In late April, a consensus view spread across investor communities online: the US's 46% retaliatory tariff — even with a 90-day pause in effect — would pull Vietnam's seafood sector down. The logic sounded reasonable. The US had been the largest consuming market for years; anti-dumping investigations and countervailing duties had repeatedly dented the earnings of listed seafood companies. The reflexive trade — "sell seafood stocks when US tariff news breaks" — had genuine historical grounding.

The four-month 2026 data released by VASEP on the morning of May 5 ran in the opposite direction. The entire sector reached approximately USD 3.6 billion, up roughly 12% from the same period in 2025.Tuoi Tre Not because the US recovered. But because the market map has been fundamentally redrawn. That new map comes with a type of risk the market has not yet fully priced in.

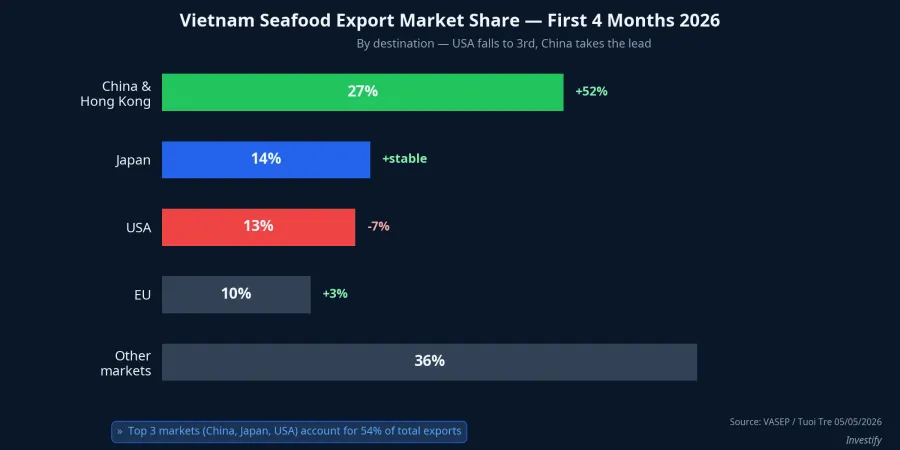

USA Falls to Third, China Takes the Lead

The export market structure changed fundamentally over the first four months of 2026.Tuoi Tre China and Hong Kong reached over USD 1 billion in value, up 52%, claiming approximately 27% of total exports and moving into first place. Japan held second position with around 14% market share, supported by stable demand for processed shrimp and surimi. The US declined approximately 7%, with its share narrowing to 13% and dropping to third. Cited reasons include anti-dumping duties on shrimp, bans on 12 product categories, and certificate-of-origin requirements. The EU reached approximately USD 452 million, up a modest 3%.

More notable than the headline growth figure is the composition of what China is buying. Lobster, pangasius and crab imports into China rose 50%. These are high-value products with significantly better margins than the commodity shrimp that historically dominated US-bound shipments. The right question is not "how much more is China buying" but "which products, and how durable is that demand."

Why China's Demand Has Surged So Strongly

Three forces are working together. All three can reverse. This is the detail worth pausing on before reading the 52% figure as unambiguously good news.

First, China is upgrading toward higher-value segments. Shrimp imports into China are forecast to rise 5% in value even as volume falls 2%, driven by middle-class consumer preference for larger sizes, processed products and lobster.Investify Vietnam holds a competitive advantage precisely in these segments, while Ecuador — the main rival — is concentrated in commodity shrimp.

Second, China has tightened informal border trade and is prioritizing formal-channel imports.Investify Vietnamese companies perform better on traceability and registered farming-zone credentials, giving them an edge over informal supply from other Southeast Asian sources.

Third, a portion of US-bound orders has been redirected to China-facing channels. When the US raised barriers, cold-storage capacity had to find alternative outlets within weeks. This redirection dynamic explains why China's jump was both fast and large in the same quarter the US tightened controls.

Together, the three forces make the 52% increase real. But they also make it potentially fragile: if US orders begin returning after the 90-day tariff pause ends, the redirection component naturally shrinks; if China suddenly tightens quarantine controls — as it has done repeatedly in 2018–2022 — the entire formal-channel pipeline can slow for weeks.

China Risk: Opaque, Fast, and Far Harder to Forecast

This is the dimension the conventional narrative is underweighting. People have grown accustomed to US risk because it is transparent: anti-dumping investigations take months, countervailing duties are announced in advance, and the magnitude of damage can be estimated from a company's US revenue share. It is a risk that is public, gradual, and measurable.

China risk operates on entirely different mechanics. Over the past eight years, the tightening episodes have followed a recognizable pattern. In 2018–2020, China increased 100% inspection rates on shrimp and pangasius shipments, extending clearance times and pushing cold-storage costs higher. Damage accumulated through margin compression rather than a single shock. In 2021–2022, Beijing applied COVID-19 surface-contamination controls on frozen goods, temporarily suspending imports from specific processing plants. Refrigerated containers backed up at northern border crossings for weeks. At various other points, Chinese customs officials tightened checks on consignments lacking registered farming-zone codes or proper formal-export registration, even from plants that met all stated standards.

The consistent pattern: China risk does not arrive through tariffs or trade-defence investigations. It arrives through sanitary-control decisions, sometimes issued within 24–48 hours, with effects lasting weeks to months. Even fully compliant plants can be suspended when China wants to send a political signal in a broader trade context. This risk has no advance notice, no investigation timeline, no fixed rate to model.

The real risk is no longer on the US tariff schedule. It sits in a quarantine announcement from Beijing that no one can time.

Seafood Stocks: Three Names in the Same Group, Three Different Directions

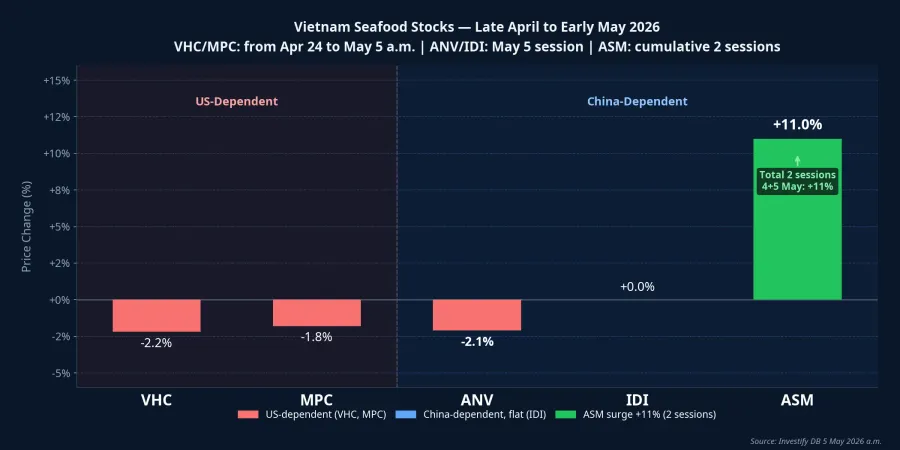

With the market structure shifting, Vietnam's seafood stocks are no longer a homogeneous basket. On the morning of May 5 — the very day VASEP confirmed China's surge — the market split in three directions simultaneously.

The US-dependent group, including Vinh Hoan (VHC) and Minh Phu (MPC), continued to pull back. VHC stood at VND 61,000, down 2.2% from April 24; MPC was at VND 15,900, down approximately 1.8% from early in the week. The temporary tariff advantage VHC enjoyed in March has already been priced in, and the outlook now depends on the outcome of US tariff negotiations after the 90-day pause expires.

The China-dependent group — Nam Viet (ANV), I.D.I (IDI) and Sao Mai (ASM) — showed a far more fragmented picture. ASM rose strongly over two sessions on May 4–5, gaining roughly 11% in total, tracking the China purchasing news. IDI was flat. ANV, also a pangasius producer with China-oriented market structure, actually fell 2.1% during the same morning session.Investify

That divergence is not short-term noise. It reflects a reality: demand from China is now established, but the supply-side story of each individual company — actual margins, customer relationships in China, history of quarantine disruptions, and ability to maintain order flow — has not yet been laid out in financial statements. What the four-month report does not say: the 52% China figure is a sector aggregate, not a uniform benefit distributed equally across every company in the group. When Q2 results are published, these three names will differentiate considerably.

Four Signals Worth Tracking

With the new market structure in place, the old narrative around USD/VND exchange rates or the next US tariff decision is no longer the focal point. Four things are actually worth monitoring:

China quarantine signals are the biggest risk for the ANV, IDI and ASM group. Any announcement of tightened inspections on registered farming zones, plant suspensions, or new certification requirements will have a direct and immediate impact on shipment volumes.

China import momentum in May–June is the most important near-term metric. If year-on-year growth stays at 50% in May, VASEP's full-year forecast of over USD 12 billion becomes credible. If the pace drops to 20–30%, end-of-year growth will contract meaningfully and require significant expectation revision.

Q2 revenue disclosures by individual companies will be the definitive test. VHC publishes monthly revenue figures consistently. ANV, IDI and ASM are less transparent; the Q2 financial statements are needed to see each company's actual US-versus-China revenue split. That is when the market will have enough data to separate genuine winners.

US tariffs after the 90-day pause remain the tail risk. If the 46% countervailing duty is reimposed, VHC and MPC face a second shock. If the pause is extended or rates are negotiated lower, US-side pressure eases and some redirected orders may return.

The belief that "US tariffs pull seafood stocks down" no longer fits the current picture. But the replacement belief that "China covers everything" needs more evidence before it becomes a reliable investment thesis. The accurate framing: the sector has swapped the type of risk it carries — from public and measurable to opaque and harder to forecast. The first Q2 report, or a quarantine announcement from Beijing, will confirm which companies are the real beneficiaries of this new structure.