Many depositors carry a natural assumption: when prices rise sharply, banks will lift deposit rates to compensate. Historically, that assumption held. The inflation spikes of 2011 and 2022 pushed 12-month deposit rates as high as 9–10% per year, giving savers a reasonable buffer against rising prices. But as May 2026 opens, the data tells a different story.

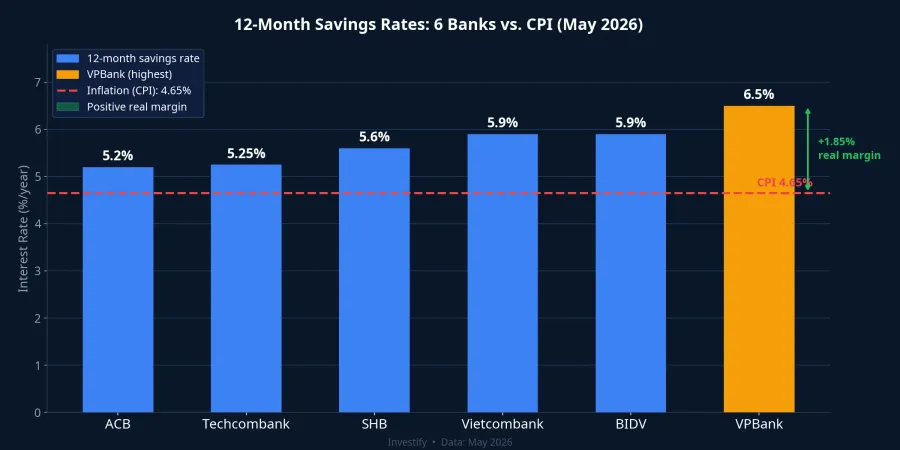

March 2026 CPI rose 4.65% year-on-year, the highest reading in five years, driven by an 12.85% jump in transport costs and domestic fuel prices climbing in the wake of Middle East tensions.Báo Văn hóa April CPI has not yet been published, but import fuel prices have not eased meaningfully, so price pressure remains. Yet the May rate cards from banks are moving in the opposite direction. Vietcombank and BIDV have set their 12-month term rate at 5.9% per year, with BIDV cutting 0.8–0.9 percentage points across the 6–12 month tenors versus its previous schedule.Nhịp sống KD VPBank trimmed another 0.3–0.5 percentage points on its online channel, and Techcombank cut 0.5 percentage points across the 6–36 month range.Tạp chí KTTC

Put simply: the number in your passbook keeps growing every month, but what that money can actually buy — your purchasing power — is shrinking. The question that matters more than the nominal rate is: once you subtract inflation, how much are you actually preserving?

Why Deposit Rates Fall When Inflation Rises

Understanding the answer means you will not be surprised by the next round of rate adjustments. Banks do not price deposit rates based on their customers' inflation expectations. Three separate constraints govern that decision.

The central bank constraint. On March 30, 2026, the State Bank of Vietnam (SBV) issued Official Letter 2342/NHNN-CSTT, instructing credit institutions to stabilize interest rates and accelerate credit growth.Tin nhanh CK The full-year credit growth target is approximately 15%, but Q1 2026 credit expanded only 3.18%. Delivering the remaining volume over nine months requires pushing lending rates lower. When the output rate falls, the input rate must follow.

The net interest margin (NIM) constraint. When lending rates are compressed downward, banks must lower funding costs to protect NIM; otherwise the spread cannot cover provisioning and operating expenses. Cutting deposit rates by 0.5 percentage points is the most straightforward way to defend the margin when lending revenue is being squeezed.

The liquidity constraint. Credit grew only 3.18% in Q1 2026 while deposits kept flowing in, particularly from corporate clients after the year-end payment cycle. When funding supply exceeds loan demand, banks have no competitive reason to maintain high deposit rates to attract more money.

All three constraints push in the same direction, independently of what CPI is doing. That is why deposit rates can fall while inflation rises without contradicting any banking logic. Only the depositor's expectation is violated, not the bank's operating model.

Quantifying the Real Margin

The simplest calculation: deposit rate minus CPI equals real margin.

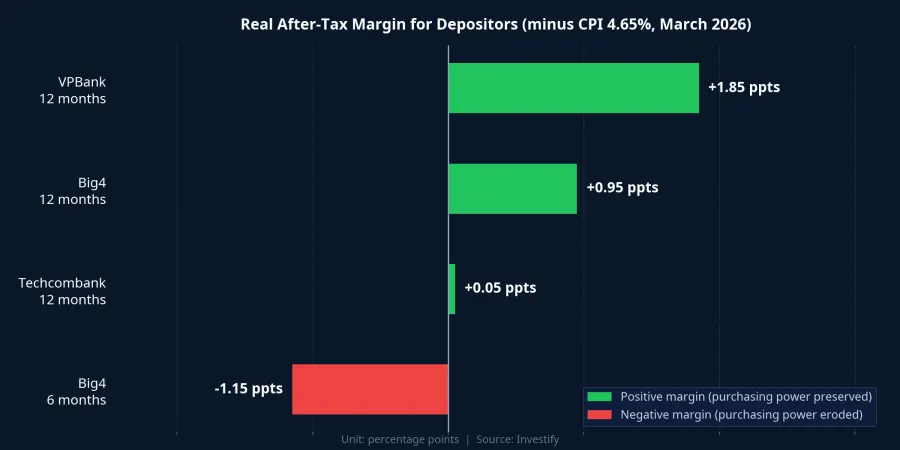

Big4 12-month rates at 5.9% per year minus CPI of 4.65% leaves a nominal real margin of 1.25 percentage points. After the 5% personal income tax on interest, that figure narrows to approximately 0.95 percentage points. Not a loss, but an extremely thin buffer.

Looking across six banks, the picture breaks down further.

Depositors in Big4 6-month accounts, where rates sit around 3.5% per year, are running a real margin of negative 1.15 percentage points. Every month that money stays in a 6-month Big4 passbook, purchasing power quietly erodes, even though the nominal balance keeps rising. Techcombank's 12-month rate of 5.25% per year produces roughly 0.05 percentage points of real margin, effectively breakeven after tax. VPBank's 12-month rate of 6.5% per year delivers the widest real margin in the comparison at 1.85 percentage points, but carries a higher risk and volatility profile than the state-owned banks.

The trajectory is worth noting: roughly three years ago, Big4 depositors received a real margin of around 2–3 percentage points. That has been cut in half, with no clear reversal signal on the horizon.

There is also a widely-missed implication: keeping money in short-term accounts for "flexibility" carries a hidden cost in the form of steady purchasing power erosion. The nominal balance grows, but its real value is shrinking faster than the interest being added.

Fixed-Income Channels That Are Paying More

The natural follow-up question: if bank deposits are no longer preserving purchasing power well, what options do Vietnamese retail investors have at a comparable risk level?

Open-ended bond funds are the closest substitute to bank deposits in terms of NAV volatility. Funds such as TCBF (Techcom Bond Fund) and VFFB (VinaCapital Fixed Income Fund) have typically delivered returns in the range of 5–7% per year under normal market conditions, with daily liquidity on business days through a T+3 redemption cycle. Management fees of approximately 0.8–1.0% per year are already deducted before the published yield figure. Real margins are meaningfully wider than Big4 short-term deposits while maintaining reasonable liquidity.

Bank-issued certificates of deposit (CDs) typically pay 0.3–1.0 percentage points more than a standard passbook at the same institution for the same tenor. The trade-off is that CDs are not covered by deposit insurance the way passbooks are, and early redemption is more restricted. For depositors who are confident they will not need the funds before maturity, this is a rational upgrade.

Listed corporate bonds offer yields in the approximate range of 8–11% per year for issuers with solid credit profiles and clear collateral arrangements. The trade-off is genuine credit risk. Post-Decree 65/2022, the market has been significantly tightened, but investors still need to read offering documents carefully and understand the collateral structure before committing. Best suited to those who can hold to maturity.

Fintech fixed-income products typically advertise fixed yields around 9–11% per year, linked to portfolios of bonds or restructured receivables. The advantage is regular interest cash flows and pre-disclosed risk parameters. Before investing, it is essential to verify the issuing entity's credentials and understand the underlying asset structure.

In practical terms: compared to the roughly 1.25 percentage point nominal real margin of a Big4 12-month deposit, these channels can offer real margins of approximately 1–6 percentage points. That gap is large enough to make the case that allocating a portion of idle funds toward non-bank fixed-income channels is a structural portfolio decision, not a market bet.

A Framework for Current Depositors

The belief that "rising inflation leads to higher deposit rates" was accurate in monetary cycles when the SBV used interest rates as a tool to fight inflation, with 2011 and 2022 as the clearest examples. The current cycle operates on different logic: the SBV is prioritizing credit growth support, pushing lending rates down, and deposit rates are being pulled along for the ride. Depositors' inflation is not the variable the bank optimizes for. It is the final subtraction savers must absorb on their own.

For the portion of funds needed for absolute liquidity over the next three to six months: keeping money in Big4 savings accounts remains the right call, even with a negative real margin at short tenors. The cost of that liquidity option is real, but appropriate when immediate access to cash is a hard requirement.

For idle funds with a six-to-twelve-month-plus horizon: a 1 percentage point real margin at Big4 is no longer optimal when open-ended bond funds and other fixed-income channels are offering 5–11% per year with quantifiable risk. Specific allocation percentages depend on individual risk tolerance, but keeping 100% of investable savings in Big4 deposits in the current rate environment comes with a significant opportunity cost.

Signals worth watching over the next four to six weeks: April 2026 CPI data expected in mid-May, credit growth figures for May and June, and rate cards from major private-sector banks. If credit growth recovers sharply toward the 15% target, system liquidity will tighten and the downward drift in deposit rates could pause. Until that signal arrives, the deposit rate floor is still tilting lower.