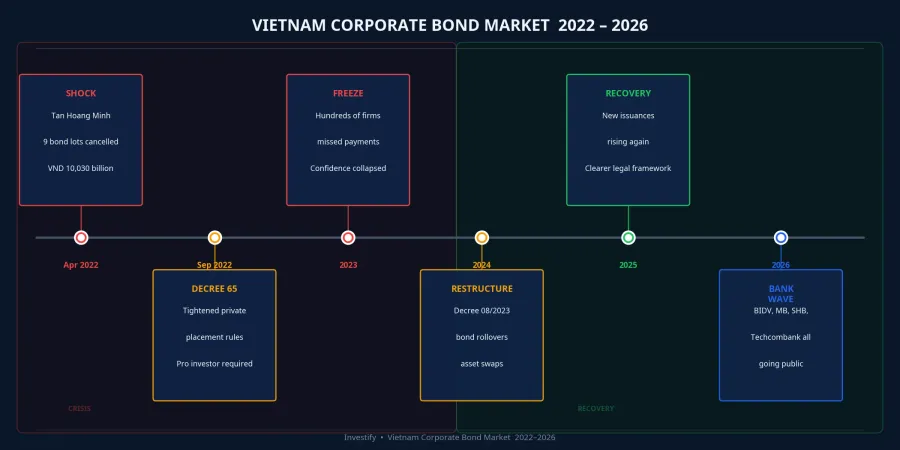

In April 2022, Vietnam's Ministry of Finance cancelled nine bond lots issued by Tan Hoang Minh Group, worth more than VND 10,000 billion.VnExpress For many individual investors, it was the first time they experienced what had only ever appeared in fine print: corporate bonds can be cancelled, and money does not automatically return. Months later, the Van Thinh Phat scandal exposed tens of trillions in bonds that had been distributed to ordinary retail investors through securities firms. Confidence collapsed.

Four years later, in early May 2026, the bond market opens a new wave. This time, the issuers are different: BIDV, MB, SHB, and Techcombank — not real estate developers. The issuance mechanism is different too. Understanding why this is a genuinely positive signal — and why careful reading still matters — comes down to three key points.

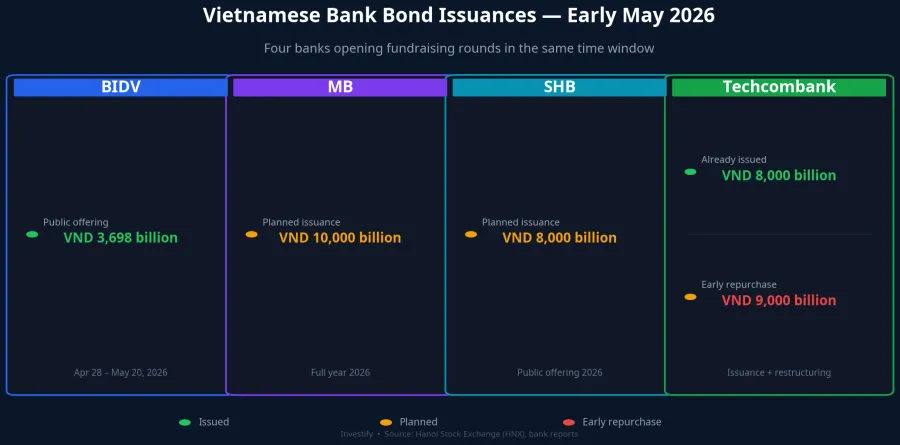

Four Banks, One Time Window

BIDV is running a public bond offering of VND 3,698 billion from April 28 to May 20, 2026, split across three bond codes with terms of 7, 8, and 10 years.Baomoi Interest rates are floating, set at a reference rate plus a margin of 1.8% to 1.9% per annum, paid semi-annually. The minimum purchase is just VND 10 million, meaning ordinary retail investors can participate. The stated purpose is to supplement Tier 2 capital and meet lending demand.

MB has approved a plan to issue up to VND 10,000 billion in bonds during 2026.DNSE SHB has received approval for a public offering of up to VND 8,000 billion, with the first tranche expected in Q2–Q3 2026, 7-year term, floating rate referenced to state-owned bank deposit rates plus a fixed margin of 3.3% per annum.Tinnhanhchungkhoan

Techcombank chose a different approach: it issued approximately VND 8,000 billion in bonds during April while simultaneously planning to repurchase up to VND 9,000 billion in existing debt in May. Some bond codes carry a fixed rate of 8.5% per annum, with two-way early repurchase clauses.DNSE

Four banks, four distinct strategies, all in the same time window. What is driving this simultaneous wave?

Why Now

The simplest way to understand the timing is to ask one question: if a bank takes short-term deposits (1, 3, 6 months) but lends to businesses for 5 to 10 years, how does it bridge that gap? The answer is long-dated bonds. That is the core driver.

On top of that, Basel III capital standards, being phased in from 2025, require banks to maintain higher capital adequacy ratios (CAR). 7 to 10-year bonds are the natural instrument for supplementing Tier 2 capital. BIDV and SHB both stated this purpose explicitly in their issuance documents.

Interest rate timing adds another reason to act now. The State Bank of Vietnam's policy rate has been at 4.50% per annum since March 2026,SBV while CPI for March 2026 came in at 4.65% year-on-year — the highest in five years.Thanh Nien With inflationary pressure still present, banks have reason to lock in long-term funding before deposit rates potentially edge higher in the second half of 2026.

These pressures are not new for any individual bank. What is unusual is that all of them reached a tipping point in the same quarter. That explains why the issuance wave is happening simultaneously rather than in isolation.

How the Legal Framework Changed Since 2022

This is the most important part for understanding why 2026 is different.

Tan Hoang Minh bonds and most real estate corporate bonds issued from 2020 to 2022 were private placements: in principle restricted to professional investors, but in practice investor qualification checks were loose, and securities firms distributed them to ordinary retail investors. Disclosure documents were thin and the use of proceeds was vague.

BIDV's current offering is a public offering: it requires approval from the State Securities Commission, comes with a full prospectus, credit rating requirements apply above certain sizes, and ongoing periodic disclosure is mandatory. The door is open to retail investors by design. The key difference from 2022 is not the interest rate or the term — it is the level of oversight and information transparency.

Decree 65/2022 and its 2024–2025 amendments tightened private placement rules: professional investors must now maintain a minimum portfolio of VND 2 billion for 180 consecutive days, credit ratings are mandatory for certain bond categories, and use-of-proceeds disclosure requirements are more detailed. The result is a structural shift in the market: in Q1 2026, real estate bonds accounted for approximately 61% of total corporate bond issuances — mostly still via private placement — while banks accounted for around 29%, leading the public offering channel.Tinnhanhchungkhoan

In simple terms: the private placement channel is being tightened, while the public offering channel is being expanded. The bank bond wave in early May is a product of that expansion.

Three Things to Understand Before Deciding

With a minimum investment of VND 10 million, BIDV's offering is accessible to many investors approaching bonds for the first time. But the prospectus contains several decision-critical points that deserve careful reading rather than a quick scan.

One: What is the reference rate? The 1.8% to 1.9% margin is the add-on. The question is: added to what? Most bank bonds reference the 12-month deposit rate at Big4 banks or the average across state-owned banks. When market savings rates fall, the bond's coupon falls with them. This is a fundamental trade-off compared to fixed-rate bonds like some of Techcombank's codes at 8.5% per annum: the fixed rate offers more certainty, but you will not benefit if market interest rates rise.

Two: Effective maturity versus stated maturity. The 7 to 10-year term is what appears on the prospectus. The early repurchase clause determines how long you actually hold the bond. Check: who holds the repurchase right, how much advance notice is required, and under what conditions the bank can exercise early repurchase unilaterally. When market rates fall, banks may repurchase to reissue at a lower cost. You lose the yield you had counted on.

Three: Secondary market liquidity. Public offering bonds can be traded on the secondary market, but the depth of trading varies significantly by bond code. In an emergency, you may not be able to sell quickly at your expected price. The safest approach is to decide upfront: this is money I am comfortable holding to maturity, not money I may need on short notice.

What This Wave Tells Us

Over four years since the 2022 shock, Vietnam's corporate bond market has moved through multiple phases: cancellations, a freeze, regulatory overhaul, debt rollovers under Decree 08/2023, and then a gradual shift in the composition of issuers. Banks have emerged as the leading channel for public bond offerings — not because the real estate sector disappeared, but because the public offering channel has been expanded and retail investors are only returning to issuers subject to the strictest oversight.

BIDV's offering remains open until May 20, 2026. That is roughly two weeks: enough time to read a prospectus carefully. Three things worth checking: how the reference rate is defined specifically, which party holds the early repurchase right, and what the bank's current CAR is. No collateral means the primary repayment source is the bank's own balance sheet. For BIDV and Techcombank, that is a risk the market prices low — but not at zero.

Signals worth watching in May: the subscription rate relative to BIDV's total issuance volume, and how subsequent tranches from MB and SHB perform. If public offering rounds attract strong demand, it will be a meaningful signal that retail investor confidence in bank bonds is genuinely returning.