When Moody's published its assessment on May 4, 2026, the headline was straightforward: Vietnam's credit outlook had been upgraded from Stable to Positive, with its Ba2 rating unchanged.Báo Chính phủ Many investors scrolled past: "It's not an actual upgrade, so what's the story?" The answer lies in how financial markets work. Markets do not wait for formal rating changes before adjusting. They reprice the moment an outlook shifts. That raises the more practical question: through what mechanism will Vietnam's government bond yields respond, and where does the broader picture stand?

A Positive Outlook Is a Probability Signal, Not a Rating Promise

In Moody's methodology, the "Outlook" signals the likely direction of a rating over the next 12 to 18 months. A Positive Outlook does not guarantee an upgrade — but it raises the probability meaningfully compared to a Stable Outlook over the same horizon. An upgrade remains conditional.

Moody's cited specific drivers. First, institutional quality and governance are improving through a wave of administrative, legal, and public-sector reforms launched in late 2024.Tuổi Trẻ Second, a diversified export base, recovering domestic demand, and sustained FDI inflows are providing growth stability. Third, the risks from U.S. trade measures have receded more than expected at the start of the year. The caveats are clear: vulnerabilities in the banking system, the property market, and certain institutional weaknesses remain key variables on the path to Ba1.

The regional context sharpens the significance of this move. Thailand's outlook was upgraded from Negative to Stable on April 23, 2026, but its Baa1 rating was held.Moody's Ratings Indonesia's outlook was downgraded to Negative. The Philippines held Stable at Baa2. Vietnam was the only country in this regional assessment cycle to move up one outlook notch. To reach investment grade, Vietnam needs two more notches: from Ba2 to Ba1, then from Ba1 to Baa3.

Three Market Layers That Reprice Yields Before the Rating Changes

Government bond yields do not wait for Moody's to finalize an upgrade. Three layers operate in parallel.

Layer 1: Passive index-tracking funds. Several regional and global bond indices determine country weights based on a combination of rating and outlook. When an outlook is upgraded, passive ETFs and index-tracking funds may increase their Vietnam allocation. The resulting real-money demand flows into the secondary market, placing downward pressure on yields.

Layer 2: Active funds repricing expectations. Active fund managers do not need to wait for the formal rating change. They revise the implied upgrade probability in their pricing models the moment the outlook shifts, then build positions ahead of it. Historically, the bulk of yield adjustment happens during this phase, not on the day Moody's announces the formal upgrade.

Layer 3: Corporate bond issuance. Government bonds are the pricing anchor for the entire credit market. When government bond yields fall, large corporates issuing new debt benefit from lower funding costs: credit spreads stack on top of a meaningfully lower benchmark yield.

Current Data: Elevated Yields, Volatile Foreign Flows

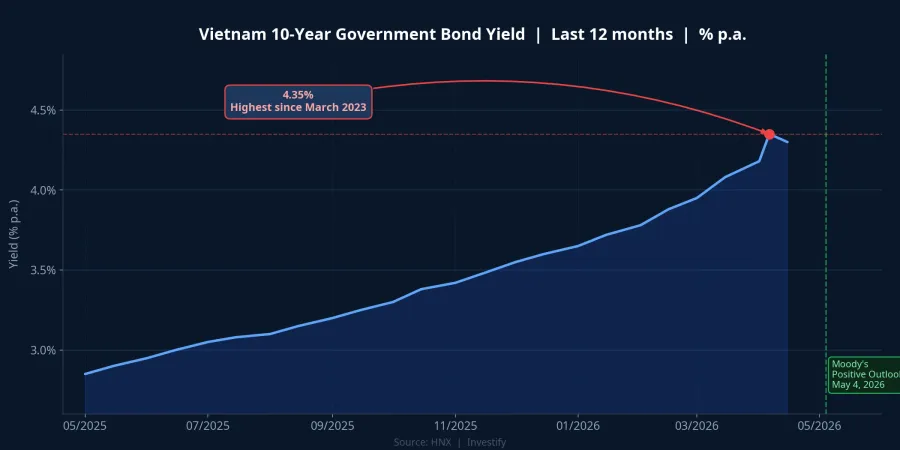

The 10-year government bond yield in the secondary market stood at approximately 4.35% on April 6, 2026, the highest level since March 2023. This represents an increase of approximately 1.28 percentage points year-over-year. In the primary market, the average winning bid rate for 10-year tenors hovered around 4.06–4.08% through Q1 and April 2026. Yields were already elevated before Moody's acted. The open question is how much room they have to compress over the coming weeks.

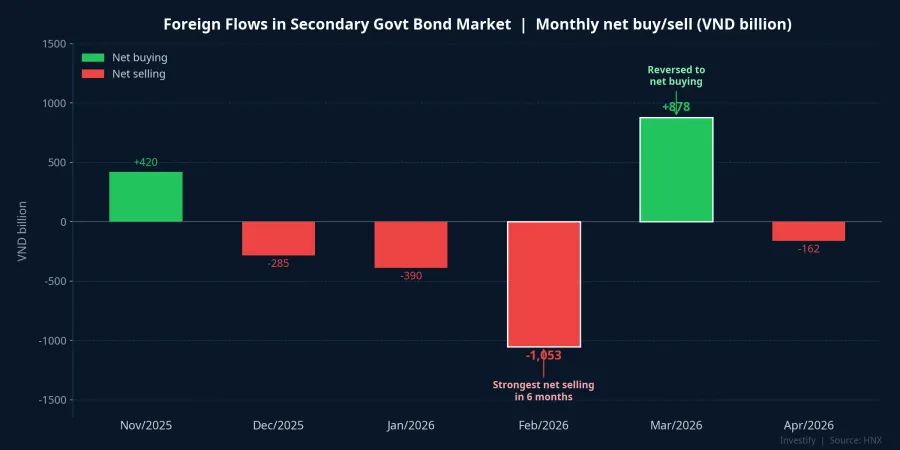

Foreign capital flows during Q1 told a mixed story. According to State Treasury data, foreign investors were net sellers of approximately VND 1,000 billion in the secondary market in February 2026, before reversing to approximately VND 878 billion net buying in March 2026. The full quarter remained in net-outflow territory.State Treasury The State Treasury raised approximately VND 80,100 billion in Q1 and approximately VND 106,300 billion through the end of April, predominantly in long-tenor issuances.

These two data points matter together: a large supply pipeline is meeting demand that is still volatile. A Positive signal from Moody's may not be sufficient to reverse foreign flows immediately if global factors — U.S. Treasury yields, broader emerging-market sentiment — continue to push in the other direction.

What Moody's Needs to See Before Confirming Ba1

Moody's does not publish hard numerical thresholds for an upgrade, but its methodology centers on three criteria.

Fiscal strength: government debt-to-GDP stable or declining, with debt-service growth remaining controlled even as public investment spending stays high.

Institutional quality: the administrative, legal, and governance reforms (ministerial mergers, reduced management layers, revised investment and land laws) must show actual results in governance indicators, not just policy announcements.

External resilience: foreign exchange reserves remain adequate, with FDI inflows and export growth sustaining momentum despite ongoing uncertainty around U.S. tariffs.

Moody's has set itself a 12-to-18-month review window. If these three conditions are reinforced, an upgrade from Ba2 to Ba1 is the base scenario. If banking and property risks resurface, or if government debt spikes significantly due to public investment that does not generate offsetting revenue, the outlook could be pulled back to Stable without an upgrade.

Three Signals Worth Watching

For portfolios with government bond exposure, three milestones are worth tracking.

First, the 10-year yield trajectory over the next four to eight weeks. If yields retract from the 4.3% zone without an external shock, it signals that the market is pricing in the upgrade expectation. If yields move sideways or drift higher, the Moody's signal is being overridden by global forces.

Second, the May and June foreign flow reports. Consistent net buying over consecutive months would be a clear signal that active funds have started accumulating positions in anticipation of an upgrade.

Third, action from Fitch and S&P over the next two to three quarters. The other two members of the "Big Three" agencies typically follow Moody's with a lag of several months. When all three align on a Positive outlook, the signal carries significantly more weight than Moody's alone. That is when passive index-fund flows tend to respond most visibly.

The current picture: upgrade expectations are a positive variable, but yields in the 4.0–4.3% range already reflect some long-tenor risk premium. The ultimate answer depends on how quickly institutional and fiscal conditions solidify over the next 12 to 18 months. Moody's next review will be the key checkpoint.