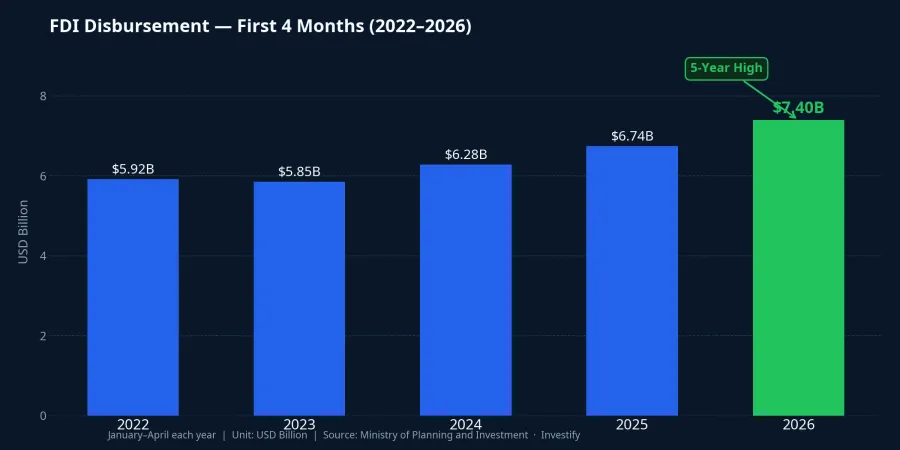

In the first four months of 2026, realized foreign direct investment in Vietnam reached an estimated USD 7.4 billion, the highest January-April reading in five years, up 9.8% year-on-year.Baomoi This is not pledged capital on paper. This is money that has already flowed into factories, construction sites, and operational production lines. At the same time, industrial park stocks on the Vietnamese exchanges gave a decidedly mixed picture: KBC gained over 6%, while VGC lost nearly 10% and IDC fell more than 8%. The big picture shows foreign capital accelerating clearly into Vietnam. But the market is rapidly sorting out who actually benefits.

Singapore Leads with USD 6.05 Billion

Through April 27, 2026, total registered FDI — covering new registrations, capital adjustments, and equity contributions — reached USD 18.24 billion, a 32% increase year-on-year.VOV Among new capital registrations, Singapore led decisively with USD 6.05 billion, capturing nearly 49.8% of newly registered capital from 53 countries and territories.VOV South Korea ranked second at USD 4.08 billion (33.6%), a significant distance behind Singapore.

Equity contributions and share acquisitions by foreign investors also accelerated sharply: 976 transactions totaling USD 2.96 billion, up 61.9% year-on-year.Baomoi This channel routes foreign capital directly into listed or OTC companies without requiring new project approvals. The 61.9% surge suggests foreign investors are gaining footholds in Vietnam's capital markets significantly faster than through direct project registrations alone.

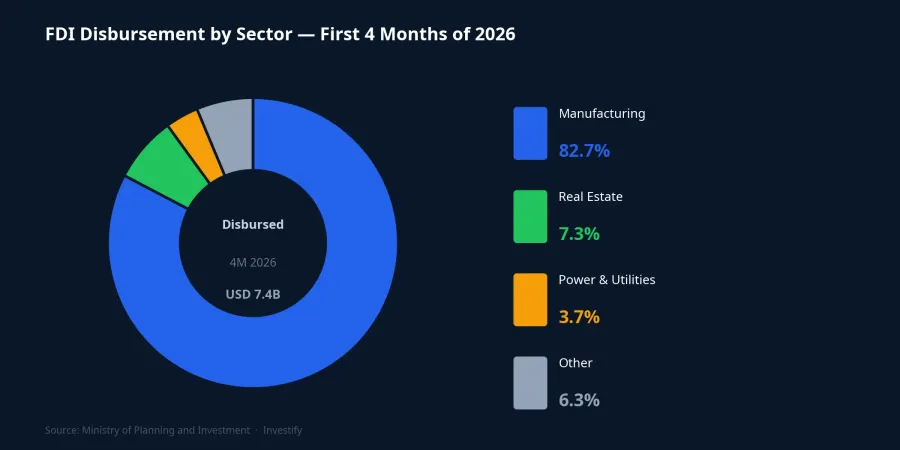

82.7% into Manufacturing: What the Money Is Buying

The sector breakdown of disbursements reveals precisely which industries foreign investors are choosing. Manufacturing led with USD 6.12 billion out of the total USD 7.4 billion disbursed, equivalent to 82.7%.Baomoi Real estate ranked second at USD 540.5 million (7.3%), followed by power and utilities at USD 270.6 million (3.7%).

On the new-registration side, manufacturing also captured USD 8.12 billion (66.8%).VOV The gap between 82.7% in disbursements and 66.8% in new registrations tells a clear story: current execution is being driven by projects licensed in prior years that are now entering construction and equipment procurement phases. This is the most committed layer of FDI capital: less reversible than financial or trade flows, and directly tied to industrial land demand over the next several years.

Named Projects: Data Centers, VSIP, and Semiconductors

Singapore's capital is going into specific, named projects, not abstract figures. In Ho Chi Minh City, three Singaporean investors — Hathor, Frontier, and Evolution — were awarded investment certificates for the Evolution DC VN HCM project, a hyperscale carrier-neutral data center with a total investment of USD 508.78 million and an IT capacity of 52 MW.Vietstock In the same licensing round, the STARMASON project at USD 480.26 million and Uptime Tier III+ certification also received approval. Together, the two projects represent nearly USD 1 billion in digital infrastructure, entirely Singapore-sourced.

In Bac Ninh province, following VSIP I and VSIP II whose combined area exceeds 900 hectares,CafeF Singapore is studying the groundbreaking of VSIP III this year, with a target of bringing Vietnam's total VSIP count to 30 by end-2026.Baomoi In semiconductors, Samsung is evaluating a multi-phase expansion in Thai Nguyen that could total USD 4 billion according to Bloomberg reporting.Baomoi If realized, this would be Samsung's largest semiconductor investment in Vietnam to date.

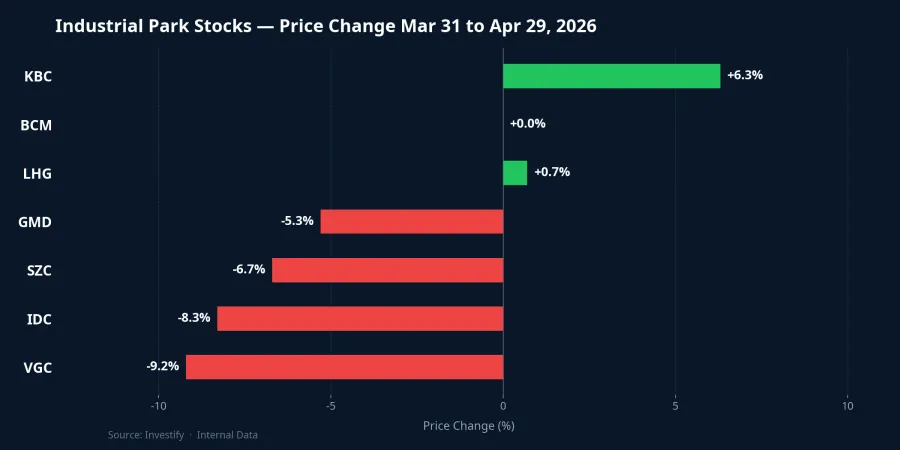

Industrial Park Stocks: Three Distinct Tiers

This is where investors need to read carefully. FDI is flowing in strongly, but April's industrial park stock prices did not move in unison.

From the March 31 close to April 29, 2026, KBC rose from VND 31,900 to VND 33,900, up 6.3% for the month. BCM was virtually flat, moving from VND 53,100 to VND 53,200. LHG edged up 0.7% within the VND 28,250–28,450 range. On the negative side, IDC fell from VND 49,300 to VND 45,200, dropping 8.3%. SZC corrected 6.7%. VGC slid from VND 46,900 to VND 42,600, losing 9.2% and finishing as the worst performer in the group. GMD, representing the logistics chain serving manufacturing FDI, fell from VND 79,500 to VND 75,300.

Capital flows are sorting these stocks into three tiers. The first tier consists of companies with ready land in provinces directly in line for VSIP III and semiconductor expansion: KBC, with its large industrial land bank in Bac Ninh, was valued higher by the market this month. The second tier includes companies that already ran ahead of the FDI story and are now digesting their valuations: BCM, IDC, and VGC all ran earlier, and the market is now recalibrating expectations. The third tier is the export logistics chain. GMD is facing near-term pressure from freight market volatility and elevated oil prices. This is a timing issue, not a business fundamentals issue. The divergence does not contradict the FDI narrative. It shows the market processing information position by position rather than buying the sector uniformly, as it did during the initial expectation-building phase.

Registered Up 32%, Disbursed Up 9.8%: Reading the Gap Correctly

Registered FDI growing 32% while disbursements grow 9.8% is not a sign of weak execution. There are three more precise explanations. First, high-tech and semiconductor projects have long lead times — from land clearance to equipment import — meaning 2026 registrations will largely disburse in 2027 and 2028. Second, the 61.9% surge in equity contributions shows foreign investors entering through the capital markets faster than through ground-level project development.Baomoi Third, regulators are tightening progress verification before approving further disbursements, which reduces the risk of projects stalling, a net positive for long-term capital quality.

For investors, this gap has two practical implications. Industrial park stocks with ready land and signed contracts are supported by actual disbursement flows today. Stocks priced to benefit from the new registration wave will need to wait another four to eight quarters before those projects generate real rental revenue.

Risks to Watch

Three risk factors warrant monitoring. Singapore and South Korea together account for 83.4% of newly registered capital. Vietnam is running a two-source dependency, and a strategic shift by either party would be material. Rising USD/VND exchange rate pressure could slow disbursement timelines for projects importing equipment priced in USD. Finally, manufacturing's 82.7% share of disbursements creates concentration risk: if global supply chains encounter a serious disruption, this capital stream is more likely to be redirected than infrastructure or energy FDI.

Signals to Track in May

VN-Index closed April at 1,854.10 points, less than 3% below the 1,877–1,900 resistance band. Early May money flows are likely to rotate around three groups directly tied to the FDI story: industrial park stocks with land banks in provinces positioned for VSIP III and Samsung expansion; the export-serving logistics chain including GMD and HAH; and construction material suppliers for the new wave of groundbreakings such as VGC and HT1.

The real test comes in Q2 2026. If disbursements maintain growth above 9% per quarter and VSIP III in Bac Ninh officially breaks ground, industrial park stocks with ready land have a genuine basis to transition from expectation-driven pricing to actual rental revenue. The bear scenario materializes if the USD/VND rate rises further or global supply chains face a harder disruption, pushing some registered projects to delay execution. Two specific signals to watch: the Q2 FDI disbursement figure due for release at the end of July, and official updates on VSIP III timelines from the Bac Ninh Industrial Zone Management Board.