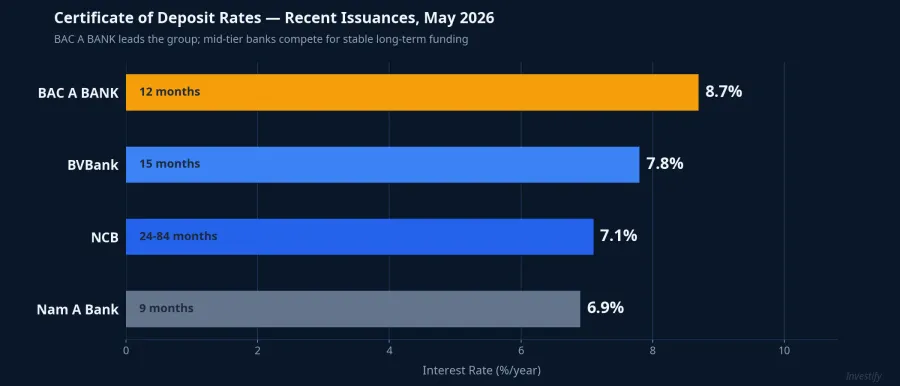

On May 5, 2026, BAC A BANK launched its first CD issuance of 2026, offering VND 3,000 billion worth of certificates of deposit at up to 8.7% per year, with a minimum denomination of VND 10 million and all interest paid at maturity.Tạp chí Kinh tế Tài chính At the same time, 12-month savings rates at the Big4 banks are sitting around 5.9% per year; Techcombank at 5.25%, and VPBank slightly higher at 6.5%.

At first glance, this seems contradictory: the same banking system, yet one product cuts rates while another pushes toward 9%. In reality, these are two fundamentally different products operating on different principles. Understanding this split is the first step toward choosing the right savings vehicle for your financial goals.

Four Key Differences Worth Understanding

A fair comparison covers four dimensions: interest rate, how interest is paid, flexibility, and deposit insurance.

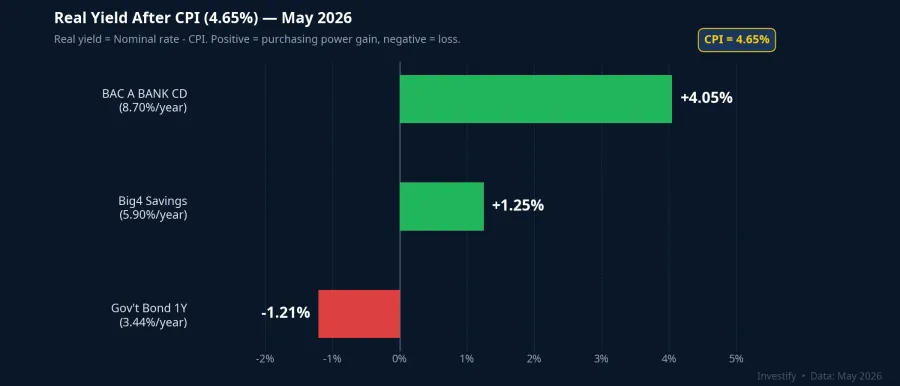

Interest rate. BAC A BANK's 8.7% CD rate exceeds the same bank's regular 12-month savings rate by approximately 1.4 to 1.6 percentage points, and it is 2.8 percentage points above Big4 banks. After adjusting for the March 2026 CPI of 4.65%, the real yield on the CD reaches approximately 4.05% per year, while Big4 savings yield only around 1.25% per year in real terms.

How interest is paid. Regular savings accounts typically offer two options: monthly interest payments or a lump sum at maturity, giving depositors a steady cash flow if they choose the monthly option. BAC A BANK's CD pays all interest at maturity with no monthly option. Simply put: you give up 12 months of interim cash flow in exchange for earning the higher rate on your full principal.

Flexibility. Under Circular 02/2025/TT-NHNN, certificates of deposit are negotiable instruments; early withdrawal typically earns only the demand deposit rate, the same effective penalty as regular savings accounts. The genuine advantage of a CD is transferability: you can sell it to a third party, whereas a savings passbook cannot be transferred. That said, the secondary market for retail CDs in Vietnam is still very thin, making this more of a paper advantage than a meaningful liquidity channel for individual investors today.

Deposit insurance. The 2025 Deposit Insurance Law raised the coverage limit to VND 125 million per depositor per institution, effective May 1, 2026. Both CDs and regular savings accounts fall under this limit. This means: if you deposit VND 1 billion at a single bank in any form, insurance only covers up to VND 125 million in the event that bank becomes insolvent. The remainder stands alongside other creditors in the resolution process.

Why Banks Are Willing to Pay 2 to 3 Percentage Points More

This rate premium is not a temporary promotion. It reflects the market price for something banks genuinely need: committed, term-locked funding that won't be withdrawn unexpectedly.

Here's a simple way to think about it: a 12-month savings account, even with a stated 12-month term, can be withdrawn at any time. The bank must factor that probability into its liquidity management. A CD has stricter early-redemption and transfer conditions. Especially at denominations of VND 10 million and above, depositors tend to hold until maturity. For the bank, this is "term-certain" funding that makes long-term capital planning far more predictable.

Demand for this kind of funding is also pushing the premium higher. Credit growth at many mid-tier banks has been outpacing deposit growth, intensifying the race to attract long-term capital. Several institutions have recently issued CDs at attractive rates: BVBank at up to 7.8% per year for 15 months,Báo Mới Nam A Bank at 6.8% and 6.9% per year for 6- and 9-month tenors, and NCB's "An Phat Loc" product at up to 7.1% per year for terms from 24 to 84 months. BAC A BANK's 8.7% is the highest in this group.

Against Government Bonds: Real Yield Tells the Real Story

Set against the risk-free benchmark, the gap becomes even clearer. The secondary-market yield on 1-year Vietnamese government bonds was around 3.4% per year at the end of April 2026. After subtracting the 4.65% CPI, the real yield on government bonds is negative: holders are losing purchasing power in real terms.

The 8.7% CD delivers a real yield of approximately 4.05% per year after inflation. This comes with a conscious trade-off. Government bonds are fully backed by the state, while CDs carry deposit insurance of only VND 125 million per institution. The nearly 5 percentage-point spread between the two products represents the market's price for the issuing bank's credit risk plus an illiquidity premium.

This does not mean one product is better than the other. It means each is suited to a different risk profile and a different set of needs.

Three Questions to Guide Your Decision

For anyone with idle funds weighing the options across banking channels, these three questions help you find the right fit before committing.

Question 1: Is your cash flow plan for the next 12 months clear? If there is any chance of an unexpected expense such as home repairs, tuition fees, or another investment opportunity, the on-demand flexibility of a regular savings account is worth more than the 2 to 3 percentage-point rate advantage. If your finances are fixed and no irregular outlays are expected over the next 6 to 12 months, a CD is genuinely worth considering.

Question 2: Does your total balance at one bank exceed VND 125 million? If so, the amount above VND 125 million is uninsured. The common safeguard is to spread deposits across multiple banks, keeping each account within the insurance limit. With CDs starting at VND 10 million, this diversification is achievable but requires opening accounts at several institutions.

Question 3: Do you need periodic interest income during the deposit term? Retirees and those who use interest income to cover monthly living expenses need monthly payments. Only regular savings accounts offer this option. A CD that pays at maturity is only appropriate when both principal and interest can sit untouched for the full 12 months.

One additional option worth knowing: fixed-income products on investment platforms are currently offering yields of approximately 10 to 11% per year with more flexible interest schedules. Structurally, these products sit between a CD and a corporate bond. The implication for your wallet: higher risk than deposit insurance covers, but meaningfully higher yields than standard bank deposits.

The System Is Tiering, Not Shrinking Your Returns

Falling regular savings rates do not mean banks are losing their ability to reward depositors. Banks are segmenting more explicitly: low-yield for on-demand money that banks cannot commit to long-term use; high-yield for term-locked money that banks can plan around.

This two-tier structure is common in developed banking systems around the world. What is newer in Vietnam is the widening spread between the two tiers. Two signals worth tracking in the coming months: whether mid-tier banks continue competing aggressively for deposits through high-rate CDs, and whether the current trend of cutting short-term savings rates reverses when the State Bank adjusts its interest rate guidance.