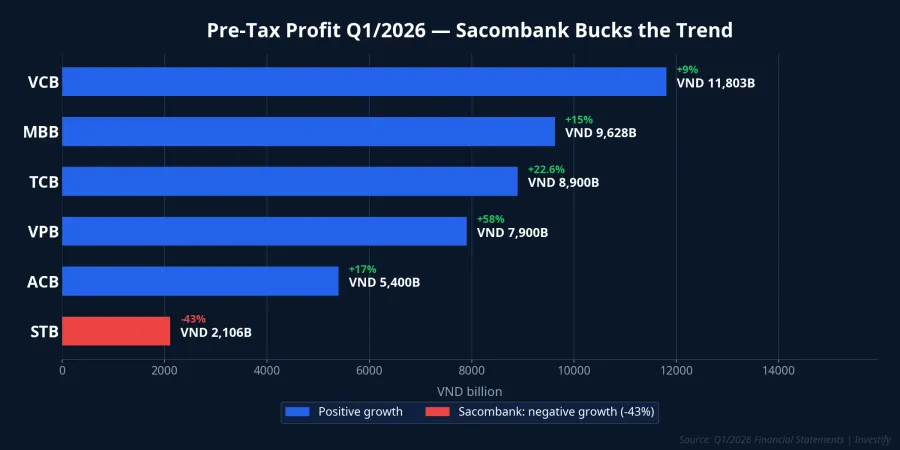

Looking at Q1/2026 numbers, Sacombank stands out as the only major private bank in the peer group moving in the wrong direction: pre-tax profit came in at VND 2,106 billion, down 43% year-on-year.Thoi bao Tai chinh Meanwhile, ACB grew 17% to VND 5,400 billionVnExpress, MB grew 15% to VND 9,628 billionBao Phap luat, Techcombank grew 22.6% to VND 8,900 billionMarketTimes, and VPBank grew 58% to VND 7,900 billion.LSVN But look inside the structure of Sacombank's numbers, and the picture changes entirely.

The 10x Provision Charge: The Number That Actually Matters

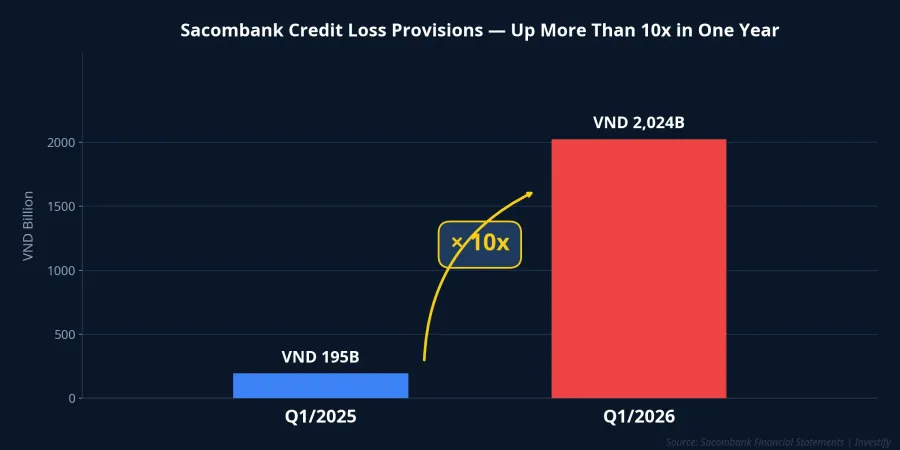

Credit loss provisions jumped from VND 195 billion in Q1/2025 to VND 2,024 billion this quarter, more than 10 times higher year-on-year.Thoi bao Tai chinh What the financial statements also show is that net operating income before provisions actually grew 7% year-on-year.Bao Phap luat In other words, the core business is not deteriorating. The 43% profit decline comes entirely from an intentional accounting decision: redirecting the bulk of net income into the loan loss buffer.

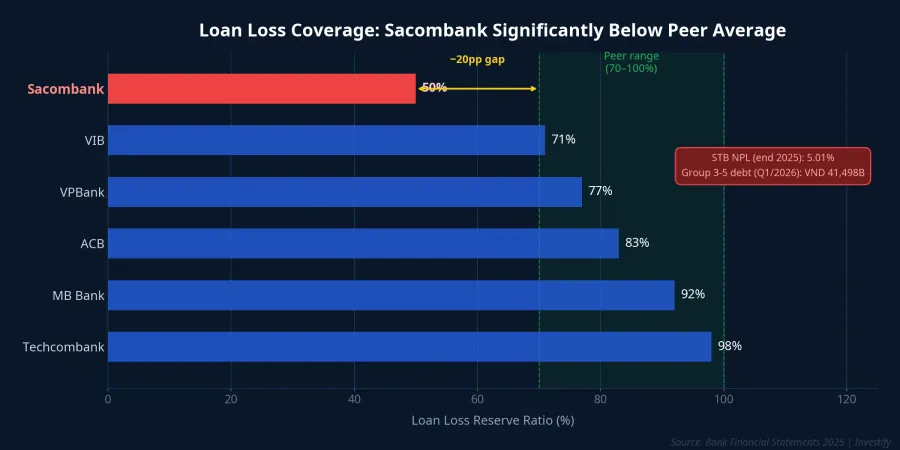

The reason for the additional buffer is a starting point that is still low by industry standards. At the end of 2025, despite provisioning over VND 11,300 billion during the year, Sacombank's loan loss coverage ratio had fallen to approximately 50% and its on-balance-sheet NPL reached 5.01%.Thoi bao Tai chinh By end of Q1/2026, Group 3-5 loans had risen a further 3.4% to VND 41,498 billion.Thoi bao Tai chinh A coverage ratio of approximately 50% sits well below the 70–100% range typical of large private peers. The bank is deliberately building that buffer before it can close out its legacy asset overhang.

Coverage Buffer Still Below Sector Average

The peer comparison makes the gap concrete. Techcombank runs a coverage ratio of 98%, MB Bank 92%, ACB 83%, VPBank 77%, VIB 71%. Sacombank sits at approximately 50%, roughly 20 percentage points below the lower end of the peer range. Closing that gap will take multiple quarters of elevated provisioning, which explains why the high provision run-rate is likely to continue.

Management has set a specific target for 2026: bring on-balance-sheet NPL below 5%. At end-2025 it was 5.01%; in Q1/2026 Group 3-5 loans still edged up. This metric is the clearest one to watch across quarterly reports.

Headcount at Lowest Since 2015

In parallel with the provisioning push, Sacombank has been accelerating its organisational streamlining. At the end of March 2026, total headcount across the bank and subsidiaries stood at 14,080, down 2,736 in a single quarter.Dan tri At the parent bank alone, headcount fell 2,570 to 13,281.VnExpress This is the lowest level since 2015. For context, during 2019–2020 the bank maintained 18,000–19,000 employees; over the past six years it has eliminated more than 5,000 positions.

This is not a headcount reduction driven by short-term financial stress. Service digitalisation and a leaner branch model are the structural drivers, running in parallel with the final phase of the restructuring program. A single quarter that simultaneously pushes both the loan loss buffer and the organisational footprint signals a clear order of priorities: clean up the balance sheet first, then grow.

The Final Knot: The 32.5% Trầm Bê Stake

To understand why Sacombank has had to go through this process, the backstory matters. The restructuring plan was approved by the State Bank of Vietnam in 2017, after the bank absorbed a massive bad debt legacy from the 2015 merger with Southern Bank (Ngân hàng Phương Nam).Phu nu Viet Nam The total value of legacy assets at the time was approximately VND 93,000 billion, comprising VND 35,000 billion in principal debt and VND 58,000 billion in accrued interest and receivables. The vast majority has now been provisioned.

The remaining bottleneck is 32.5% of Sacombank's shares pledged as collateral by the group associated with former Vice Chairman Trầm Bê, currently held under State Bank of Vietnam management.Nguoi Quan Sat Sacombank submitted its auction proposal to the regulator in 2025, but legal procedures and valuation have not yet been completed. Management expects final feedback from the State Bank in the second half of 2026.Bao Moi Some analysts still consider a slip into subsequent years a real possibility.

When the 32.5% stake is successfully auctioned, three things happen simultaneously. Sacombank recovers principal and interest, completing the restructuring plan. The accumulated loan loss provisions are released, unlocking a material profit uplift. And the bank is finally permitted to pay dividends for the first time in a decade, a plan already approved in principle at the April 2026 AGM, conditional on resolving the Trầm Bê stake.DNSE

2026 Plan and New Leadership

The April 2026 AGM approved a full-year pre-tax profit target of VND 8,100 billion, up just 6.2% from 2025 and 45% below the original 2025 target of VND 14,650 billion.Vietstock This is a deliberately compressed target designed to free up room for provisioning and NPL resolution, not a reflection of limited growth opportunity. After Q1, the bank has completed approximately 26% of its full-year profit target, exactly on a one-quarter pace.Bao Phap luat

On the leadership front, Mr Dương Công Minh continues as Chairman of Sacombank's Board of Directors, a position he has held since 2017.Tuoi Tre The AGM elected Mr Nguyễn Đức Thụy as Standing Deputy Chairman of the Board, directly overseeing strategic direction and senior governance.Sacombank Following Mr Thụy's move to the Deputy Chairman role, Mr Loic Faussier was appointed Acting Chief Executive Officer of Sacombank.Bao Phap luat The leadership transition is taking place precisely as the bank enters the closing chapter of its restructuring program.

STB Stock: Buying the Expectation, Not the Current Earnings

STB closed on May 5 at VND 66,600 per share with a market capitalisation of VND 125,600 billion. Over the 17 months from late 2024 to early May 2026, the stock more than doubled from the VND 30,000 range. The high in that period was VND 68,100 on April 28, the session right after the AGM approved the dividend plan.DNSE

The valuation the market assigns to STB today does not reflect a bank growing profits at 6% per year. It reflects an expectation: that the Trầm Bê auction succeeds, that the accumulated provisions are released, and that dividends are paid. That means STB's valuation risk is tied directly to the legal timeline of a single auction process, not to quarterly earnings delivery.

Three Signals Worth Watching

The Q1/2026 report makes one thing clear: Sacombank is in the final stretch of a nine-year restructuring, not somewhere in the middle. The thesis is grounded: core operations still grew 7%, management has set a specific NPL target, and the auction plan has been submitted to the regulator. That said, two risk factors require close monitoring. The State Bank's approval timeline remains uncertain. And Q1 NPL is still edging up rather than declining.

Three specific milestones to track across coming quarters:

First, the State Bank of Vietnam's response to the 32.5% Trầm Bê stake auction plan, expected in the second half of 2026. This is the condition for resolving the final bottleneck. If it slips to 2027, current valuations need to be reassessed.

Second, the loan loss coverage ratio at the end of each subsequent quarter. If the bank can pull the ratio from approximately 50% toward the 70%+ range, the elevated provisioning run-rate is likely to persist for several more quarters before easing.

Third, the on-balance-sheet NPL ratio each quarter. The full-year target is below 5%. End-2025 stood at 5.01%; Q1/2026 Group 3-5 loans still nudged higher. The first quarter in which NPL actually begins to fall will be the most concrete evidence that the clean-up is producing real results.

For a bank intentionally compressing its profit to direct resources toward provisioning, every quarter in which provisions remain elevated is a quarter closer to the endpoint rather than further away. The first quarter in which provisioning reverts to a normalised level will be the clearest signal that the final chapter has closed.