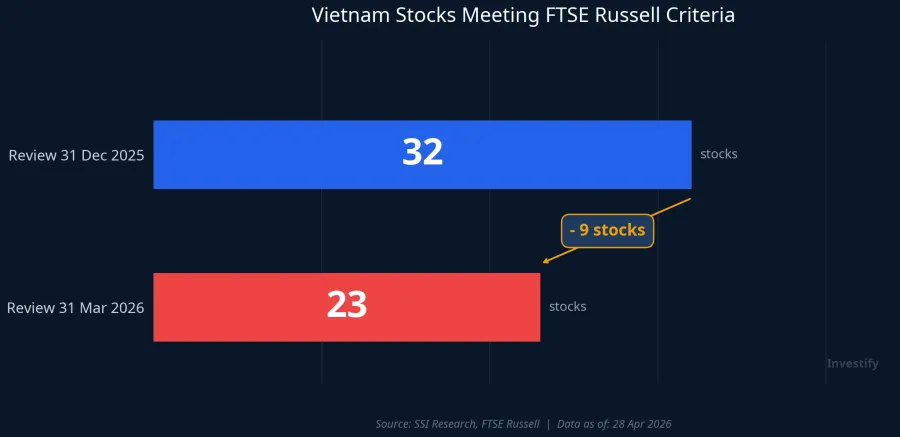

The FTSE Russell review of March 31, 2026 data has narrowed Vietnam's eligible stock list from 32 to 23 names. Nine stocks were removed, including SAB, DIG, and DXG. Critically, none of them were removed because their business performance deteriorated or their risk profile worsened. They were cut because they no longer met the technical eligibility criteria FTSE Russell applies to emerging market constituents.TạpchíKT&TC

This distinction matters more than it might seem. Investors accustomed to reading company news can easily confuse index signals with business signals. This article breaks down the four technical criteria FTSE uses in its screening, the specific reasons each group of removed stocks failed, the mechanics of passive ETF rebalancing, and a pervasive misconception about FUEVFVND and E1VFVN30.

The Four Technical Criteria FTSE Russell Applies

FTSE Russell screens stocks against four technical conditions to determine eligibility. This is a periodic filter applied uniformly across all emerging markets. Company earnings play no role.

The first criterion is free-float adjusted market capitalisation. FTSE counts only the portion of shares freely available for trading in the market. Stakes locked up by large shareholders or state entities are excluded from the calculation. The second criterion is liquidity, measured by average monthly and quarterly trading value. The threshold is calibrated to the size of the market in question. The third criterion is foreign investor accessibility: remaining foreign ownership headroom (known as "room"), or an equivalent access mechanism such as NVDR (non-voting depositary receipts, common in Thailand). The fourth criterion is data continuity: stable, uninterrupted trading records that passive funds can reliably replicate without gaps.

These four screens operate entirely independently of a company's earnings, debt level, or strategic direction. A stock can report 40% profit growth one quarter and still be removed from the index if foreign ownership headroom runs out. Conversely, a company navigating a difficult cycle can remain in the index as long as its free-float cap and liquidity hold up.

Why SAB, DIG, and DXG Were Removed

Each of the three headline removals failed on a different criterion.

SAB was removed on the foreign ownership criterion. The foreign ownership share in Sabeco has reached its ceiling, leaving no room for additional foreign purchases. FTSE treats this as a practical barrier to access: even though the stock is publicly listed, foreign investors wanting to build a position to match index weights cannot do so. If Sabeco establishes an NVDR mechanism or expands its foreign ownership limit, the eligibility picture could change at the next review.

DIG was removed on liquidity. Average daily trading volume in DIG has dropped significantly from its 2022–2023 levels, falling below FTSE's minimum quarterly trading threshold. This is a direct consequence of the prolonged slowdown in the real estate sector and tightened credit conditions, which drained market-side participation from the group.

DXG was removed because its free-float adjusted market capitalisation slipped below the minimum threshold FTSE requires for emerging market membership. A prolonged decline in share price, combined with a relatively small free-float, can push effective market cap below the floor even when the underlying business remains operational.TạpchíKT&TC

The 23 Remaining Stocks and Estimated Inflows

The 23 stocks that passed the review are: VIC, HPG, VHM, FPT, MSN, SSI, VNM, STB, VCB, VJC, VRE, VIX, NVL, VCI, SHB, GEX, VND, KBC, KDH, BID, DGC, BSR, and GEE.

SSI Research estimates total passive inflows into these 23 names at approximately USD 1.3 billion from September 2026 to September 2027, as Vietnam's weighting in FTSE indices is phased in over that period. This is not a one-off inflow: FTSE-tracking funds will increase their Vietnam allocation in steps across the 12-month schedule.Kevesko

Within the 23 names, VIC is expected to receive approximately USD 498 million and HPG approximately USD 115 million. The remainder is distributed by free-float adjusted weight. It is worth noting that Vietnam's overall weighting in FTSE indices has been revised downward following this review: FTSE Emerging All Cap moved from 0.350% to 0.329%, FTSE All-World from 0.024% to 0.020%, and FTSE Emerging from 0.227% to 0.192%.Kevesko The lower weights reflect the smaller number of eligible Vietnamese stocks and the corresponding reduction in total adjusted market cap.

How Passive ETF Rebalancing Works

An index-tracking ETF is a passive vehicle: its entire portfolio mirrors the composition and weights published by the index provider, in this case FTSE Russell. When FTSE removes a stock, the fund has no discretion to hold it regardless of how attractive the valuation appears. When FTSE adds a stock, the fund must buy it regardless of how far prices have already run.

This creates a structurally different kind of buying and selling pressure from active trading. Three characteristics define it. First, the size is estimable in advance because flows scale with the total assets of FTSE-tracking funds and the weight assigned to each stock. Second, the timing is fixed around the rebalance date, not spread gradually the way active trading flows tend to be. Third, passive funds do not adjust for valuation. An active manager can stop selling when a price gets cheap enough; a passive fund must complete the trade to maintain its tracking.

For the nine removed stocks, selling pressure from international FTSE-tracking funds is expected to concentrate around September 21, 2026. The actual magnitude depends on each stock's previous weight in the index and the total assets under management of funds tracking FTSE Vietnam and broader FTSE Emerging Markets indices. Markets typically begin pricing this in during the sessions leading up to the effective date.

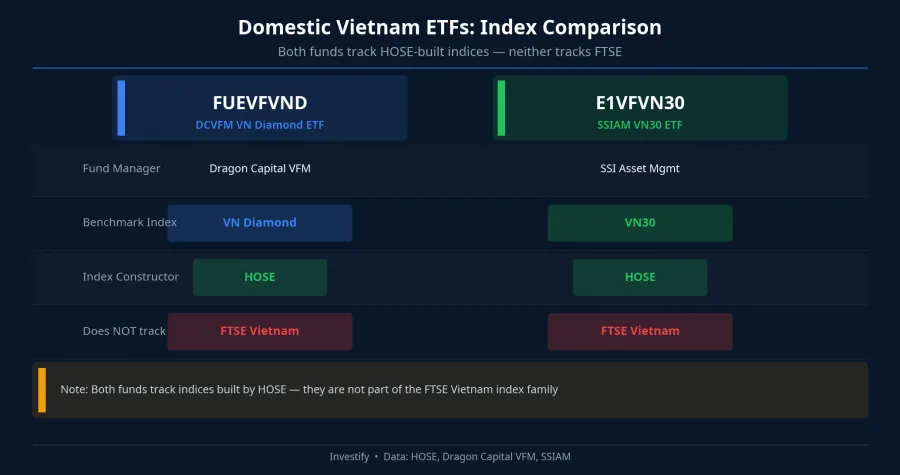

FUEVFVND and E1VFVN30 Do Not Track FTSE

This is the most common misconception surrounding Vietnam's FTSE upgrade. FUEVFVND, managed by Dragon Capital, tracks the VN Diamond Index, which is constructed by HOSE.Vietstock E1VFVN30 tracks the VN30, also a HOSE-built index.Vietstock Both indices were constructed by the Vietnamese exchange using their own selection criteria, with no connection to the FTSE Russell eligibility framework.

The practical implication: the September 2026 upgrade does not directly alter the portfolio of either fund. SAB falling off the FTSE list does not trigger FUEVFVND to sell SAB, because SAB is not a VN Diamond constituent under VN Diamond criteria. The USD 1.3 billion in expected passive inflows moves through international FTSE-tracking vehicles such as the Xtrackers FTSE Vietnam Index ETF and the global FTSE Emerging Markets funds that carry a Vietnam allocation.

Vietnamese retail investors holding FUEVFVND or E1VFVN30 can benefit indirectly, through market price appreciation of stocks that overlap between their fund's portfolio and the FTSE-eligible 23. But there is no direct rebalancing mechanism from FTSE. The word "ETF" describes a legal fund structure, not the index being tracked. The benchmark prospectus determines what the fund actually follows.

Timeline and What to Monitor

Three milestones matter between now and the upgrade:

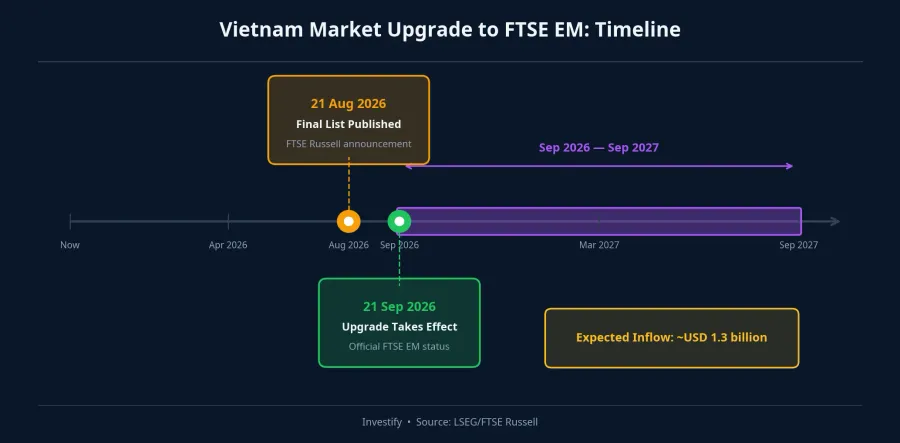

By August 21, 2026, FTSE Russell will publish the final list of Vietnamese stocks that will be included in its indices. Between now and that date, the current list of 23 can still shift if a stock's liquidity or foreign ownership headroom changes materially enough to affect the next review's data cut. This publication date is the critical checkpoint, not the effective date.

September 21, 2026 is the effective date of the upgrade. FTSE-tracking passive funds execute their portfolio rebalances according to the phase-in schedule. Buying pressure concentrates on the 23 remaining stocks; selling pressure concentrates on the nine removed stocks. Markets typically begin reflecting this dynamic in the sessions surrounding the date.

From September 2026 through September 2027, approximately USD 1.3 billion in passive inflows is expected to enter in stages as Vietnam's FTSE weighting is phased in.

For investors currently holding domestic ETF certificates, three things are worth verifying before August 21: the benchmark index of the fund you hold (FTSE Vietnam, VN Diamond, VN30, or another), the degree of overlap between your fund's current portfolio and the 23 FTSE-eligible stocks (which indicates the level of indirect benefit), and whether any names in your portfolio fall among the nine removed stocks and may face selling pressure around September 21.

Passive inflows from FTSE represent a fixed, time-bounded layer of demand. They do not reverse the fundamental story of a business, and they are one variable in a broader valuation picture. A stock's inclusion in an index does not automatically make it a good investment; removal from an index does not automatically make it a bad one. Understanding the mechanics clearly allows investors to separate index signals from business signals, and avoid acting on the wrong one.

The next signals to monitor: changes in liquidity or foreign ownership headroom for stocks in the current 23-name list before the next review cut, and August 21, 2026 when FTSE finalises the definitive list.