal weight. The freight-cost force is exogenous and reversing. The Mekong Delta supply cycle will persist a few more weeks. The India policy variable has no visible direction. That combination is exactly why this is a crossroads, not a confirmed trend.

The Divergence Story From Q1/2026

In Q1/2026, Vietnam exported approximately 2.3 million tonnes of rice at a total value of USD 1.11 billion: volume was essentially flat (+0.2% year-on-year), but export value fell 7.8% and the average price declined 8% to approximately USD 480 per tonne.Xaluan This is not the picture of an industry fully capturing the benefit of rising global prices.

The reason lies in how margin is distributed across the Mekong Delta rice value chain. When global prices spike sharply over a few weeks, most of the incremental margin accrues to traders and export companies — the parties that sign FOB and CIF contracts directly with foreign buyers. Farmers sell fresh paddy at the farm gate at prices agreed a few weeks before harvest; they have no storage capacity to wait for better prices. Export companies, meanwhile, face the opposite pressure: the cost of buying dry paddy at the end of the season rises in step with world prices, compressing gross margin.

Lộc Trời (LTG) is the textbook illustration. In Q1/2024, the rice business contributed approximately 85% of revenue but carried a gross margin below 3%, resulting in a net loss of nearly VND 100 billion even as revenue grew 57%, while borrowings accounted for 53% of total capital at the time.Thi Truong Tai Chinh These are Q1/2024 historical figures, but they illustrate a structural trap LTG has yet to escape: high revenue, thin margin, heavy leverage. Today, LTG trades around VND 6,400 per share with almost zero liquidity; many sessions end with no matched orders.

Vietnam's USD 140/Tonne Premium: Will It Hold?

Vietnam's 5% broken rice is currently offered at USD 490–500 per tonne, roughly USD 140 higher than India and USD 100 higher than Thailand.VFA That premium reflects partly quality differentiation — especially aromatic varieties like Jasmine and ST25 — and partly different target market positioning. The USD 140 gap is also a competitive vulnerability if India continues expanding its export volume.

PAN Group stands apart within the rice stock universe. On May 6, PAN traded at VND 32,400 per share, up 2.37% on the session and approximately 15.7% above the VND 28,000 level seen at end-March. Its rice exposure runs through Vinaseed, which is just one of several business segments (seafood, agri-products, consumer goods), giving PAN better diversification against single-commodity swings, though that same diversification dilutes the upside when rice prices rally. Trung An (TAR) at around VND 3,200 and Angimex (AGM) near VND 2,000 both reflect a market that has little conviction in the rice story at this juncture.

Three Scenarios Ahead

Scenario A: Middle East re-escalation. If Iran takes new escalatory action within the next four to six weeks and Brent rebounds above USD 115 per barrel, global rice prices could hold the USD 11–12 per cwt range. However, export margins would continue to be pressured by rising freight and fertilizer input costs. High revenue alongside thin gross margin is a pattern LTG has already experienced; with current leverage levels, this is not a favorable outcome.

Scenario B: Sustained Middle East de-escalation. This is the scenario implied by the price action in the two most recent sessions. The ceasefire holds, Brent drifts toward USD 95–100 in Q2, and freight rates ease. Global rice prices settle back toward a new equilibrium around USD 10.5–11.0 per cwt. Competition shifts back to product quality and niche market share. Integrated players like PAN benefit on a relative basis; pure-trading operators like TAR and AGM face more margin compression.

Scenario C: India changes its export policy. This is the variable with the largest potential impact and the least visibility. If New Delhi tightens exports through tariffs or floor pricing, Vietnamese rice export stocks could rally sharply in one or two sessions — but sustained gains depend on each company's ability to lock in Q3 contracts at elevated prices. If New Delhi instead opens the tap further, the USD 140/tonne spread between Vietnam and India narrows materially.

Based on the last two sessions' price behavior, Scenario B currently carries the highest probability for Q2. But both A and C can materialize within weeks; that is precisely what makes this a crossroads rather than a settled trend.

Three Signals to Watch

The big picture: last week's rice price rally was a combination of three forces moving in different directions and on different timescales. Scenario B leads in probability, but A and C remain live. A limited position in rice export stocks is appropriate while these signals resolve.

First, India's rice export policy over the next four to eight weeks: any move to impose duties, set floor prices, or broaden export licenses would have the largest and most immediate price impact.

Second, ocean freight rates from the Mekong Delta to the Philippines, Indonesia, and Africa: the fastest leading indicator for both price direction and company margins. Freight declining alongside oil confirms Scenario B; freight rebounding signals Scenario A.

Third, Q2 export contract volumes for LTG, PAN, and TAR: these will surface in June management reports and half-year financial statements. Long-term contracts signed at elevated prices are the condition that lets the value chain actually retain margin rather than just report revenue.

These three signals are the conditions to watch before drawing conclusions about the direction of this market.