On May 2, 2026, Spirit Airlines ceased all operations after 34 years, after a last-minute deal for a $500 million government rescue loan collapsed under the Trump administration. The airline's largest creditors — including Citadel, led by Founder and CEO Ken Griffin, alongside Ares Management and Cyrus Capital — voted against the bailout plan, reasoning that the government loan would rank senior to their existing claims in the debt structure. With that vote, a 34-year-old carrier, 17,000 employees, and what was once a symbol of the American ultra-low-cost model came to an end in a single day.CBSNews

That same week in Vietnam, VietJet reported Q1/2026 results running in the opposite direction: consolidated revenue of VND 21,021 billion, up 17.1% year-on-year, and consolidated net profit after tax of VND 1,023 billion, up 59.6%. The airline carried 7.2 million passengers across 39,903 flights.VnEconomy VJC shares closed the April 29 session at VND 180,000 per share, giving the company a market cap of VND 106.5 trillion.

Both carriers share the "budget airline" label. Same week, opposite outcomes. The real question is not whether VJC is completely risk-free (it is not). The question is: which three structural axes actually determine whether a low-cost carrier survives a difficult cycle, and where does VietJet stand on each axis compared to Spirit?

Axis 1: Saturated Market vs. Room to Grow

The data on market penetration tells the story clearly.

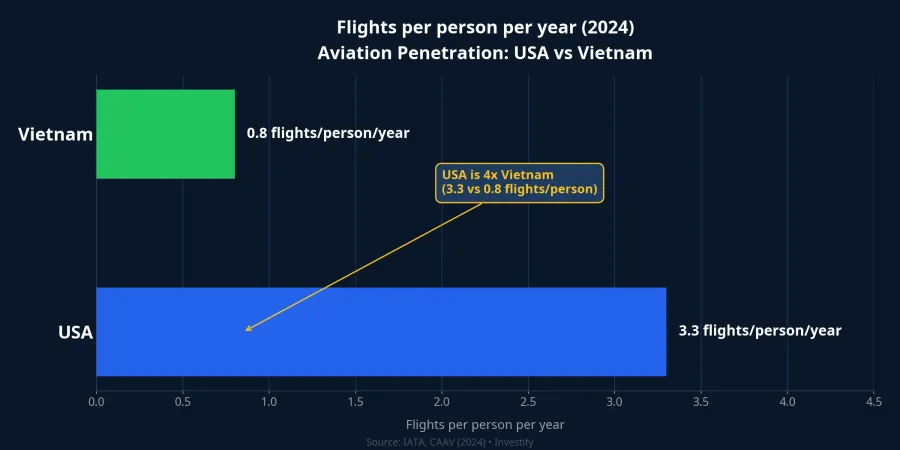

The United States has been a mature aviation market for more than three decades. Total passenger traffic in 2024 exceeded 1.1 billion trips on a population of around 333 million, equivalent to more than 3.3 flights per person per year. At that level of saturation, there is no new market left to open. Spirit had to compete directly with Frontier, Allegiant, and the low-cost arms of Delta, United, and American. All of them were fighting on a price floor already compressed to razor-thin margins. No carrier in that environment can escape the pricing trap by repositioning alone.

Vietnam sits on the opposite side of the curve. Total passenger traffic in 2024 came to around 76.4 million on a population of 98.5 million: fewer than 0.8 flights per person per year, or roughly a quarter of the U.S. rate. Terminal 3 at Tan Son Nhat and the new Long Thanh airport are in their final development phase, with plans to bring total network capacity close to 300 million passengers by 2030.VnEconomy Vietnam's relaxed visa policy continues to attract international arrivals. VietJet currently operates 186 routes, and expanding international frequency was its primary growth lever in Q1/2026. That is growth driven by a market expanding around the airline, not growth squeezed from competitors' share.

The structural gap on this axis is straightforward: Spirit had to generate profit in a contracting market; VJC has meaningful room to grow revenue without forcing margins lower on rivals.

Axis 2: Fuel Cost Structure and Flexibility

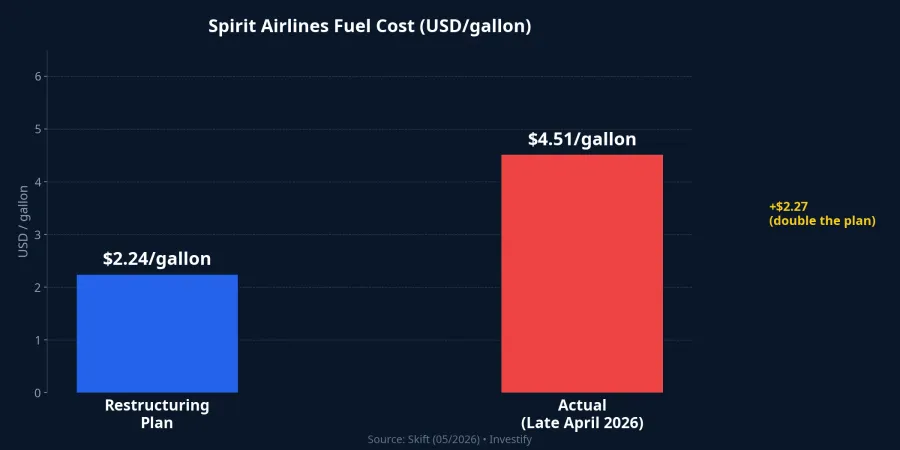

This is where Spirit's restructuring plan unraveled in the most literal sense.

In its post-bankruptcy restructuring plan, Spirit projected jet fuel at approximately $2.24 per gallon.Skift The actual cost by late April was $4.51 per gallon — double the base assumption — after Iran-related tensions drove Brent crude to a peak of $126 per barrel around April 30. Fuel accounts for 35–40% of a low-cost carrier's total operating costs. When the single largest line item exceeds the assumption by a factor of two, no recovery scenario remains viable.

VietJet faced the same Brent shock, but with two structural advantages. First, its fleet of Airbus A320neo and A321neo aircraft consumes roughly 15–20% less fuel per flight than the previous generation. The same price-per-barrel increase translates into a proportionally lower cost increase. Second, when Jet A-1 reached the VND 190,000–234,000 range per barrel in April, VietJet proactively cut 18% of its capacity, adjusting its operating scale to match the fuel environment rather than maintaining a fixed schedule as Spirit had done. Brent has since pulled back to around $110 per barrel as tensions eased, relieving part of the pressure.

The structural contrast on this axis: Spirit was locked into a low-fuel assumption and had no operational flexibility to adjust; VJC retained control over both unit cost and operating scale.

Axis 3: Liquidity Buffer Through a Down Cycle

This is the decisive axis, and the gap between the two carriers is widest here.

Spirit filed for bankruptcy twice within 18 months: first in November 2024, then again in August 2025. By April 2026, its senior debt stack had become so dense that creditors concluded their recovery value would actually be lower if the government loan ranked ahead of them. That calculation is what led Ken Griffin's Citadel and Ares Management to vote against the bailout despite a U.S. government backstop: more cash into the structure would not rescue the airline; it would only dilute existing creditors' recovery.Travel Market Report

VietJet entered Q1/2026 with a current ratio of 1.5x: current assets covering current liabilities with a 50% buffer. Total assets exceeded VND 143,534 billion, with a net debt-to-equity ratio of approximately 2.1x. That leverage is not low by sector standards, but it comes with positive operating cash flow and net profit up 59.6% year-on-year. When an airline can generate VND 1,023 billion in profit during a quarter of elevated fuel prices, its creditors have no reason to hold a vote on whether to rescue it.VnEconomy

The structural contrast on this axis: Spirit needed external rescue; VJC can service its short-term obligations from its own operating cash flow.

What the Three Axes Mean for VJC Shareholders

Placing all three axes side by side, the conclusion is not that VJC is immune to risk. VJC shares carry full cycle risk: Brent volatility, airport infrastructure bottlenecks, and rising competitive pressure as more carriers return to market in 2026.Tien Phong

What matters is the nature of that risk. VJC faces margin risk: profits could compress if Brent rises again. Spirit faced existential risk: the inability to service its debt. These are fundamentally different categories of risk, even though both carriers carry the same industry label.

Three signals are worth watching over the coming weeks. First, whether Brent holds near $110 per barrel or moves back toward $120+ as geopolitical tensions shift. Second, VJC's May capacity deployment after the 18% April cut: the pace of recovery will reveal how effectively the airline can scale up and down. Third — and most important for long-term holders — the infrastructure execution variable: VJC's growth trajectory depends on T3 Tan Son Nhat and Long Thanh delivering on schedule. That is a third-party execution risk outside the airline's control.

News of Spirit's closure may weigh on global airline valuations for a few sessions, with sentiment spillover potentially reaching VJC. If the three structural axes described above have not changed, any resulting discount in VJC's share price reflects sentiment, not fundamentals. Q2 results will be the next real test of that thesis.