Every year in early May, global investors dust off the same old adage: "Sell in May and go away." This year, that question returns with an unusually high-stakes backdrop. VN-Index closed April at 1,854.10 points, logging a monthly gain of 10.73% — its strongest performance since the post-COVID recovery in 2020. On the morning of May 4, investors returned to the exchange after a five-day public holiday and stepped into a month with two major unresolved variables: the US Navy's "Project Freedom" operation to escort commercial ships through the Strait of Hormuz, and the US non-farm payrolls report due Friday, May 6. The big picture is unusually binary: this is not an average May.

A 17th-Century Adage in a 21st-Century Market

The full saying is "Sell in May and go away, come back on St. Leger's Day", tracing back to London's financial circles in the 1600s, when the upper class would leave the city for summer and return to trading around September. Bouman and Jacobsen (2002) tested the pattern across 37 markets and found that November-to-April returns outperformed May-to-October returns in 36 of them. Subsequent research has shown the effect weakening as developed markets grew more informationally efficient. Vietnam is even further from the original model: its market history is shorter, and its capital flow dynamics are fundamentally different.

Vietnam's May Track Record: Effect Has Faded

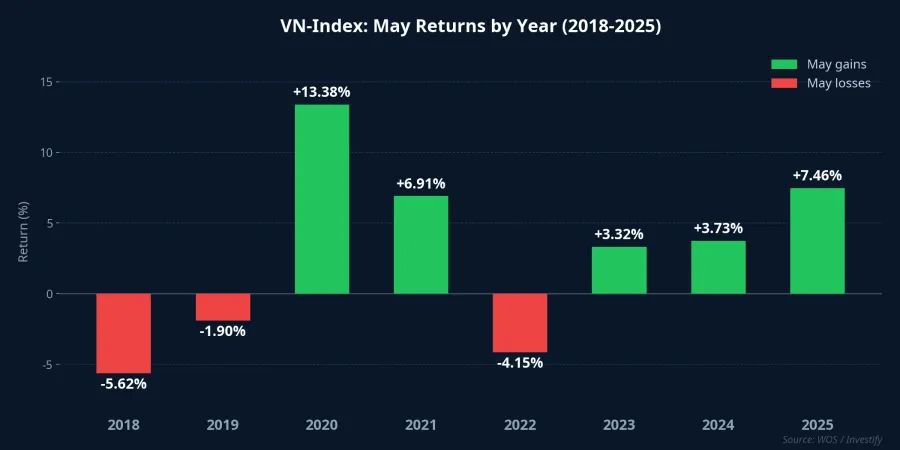

Across 25 years of VN-Index history, the market advanced in May in 12 out of 25 years, a win rate of roughly 48%.CafeF Viewed over that full 25-year window, May looks no better than a coin flip. But zoom in to the past 10 years and the win rate climbs to 70%. Whatever "Sell in May" effect once existed in Vietnam has clearly weakened since the flood of retail capital entered the market after 2020.

Looking at the eight most recent years (2018–2025), VN-Index posted five May gains and three May losses. The worst years were 2018 (–5.62%) and 2022 (–4.15%), both coinciding with global inflation and rate-hike pressure. The important lesson: those down Mays were driven by specific macro conditions, not a calendar pattern. Which brings us to the real question: what are the specific macro conditions in May 2026?

Two Opposing Forces Open the Month

The macro picture at the start of this month is unusually polarized.

The supportive side is genuinely strong. The S&P 500's VIX volatility index closed the final week of April at 16.99, falling 36.9% over the month — its lowest reading since the start of the year, reflecting peak short-cycle risk appetite. Brent crude has pulled back from a high of $126/bbl to around $110/bbl following an initial de-escalation of Iran tensions.Gulf News On the medium-term horizon, FTSE Russell has confirmed it will officially upgrade Vietnam to Secondary Emerging Market status on September 21, 2026.CNBC That event is a powerful structural anchor for passive fund inflows over the coming months.

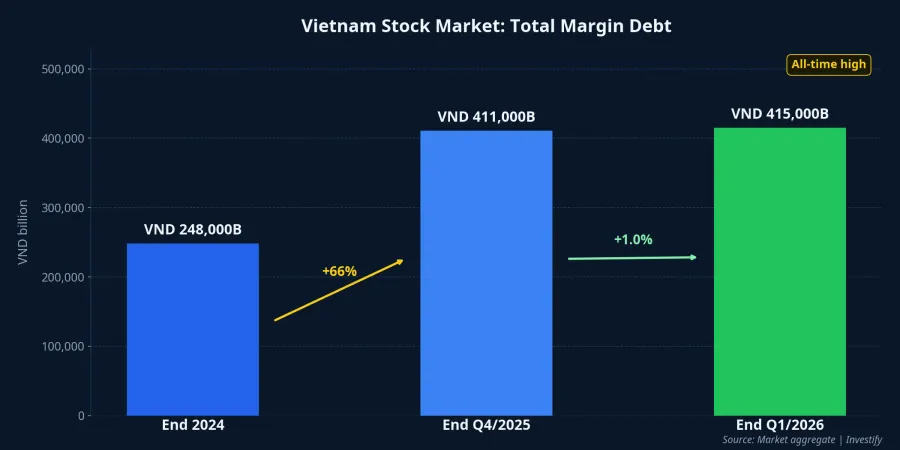

The risk side has also built up significantly. Foreign investors sold a net VND 13,800 billion on HOSE in April, bringing the year-to-date net outflow to over VND 41,300 billion.Tin Nhanh Chung Khoan All of that selling pressure has been absorbed by domestic capital and leverage. Total market margin debt at the end of Q1/2026 reached an estimated VND 415,000 billion — an all-time high.VietnamFinance Compared to the end of 2024, when the figure stood at VND 248,000 billion, leverage has grown more than 67% in just five quarters.

High leverage does not create immediate risk when prices are rising. But when the market pulls back quickly, margin becomes an amplifier: forced liquidations push prices lower, triggering more liquidations in a self-reinforcing loop. This is precisely what makes May 2026 worth monitoring more carefully than an average May. Not because of the calendar, but because of the leverage structure in place.

Hormuz and US Jobs: Two Open Questions

Capital flows are waiting on two specific events.

Variable one: Project Freedom. On May 3, the US president announced that the Navy would begin escorting commercial ships from other countries through the Strait of Hormuz starting Monday morning.Gulf News If Iran does not escalate and the operation proceeds smoothly, Brent can hold stable in the $100–$110 range and global risk appetite can stay elevated. If there is an incident at Hormuz, VIX spikes and capital flows into safe havens. That is an adverse scenario for every emerging market, Vietnam included.

Variable two: US Non-Farm Payrolls on May 6. The NFP print and unemployment rate will either confirm or challenge the market's expectations for the Fed's rate-cut path. If NFP exceeds 150,000 and unemployment stays below 4.2%, that supports the bull scenario: the US economy holds, the Fed is not pressured into fast cuts, and risk appetite persists. If NFP falls below 100,000 or unemployment breaches 4.3%, fears of a rapid economic slowdown would pull capital out of risk assets.

These two variables operate through different mechanisms but converge on the same output: the global level of risk appetite, and by extension, the pressure or support VN-Index faces.

Three Signals to Watch the Week of May 4–8

The last time VN-Index faced a similar binary setup — two clear scenarios, no tiebreaker signal yet — was in late October 2023 ahead of the Fed rate decision. The market could not predict the direction at the time, but it reacted quickly once the signal arrived. That lesson still applies.

This week has three concrete resolution points:

First: VIX. The 22 level is the dividing line. Any session closing below 20 supports the bull scenario; crossing 22 tilts toward the pullback scenario.

Second: US NFP on the evening of May 6 (Vietnam time). A print above 150,000 with unemployment below 4.2% sustains the bull case. A print below 100,000 or unemployment above 4.3% triggers rapid-slowdown concerns.

Third: Foreign fund flows in the first week of May. Switching to net buying for 3 or more of the 5 sessions is the earliest indicator of capital front-running the September FTSE upgrade. Continued net selling above VND 2,000 billion per session signals the pullback scenario is consolidating.

Leverage Amplifies, It Does Not Predict

Twenty-five years of data do not support a rigid "sell in May" strategy for Vietnam. But VND 415,000 billion in margin debt changes one important thing: the market's reaction to any external shock is amplified in both directions. If VIX rises and Hormuz turns volatile, the depth of any pullback will be greater than it would be without high leverage in the system. If NFP comes in strong and foreign capital reverses, the rally could also overshoot expectations as the same leverage works in reverse.

The question for this week is not "Sell in May or not?" The real question is: in which direction do the three signals point, and how does your portfolio's position compare to the current leverage structure in the market?

The bull scenario (B) depends on Hormuz stability, a solid US jobs report, and a reversal in foreign flows. The cautious scenario (A) needs only one of those three to turn. The speed and magnitude of either move will be set by VND 415,000 billion in margin waiting to react.