BSR's (Binh Son Refining and Petrochemical) Q1/2026 consolidated financial statement recorded a net profit after tax of VND 8,265 billion, up nearly 21 times from the same period a year ago, marking the highest quarterly figure in four years.Tuoi Tre Total net revenue reached VND 46,462 billion, up approximately 44% from Q1/2025.CafeF These figures are real and independently verified. But reading them accurately requires one more data point from the same balance sheet: inventory at March 31, 2026 stood at VND 21,573 billion, nearly double the level at the start of the year.Bao Phap Luat

Record profit and ballooning inventory are not independent events. They are two sides of the same mechanism that operates at every refinery when Brent crude rises sharply: a dynamic that rarely gets explained clearly to retail investors.

Record Profit: Reading the Structure Correctly

The most telling detail in the Q1/2026 financials is the gap between revenue growth and profit growth. Revenue rose approximately 44%, but net profit rose 21 times over. That gap reflects gross margin jumping to approximately 20.7% from around 1.2% in the same quarter last year. This is a margin expansion story, not a volume growth story.

Looking at operating throughput, the Dung Quat refinery processed close to 2 million tonnes of crude in the quarter, entirely within its normal operating range. The plant did not suddenly become more efficient; it did not meaningfully cut costs. The bulk of the VND 8,265 billion profit came from the price differential, not from any change in the refinery's operational processes. To understand where that price differential came from, the inventory gain mechanism needs unpacking.

The Inventory Gain Mechanism: When the Tank Farm Earns Money

Oil refinery operations follow a process with a clear time lag: purchase crude oil, ship it from the Arabian Gulf to Dung Quat, process it through distillation towers, then sell gasoline and diesel into the market. The gap between purchase and sale typically spans several weeks to a month.

During that window, if Brent prices move higher, the following happens: the crude was purchased at a lower price, but the finished products are sold at current market prices that already reflect the higher Brent level. The gap between the recorded cost of inventory and the market price at the point of sale converts into margin. That is an inventory gain. It is a genuine, fully recognized accounting effect. This is not a technical adjustment or an accounting trick. It is simply an unavoidable consequence of the production cycle in a rising-price environment.

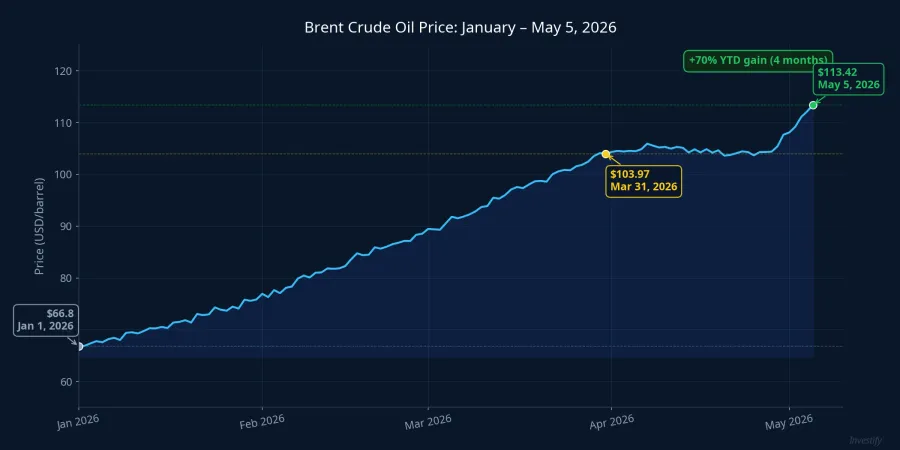

Q1/2026 was a textbook window for this mechanism. Brent rose from approximately $66.8 per barrel at the start of January to $103.97 per barrel by the end of March, a gain of more than 55% in just three months.Bao Phap Luat Every barrel BSR purchased in January at around $67, processed, and sold in February or March at output prices anchored to $90–104 Brent automatically carried that price differential into the income statement.

Over VND 9,000 Billion in Crude Still at Sea

The geopolitical backdrop adds another layer to BSR's inventory story. Throughout Q1/2026, the Strait of Hormuz remained under sustained tension, with recurring confrontations in the Gulf region, most recently an Iranian strike on the UAE's Fujairah oil port on May 4. Against this backdrop, BSR increased its debt by nearly 60%Nguoi Quan Sat to import additional crude, securing feedstock supply through July 2026 in a scenario where Hormuz becomes disrupted.

That decision has two distinct dimensions. From a supply chain risk management perspective, an unplanned plant shutdown from feedstock shortage costs far more than storage expenses, making high inventory an entirely rational hedge in an unstable geopolitical environment. At the same time, buying additional crude at precisely the moment Brent was rising means every extra barrel gets revalued upward as Brent climbs further.

The result: more than VND 9,000 billion in crude oil was in transit, still aboard tankers and not yet docked at Dung Quat as of March 31, 2026.Nguoi Quan Sat These cargoes are a pure oil-price position on the balance sheet. With Brent rising from $103.97 at Q1 close to $113.42 on May 5, the price difference continues flowing into unrealized profit on those batches.

The symmetry here is critical. The same VND 21,573 billion inventory base that generates gains when Brent rises will create pressure for impairment provisions when Brent falls below the recorded cost. Under accounting standards, that reversal hits net profit directly in the quarter it is recognized. The leverage runs in both directions.

Current Safety Margins and the Q2 Equation

A sensitivity analysis based on Q1/2026 refining margins suggests BSR's Brent breakeven sits in the $50–55 per barrel range if crack spreads hold at Q1 levels. When crack spreads narrow 10%, the breakeven moves up to $58–60. When they widen 10%, it drops to $45–48.

Brent closed at $113.42 per barrel on May 5, up approximately 8.6% over the past week.CafeF The cushion above breakeven is wide: more than $50 under every crack spread scenario. At these levels, core refinery operations remain firmly profitable without relying on inventory gains.

The real question for Q2 is not whether BSR will lose money on operations. It is about the gap between two scenarios. If Brent holds the $105–115 range through Q2, inventory continues to be revalued or maintained at cost, and Q2 earnings could approach Q1 levels. If Brent retreats to $90–95 due to Iran-U.S. negotiations advancing or a stronger OPEC+ supply increase, the difference between inventory acquired at $100–113 Brent and new market prices will create pressure on inventory values. Q2 profit could fall sharply from Q1 with no change whatsoever in plant operations.

The Stock Is Pricing Brent

BSR closed at VND 26,750 on May 5, up 5.94% for the session on volume of 24.5 million shares, twice the 30-session average.CafeBiz From its April 28 trough of VND 23,400, the stock has recovered approximately 14.3% over a few sessions, bringing market capitalization close to VND 134,000 billion.

The rally coincided with Brent rising from $104.40 on April 28 to $113.42 on May 5. The strong Q1 results, the Brent uptrend, and the Fujairah attack catalyst on May 4 all plausibly contributed to the recovery, in proportions that are difficult to isolate precisely. What is clear is that the market is pricing BSR in sync with crude oil, consistent with the inventory-dependent earnings structure the Q1 report laid bare.

The forward-looking question is: to what extent does the current share price already reflect the unrealized profit on the VND 21,573 billion inventory, and will that value convert into reported earnings or reverse, depending on where Brent trades over the next two months.

Signals to Watch

Three factors will shape BSR's Q2 earnings trajectory.

Iran-U.S. Negotiations. Both sides appear to be leaning toward phased de-escalation. Iran has permitted some shipping exemptions; U.S. strikes on energy infrastructure have moderated. A temporary Hormuz reopening agreement would pull Brent back toward the $90–100 range quickly and hit inventory values directly.

OPEC+ June 2026 Meeting. The group increased output by roughly 206,000 barrels per day starting in April, but major members remain cautious. A more aggressive supply increase is a second, independent downside factor for Brent that does not require Iran progress.

BSR Q2/2026 Financial Report. This is the definitive test. If Brent holds $105–115 through Q2, earnings should track close to Q1. If it drops to $90–95, the gap between the two quarters will provide a quantitative proof of the inventory gain mechanism that Q1 first revealed.

BSR's Q1/2026 record profit of VND 8,265 billion is real and fully verified. But the current earnings structure leans heavily on inventory revaluation driven by Brent, rather than on improved core operational efficiency. That is not a negative signal in itself: at $113 Brent with a $50-plus buffer above breakeven, BSR is operating solidly in the black. It simply means that when reading the Q2 report, the most important number is not total profit but its internal composition: how much came from inventory gains versus genuine refinery margin. The Q2 report will answer that question more clearly than any forecast. The deciding factor is where Brent trades over the next two months. Iran and OPEC+ are the two variables to watch.