The instinct to buy Petrolimex (PLX) stock when fuel prices rise is not entirely unreasonable. PLX's revenue is tied to fuel volumes sold, and higher prices inflate the absolute numbers on the income statement. The problem is that this logic skips a fundamental detail. Q1/2026 just tested it with a concrete figure.

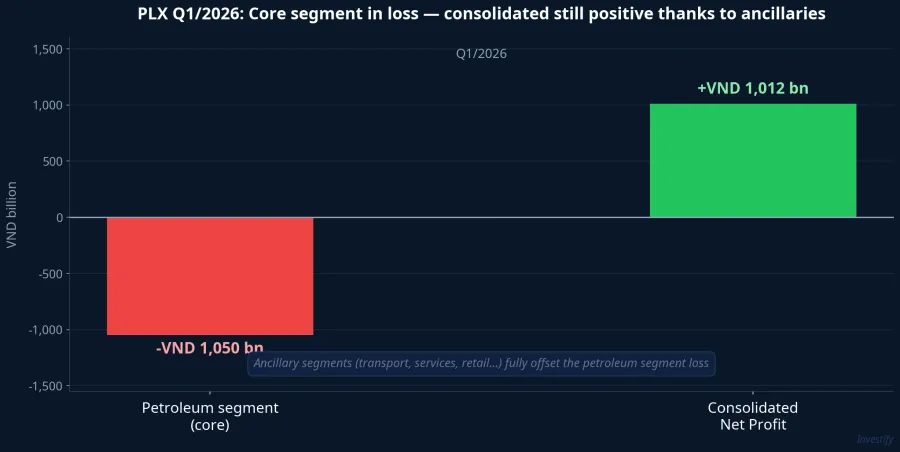

At the 2026 Annual General Meeting of Shareholders (AGM) on April 24, Petrolimex's CEO Lưu Văn Tuyển confirmed that the company's petroleum distribution segment recorded an estimated loss of over VND 1 trillion in Q1, in the same quarter when domestic retail fuel prices saw their sharpest swings since 2024.Vietstock To understand how both can happen simultaneously, you need to read PLX through the lens of the business model it actually operates.

Key Numbers from the April 24 AGM

Looking at the reported figures: Petrolimex's consolidated pre-tax profit for Q1/2026 came in at approximately VND 1,012 billion, meaning it remained positive. But the segment breakdown tells a different story. The loss of over VND 1,000 billion was concentrated entirely in the petroleum distribution segment, which accounts for the overwhelming share of the group's revenue. The offsetting contribution came from transport, services, non-network retail, and financial items.

CEO Lưu Văn Tuyển attributed the loss to international oil price volatility described as "unprecedented": prices moved 20–50 USD per barrel per day, with international diesel briefly reaching 292 USD per barrel in March before retreating to around 140 USD by April.CafeF Import surcharges jumped from approximately USD 25–26 million to USD 85–87 million per 40,000-ton vessel.Vietnambiz

Why the Loss Happened: It's About Speed, Not Price Level

What many investors miss is that PLX does not set its own prices. Domestic retail fuel prices are regulated under Decree 80/2023, with adjustment cycles every Thursday (approximately every 7 days). The Ministry of Industry and Trade publishes a reference base price derived from import reference costs, standard expenses, regulated margins, and taxes. PLX sells at that price, not at a free-market rate.

The key mechanism is the lag. When international prices move 20–50 USD per barrel per day, the distributor must source inventory at spot market prices immediately. But the domestic selling price can only be adjusted on the next scheduled cycle, 7 days out. That gap, multiplied by 20–25 days of inventory on hand, creates the loss: costs enter the books first, revenue adjustments follow later. Across a quarter when international prices swung by those magnitudes, the accumulated lag becomes a trillion-dong figure.

This is the structural difference from upstream players like PVD or GAS, or refiners like BSR. Those businesses sell at market prices or operate under different pricing frameworks. PLX is closer to a utility model: relatively stable regulated margins when the market is calm, in exchange for sharply compressed margins when there is a price shock. The company absorbs inventory risk and timing lag on behalf of consumers to keep retail prices stable. The Price Stabilization Fund is the mechanism designed to support that arrangement.

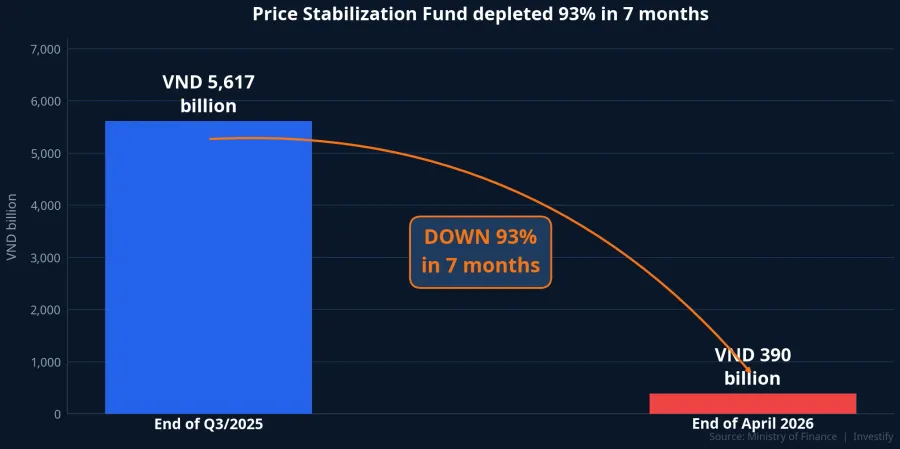

The Price Stabilization Fund: Almost Depleted

The Petroleum Price Stabilization Fund (BOG) operates through a contribution-and-disbursement mechanism. When international prices spike, the regulator draws from the fund to reduce the pace of retail price increases, with that disbursement flowing directly to distributors. When prices fall, contributions are collected.

The data here is telling. As of the end of Q3/2025, the fund balance stood at VND 5,617 billion.Báo Chính phủ By April 29, 2026, the balance had fallen to approximately VND 390 billion, a roughly 93% contraction in just 7 months as continuous disbursements were made to cushion retail prices from rising international costs. If a similar price shock recurs in the coming quarters, the intervention buffer is essentially gone.

The practical implication: in previous volatility episodes, the BOG fund could absorb pressure for both consumers and distributors. With the current balance at approximately VND 390 billion, that capacity no longer exists at meaningful scale. If another shock arrives before the fund is replenished, distributors will bear the full margin burden, or retail prices will need to rise by the full underlying amount.

Market Reaction and the 2026 Plan

The stock price reaction was unambiguous. On the day of the AGM, April 24, PLX closed at VND 39,700 per share. On the first trading session after the holiday break, April 28, the stock fell 6.93% to VND 36,950 per share on volume of 6.5 million shares, nearly triple the preceding average.

The management's 2026 plan reinforced the cautious signal: revenue of VND 315,000 billion (up approximately 2% versus 2025), consolidated pre-tax profit of VND 3,380 billion (down approximately 7% versus 2025), and fuel sales volume of 19.4 million tonnes (up approximately 10%). Planning for higher volumes alongside lower profit is a clear indication that per-unit margins are compressing, and management does not expect a near-term reversal.

Reading PLX Through the Correct Framework

When analyzing PLX, the two key variables are not simply the Brent price level. The first is the amplitude and speed of international price swings within each 7-day regulation cycle: Brent at elevated but stable levels (within 5–10 USD per day) allows PLX to operate near normal regulated margins; Brent swinging 20–50 USD per day as in Q1/2026 is a loss-generating environment. The second is the remaining capacity in the Stabilization Fund relative to what would be needed to buffer the next shock cycle.

Positive consolidated profit in Q1/2026 is worth noting, but needs to be placed in proper context. The ancillary segments were just sufficient to keep the consolidated figure from going negative during a shock quarter. They are not large enough to drive a positive revaluation of the group as a whole. The structural risk sits in the core segment, and a VND 1,000 billion loss there is a structural signal, not a technical one-off.

Three Signals to Watch Heading Into Q2

Three developments are worth tracking for anyone following PLX. First, the situation in the Strait of Hormuz and US–Iran negotiations: this is the root driver of international price volatility amplitude.VOV Brent returning to a narrower daily trading range would reduce pressure on regulated margins. Second, the official Q1/2026 financial statements when released will provide clearer segment-level data and show whether Q2 recovery is on track. Third, upcoming price adjustment sessions and Stabilization Fund contribution levels: whether the fund is replenished as international prices soften will determine how much buffer remains for future volatility episodes.

For a stock operating under government-regulated pricing during a period of elevated geopolitical uncertainty, the right analytical question is not "is the fuel price rising?" but "is the volatility narrow enough for the regulated-margin model to function normally?" The official Q1 report and the next few pricing sessions will provide the most direct answers.