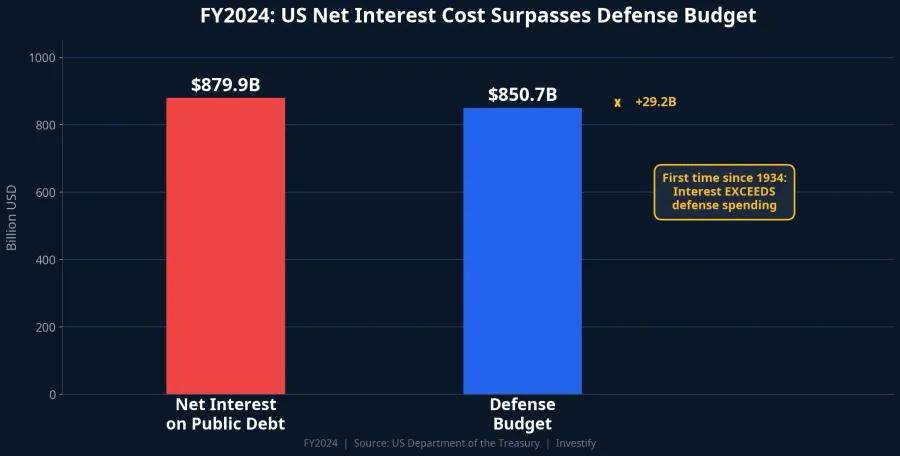

In fiscal year 2024, the US federal budget recorded a figure not seen since 1934: $879.9 billion in net interest on the national debt, exceeding the $850.7 billion defense budget by $29.2 billion.CRFB This was not the product of a single bad quarter or one misguided policy decision. It is the endpoint of a 16-year accumulation of debt driven by three structurally distinct jumps. Understanding those three jumps is the only reliable way to answer the question most investors are asking: why are global interest rates unlikely to return to the low-for-long regime of 2010–2020, and what does that mean for their portfolios today?

Three Jumps, Three Different Mechanisms

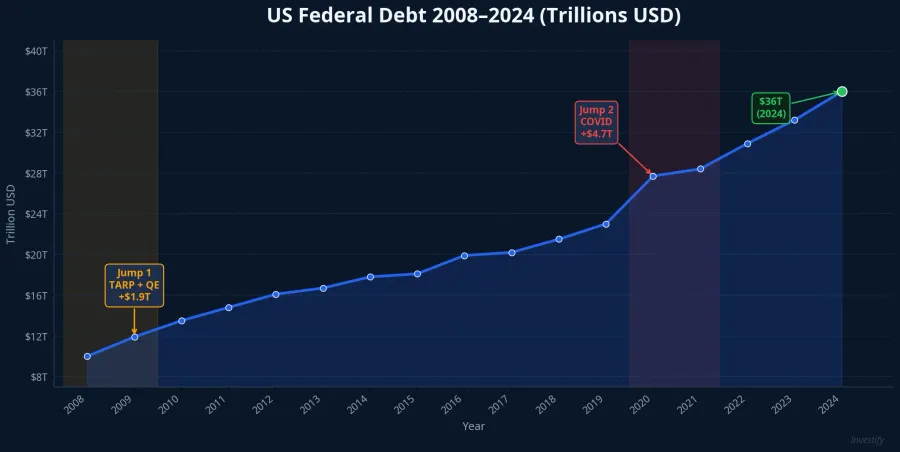

The US national debt chart does not show a smooth upward line. It shows three distinct surges, each driven by a different mechanism. What makes the third jump particularly consequential is that it added no new debt at all. It simply repriced the entire stock of debt accumulated in the first two.

Jump One: 2008 and Quantitative Easing

The 2008 financial crisis forced Congress to approve the $700 billion TARP program to stabilize the banking system.CRFB The Federal Reserve simultaneously launched an unprecedented quantitative easing program, cutting the federal funds rate to near-zero and holding it there for nearly seven years.

Federal debt stood at roughly $10 trillion before the crisis. By the end of the Obama administration in 2017, it had surpassed $17 trillion. Yet during this period, rising debt volume did not translate into rising interest costs: near-zero rates allowed the Treasury to issue new debt at historically cheap rates. The problem was deferred, not eliminated. When those bonds matured, they would need to be refinanced at whatever rate prevailed at that time.

Jump Two: 2020 and the COVID Stimulus

In March 2020, the pandemic triggered the largest peacetime fiscal response in US history. Within twelve months, the CARES Act ($2.2 trillion), successive supplemental packages, and the American Rescue Plan of early 2021 added approximately $5 trillion to the debt. The Fed returned to near-zero rates, repeating the 2008 playbook almost exactly.

Total federal debt surged from roughly $23 trillion at the start of 2020 to over $28 trillion by end-2021. For the second time in twelve years, an enormous block of new debt was issued at near-zero rates. The underlying risk was identical: this entire block would eventually need refinancing. The cost would be determined by the prevailing rate at maturity, not at issuance.

Jump Three: 2022–2023 and the Refinancing Math

US inflation peaked above 9% in the summer of 2022, forcing the Fed into the fastest rate-hiking cycle in four decades: from near 0–0.25% in early 2022 to a peak of 5.25–5.50% by mid-2023, before modest cuts brought the rate to its current 4.50%.

Jump Three added no new debt. Instead, it transformed the cost structure of the entire existing pile. Bonds issued at 1.5% during COVID maturing in 2024–2025 had to be refinanced at 4.5–5%. With every refinancing cycle, the annual interest bill ratchets up another notch. By FY2024, net interest reached $879.9 billion — double the FY2020 level — and exceeded defense spending for the first time in nine decades. Total federal debt now stands at approximately $36 trillion.US Treasury

The FY2024 Milestone and the Road to 2036

Niall Ferguson, Senior Fellow at the Hoover Institution at Stanford University, labels this threshold "Ferguson's Law": when a great power spends more servicing debt than on defense, its geopolitical position begins to erode.Fortune In his February 2025 study, he cited Spain in the 17th century and the British Empire after World War II. Both lost great power status within decades of crossing this threshold.Hoover Institution The historical argument can be debated; the underlying data cannot.

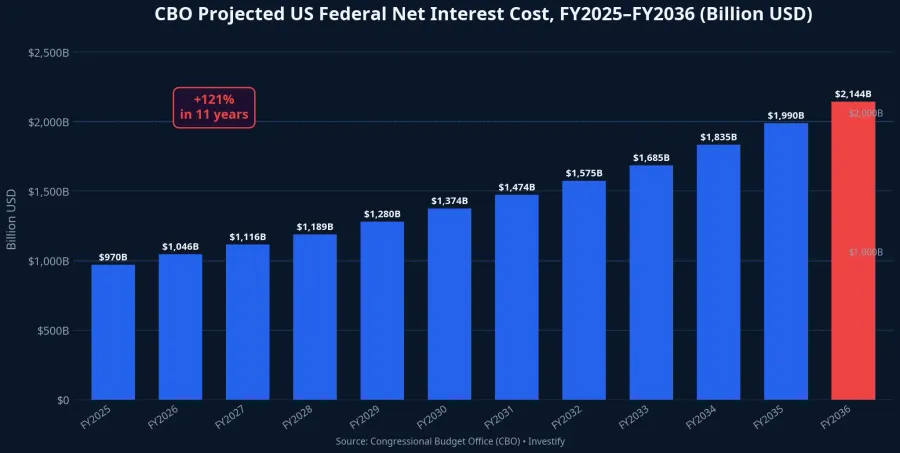

The trajectory ahead offers no self-correction. According to the Congressional Budget Office's Budget and Economic Outlook: 2026 to 2036, published in February 2026, net interest costs are projected to reach $1,039 billion in FY2026 and climb to $2,144 billion by FY2036. As a share of GDP, interest costs are expected to rise from 3.3% today to 4.6% by 2036. The CBO is a nonpartisan analytical agency that serves Congress: this is not advocacy or forecasting from a think tank with a policy agenda.

Why the Fed Cannot Pivot Easily

The three-jump trajectory has placed the Federal Reserve in a structural bind. Easing too early or too aggressively risks reigniting inflation. The 2022 episode is recent enough that no one at the Fed is ready to repeat it. But holding rates high for too long means each successive refinancing of the $36 trillion debt pile pushes the annual interest bill higher, crowding out spending on infrastructure, education, and entitlements.

Core PCE inflation, the Fed's preferred gauge, came in at 3.2% for March 2026, well above the 2% target.BEA Meanwhile, the DXY dollar index stood at 98.13, down approximately 2.1% in early May 2026, signaling that markets expect the Fed to eventually ease.CNBC These two signals pull in opposite directions. The practical result: the path of least surprise for the Fed is "higher for longer", not a rapid return to the near-zero rates that defined 2010–2020.

Four Channels to Vietnamese Investors

The US fiscal picture is not a remote Washington problem. It translates into four direct channels affecting Vietnamese markets.

USD/VND Exchange Rate. The USD/VND rate sat at 26,355 in the May 1 session, up approximately 1.2% over the prior 12 months. When the interest rate differential between the dollar and the dong remains wide, the State Bank of Vietnam must keep VND rates high enough to reduce capital outflow pressure. This narrows the room for domestic monetary easing, which helps explain why deposit rates have been trimmed but not slashed.

Foreign Capital Flows. With US Treasury yields anchored high, the yield premium that Vietnam and other emerging markets must offer to attract foreign capital becomes more expensive. Foreign investor net selling in Vietnam's equity market has been a persistent trend. The expected FTSE Emerging Markets inclusion in September 2026 could partially reverse this dynamic, but the timeline and magnitude depend heavily on where the dollar and US yields stand at that point.

Savings Rates and the Cost of Capital. The Big Four banks currently offer 5–5.5% per year on 12-month deposits; smaller banks are at 7–8%. With exchange rate pressure still present, the State Bank's room to cut further is constrained. At current levels, fixed deposits at major banks are approximately on par with the year-to-date returns of some open-ended bond funds in Q1, meaning fixed-income instruments retain meaningful relative attractiveness.

Risk Asset Valuations. High US yields pull down the valuation floor for Vietnamese equities relative to the low-rate era. Gold is moving in the opposite direction: XAUUSD closed at $4,590.58/oz on May 4, up approximately 37% versus 12 months earlier; SJC gold (retail selling price) recently hit VND 168.8 million per tael, up roughly 41%. Real estate faces a dual squeeze: elevated mortgage rates compress demand while highly leveraged developers bear heavier financing costs.

A Portfolio Framework for the New Rate Environment

In a "higher for longer" rate environment, a few allocation principles become more relevant than they were in the 2010–2020 cycle.

Fixed-income instruments deserve meaningful weight. Deposit rates at major banks and open-ended bond funds currently yield 5–7% per year. That is not a low return when Vietnamese CPI is running around 4.65%. Gold warrants a 5–10% allocation as a hedge against exchange rate volatility, a range commonly cited for environments with elevated currency risk. For equities, the priority is businesses with low USD-denominated debt and margins wide enough to absorb higher financing costs; highly leveraged sectors sensitive to domestic rates are worth underweighting.

The VN-Index closed at 1,854.06 on May 4. Current valuation levels support selective accumulation of fundamentally sound names. The difference from the low-rate era is that sector and company selection matters far more: rising liquidity no longer lifts most boats.

Two signals are worth watching closely in the coming week: whether USD/VND holds or breaks above 26,400, and whether the next Fed communications shift the 2026 dot-plot projections. Those two data points will do more to shape six-month rate expectations than any single quarterly earnings release.