On the night of May 5 (US time), two earnings reports released after the close of New York markets drew significant attention from technology analysts. AMD posted revenue of $10.3 billion, up 38% year over year. Super Micro Computer — the largest AI server assembler in the United States — hit $10.24 billion, up 123%. These companies operate at two different points in the AI hardware supply chain, yet both reported beats in the same session. That alignment is not a coincidence: they are measuring the same phenomenon from opposite ends.

The Bear Case and Its Three Arguments

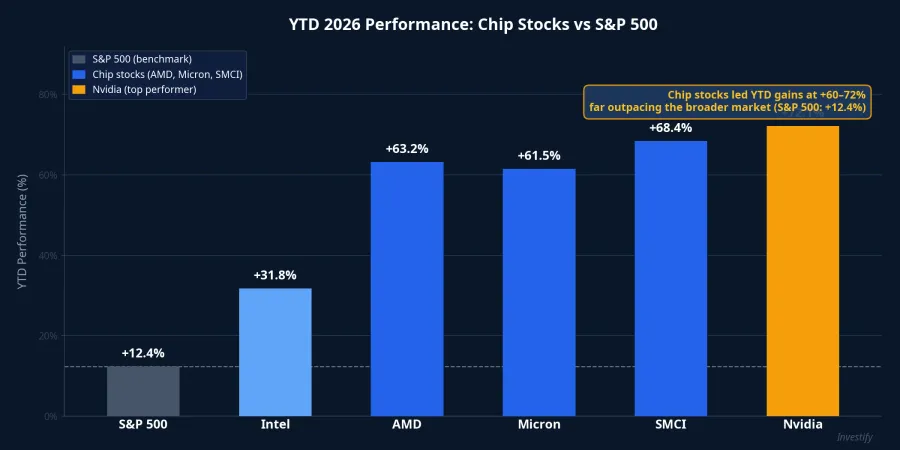

Since the start of 2026, US semiconductor stocks had rallied 60–72%, far outpacing the S&P 500's 12.4% gain. That multiple expansion created pressure: if Q1 results fell short, the correction would come quickly.

The bear case rested on three arguments. First, AI capital expenditure by the hyperscalers had peaked and could not sustain its trajectory. Second, the HBM memory cycle was due to tip into oversupply as Samsung and SK Hynix ramped output. Third, AMD's Instinct MI300X GPU had not secured large-scale contracts with top-tier hyperscalers. The Q1/2026 reporting season became a direct test of all three claims.

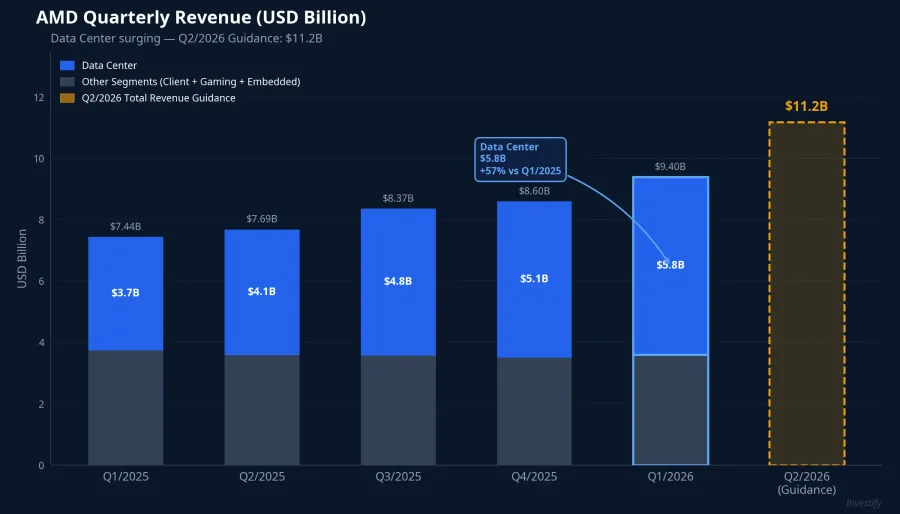

AMD Q1/2026: Data Center Crosses $5.8 Billion

The numbers from AMD speak for themselves: Q1/2026 revenue came in at $10.3 billion, up 38% year over year, beating the Street's estimate of $9.84 billion.CNBC Net income nearly doubled to approximately $1.4 billion. AMD shares jumped 12% in after-hours trading.

The more significant figure was in the data center segment: $5.8 billion, up 57% year over year, and for the first time accounting for more than half of the company's total revenue. This is the clearest indicator that AMD is no longer primarily a PC and gaming chip company. The AI segment has become its main growth engine.

Lisa Su, Chair and CEO of Advanced Micro Devices (AMD), said the company has "strong and growing confidence" that AI data center revenue will reach "tens of billions of dollars in the coming year," exceeding its long-term growth target of 80% annually.

Even more notable was the Q2/2026 guidance: AMD projected revenue of approximately $11.2 billion, plus or minus $300 million, representing roughly 46% growth year over year.CNBC Against an already high comparison base, that acceleration tells two stories. AI GPU orders did not cool heading into Q2. And the 6-gigawatt MI450 supply agreement with Meta — announced in February 2026 and estimated at $60–100 billion over five years — has begun flowing into the order book, even though the first deliveries are scheduled for the second half of 2026.MarketMinute Combined with the OpenAI agreement signed in October 2025 and MI300X's presence on Oracle Cloud Infrastructure, AMD now has at least three confirmed hyperscale customers on the books, directly rebutting the claim that the MI300X "had no clear customers."

Super Micro Computer: 123% Growth as Independent Confirmation

Super Micro Computer does not make GPUs. The company assembles AMD and Nvidia GPUs into complete rack-scale systems and delivers them to customers. That role makes SMCI's revenue an independent measuring stick: when servers ship, GPUs have been deployed to real customers. They are not sitting in inventory.

SMCI reported quarterly revenue of $10.24 billion, up 123% year over year.CNBC Adjusted EPS came in at $0.84, beating the $0.62 estimate by roughly 35%. The stock rallied 18% after guidance for the next quarter also topped Wall Street expectations. The logic is simple: if hyperscalers were only signing contracts without taking delivery, SMCI's revenue could not reach this level.

A reasonable concern remains: server assembler gross margins are typically thin, and rapid growth can compress them through price competition. SMCI faced pressure following accounting issues in 2024. This time, management emphasized that the high mix of GPU-intensive products is keeping margins stable. That is a point worth monitoring in coming quarters. It is not a concern that has been fully resolved.

Micron and Intel: Corroborating Signals from the Supply Chain

Also during the same week, Micron Technology reinforced the message that its entire 2026 HBM (high-bandwidth memory) output has been pre-sold under multi-year supply contracts running three to five years.Seeking Alpha Micron guided for gross margins of 68% and EPS of $8.42, both record levels for the company. This is the most critical data point against the memory cycle bear thesis: if long-term contracts hold, part of the traditional DRAM cycle's volatility is being structurally eliminated rather than temporarily suppressed.

On the same day, reports that Apple was in discussions to use Intel and Samsung foundries to produce iPhone chips in the United States pushed Intel's stock up an additional 10%.MacRumors This adds evidence for a separate argument: server CPUs are not being replaced by AI GPUs. Both hardware layers are being deployed in parallel inside the new generation of rack-scale systems, demonstrating that the "AI era" is not a single-chip story.

What This Means for Vietnamese Investors

Vietnamese retail investors now have growing access to US equities through brokers that offer international trading services, as well as through sector-specific technology ETFs listed in the United States. The data from May 5 does not provide a buy or sell signal for any specific ticker. What it provides is a more useful analytical framework.

First, when asking whether AI is generating real revenue, the most relevant data comes from hardware suppliers' financials, not the valuation multiples of the hyperscalers themselves. A hyperscaler can sustain capital expenditure from free cash flow without proportionate AI revenue; the ROI concern the bears raise is still valid. But the hardware those hyperscalers are purchasing has converted into real revenue at AMD, SMCI, Micron, Nvidia, and TSMC.

Second, two different questions need to stay separate: concerns about hyperscaler P/E valuation are one issue; concerns about AI hardware demand are another. May 5 answered the second question positively. It did not touch the first. Investors who hold both in their heads simultaneously will be better positioned when evaluating their portfolios as Q2 and Q3 results arrive.

What to Watch Next

The Q1/2026 results shift the debate rather than end it. The question is no longer "does AI hardware have real revenue?" It has become: "will AI hardware revenue convert into profit for the hyperscalers?"

Key signals to track in the second half of 2026:

- Disaggregated AI revenue from hyperscalers: Microsoft, Google, Meta, and Amazon have yet to report AI product revenue in sufficient detail. Q2 and Q3/2026 are the first reporting periods where this could meaningfully change.

- HBM contract renewals for 2027: if Micron's long-term agreements are not renewed, the "cycle-breaking" structural argument loses its foundation.

- Power costs at AI data centers: electricity costs are rising faster than revenue in some regions; if they exceed economic thresholds, capex plans may be revised downward in the second half of the year.

The overall picture from Q1/2026 remains positive at the hardware layer. The remaining questions sit one level up, where the hyperscalers must demonstrate that hundreds of billions in capital expenditure are generating the returns their shareholders expect.