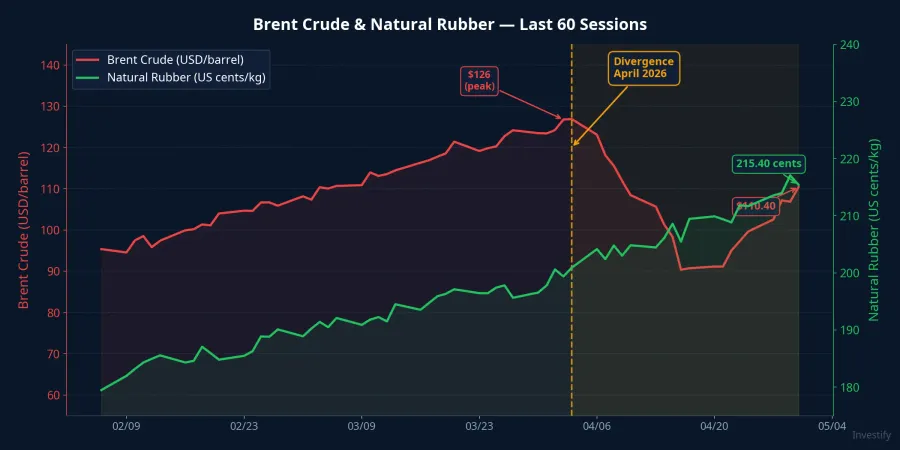

On April 30, Brent crude closed at $110.40 a barrel — still elevated, but well below the $126 peak reached before US President Donald Trump sent Congress a statement declaring that hostilities with Iran had terminated.PBS NewsHour Markets read the geopolitical signal and priced in a partial de-escalation. On that same session, natural rubber futures stood at 215.40 US cents per kilogram — the highest level since February 2017. Nearly nine years of history at a single data point.

Oil and rubber are supposed to move together. They share the same petrochemical feedstock chain. But April 2026 broke that assumption: Brent tumbled from its peak to $90.38 on April 17 before rebounding to $110, while natural rubber climbed 8.9% from 197.80 cents/kg on March 27 to 215.40 cents by month-end.Al Jazeera PHR and DPR — the two largest rubber stocks listed on HoSE — had already warmed to those price gains. The week of May 4 marks the first full market reaction after the April 30 public holiday, and the divergence cannot be ignored.

Why Rubber Broke Away from Oil: A Transmission Chain with One Independent Link

The explanation starts with how synthetic rubber is made. SBR and BR — the two main synthetic alternatives — are produced from butadiene and styrene, both derived from naphtha cracking in oil refineries. When crude oil is expensive, naphtha costs rise, and synthetic rubber becomes pricier. Tire manufacturers shift a portion of their demand toward natural rubber to manage costs. When oil falls, that substitution pressure reverses.

This channel worked exactly as expected in April. Synthetic rubber prices in China dropped 9.9%, from CNY 18,150 per tonne on April 7 to CNY 16,350 per tonne on May 1. Brent's decline was the cause; synthetic rubber followed in lockstep. That part of the mechanism ran to script.

The break happened at the final link. Natural rubber has its own supply dynamics entirely separate from the synthetic side. Southeast Asian rubber plantations have not fully recovered from an extended replanting cycle, and Chinese tire demand has remained robust. The result is a structural supply deficit that kept natural rubber prices firm even as the substitution pressure from cheaper synthetics eased off. For natural rubber, the April environment delivered two simultaneous tailwinds — moderate substitution demand from cost-sensitive tire makers, and an underlying supply constraint that didn't go away. Those forces outweighed the directional pull from cheaper oil.

PHR and DPR: Same Sector, Different Leverage

Both stocks gained ground in April, but at different rates and for structurally different reasons. PHR closed April 29 at VND 61,400 per share, up roughly 8.1% from around VND 56,800 at the end of March. DPR closed at VND 41,200, up 10.2% from VND 37,400 on March 23. DPR was more responsive, and that gap reflects how each company is built.

PHR earns revenue from more than rubber. Its industrial zone operations — anchored by the 786-hectare Thaco Mechanical Industrial Park project — are expected to contribute meaningfully to earnings in 2026 through 2028, generating income streams that are independent of rubber price cycles.Elibook DPR derives almost all of its revenue from natural rubber, making it a direct and high-sensitivity play on commodity prices.

The portfolio implication is straightforward. PHR's industrial zone exposure acts as a buffer: when rubber prices fall, the IZ income limits the downside in earnings and the share price. DPR has more commodity leverage: it performs better than PHR when rubber rises, and it suffers more when rubber corrects. Neither company is structurally superior: they represent different risk-return points on the same sector exposure. Which one fits a portfolio depends on how much rubber price sensitivity an investor is willing to hold.

Three Brent Paths, Three Different Outcomes for Rubber Stocks

Trump's May 1 statement did not close the Iran file. Over the same weekend, the US rejected Tehran's latest peace proposal and Trump said there would be no early end to the conflict.Al Jazeera Brent is holding at $110, not at the $90.38 low it touched on April 17, which suggests the market has not fully priced in a full peace scenario. Three distinct paths lie ahead for this week, each with identifiable triggers.

Peace confirmed — roughly 35% probability at current data — would activate if Iran makes a verifiable, substantive concession or if the US lifts its Hormuz blockade. Brent could slide to the $85–$90 range. Synthetic rubber would continue falling, easing the substitution demand that has partially supported natural rubber prices. Natural rubber might ease from its peak, though the Southeast Asian supply constraint would remain a price floor. DPR would face greater pressure than PHR in this scenario because it has no non-rubber income buffer.

Prolonged stalemate — roughly 45%, the central scenario — plays out if Trump's ceasefire declaration remains a paper statement, negotiations stall, and Iran produces no breakthrough. Brent would hold the $100–$110 range. Synthetic rubber would lose no further ground. Natural rubber would stay near its nine-year high. Both PHR and DPR would continue to benefit through Q2, with DPR retaining more upside sensitivity.

Escalation — roughly 20% — would follow Iranian military action or a Hormuz incident. Brent could push back above $120. The cost differential between synthetic and natural rubber would widen further, providing additional price support for PHR and DPR's output. The counterweight: rising energy costs would compress operating margins for both companies, and at the macro level, imported fuel inflation would add pressure on Vietnam's CPI. That second-order effect is a negative signal for broader market sentiment.

Signals to Watch in the Week Ahead

Three data points will determine which scenario is actually playing out. First, Iran's official response to the Trump statement: a concrete and verifiable concession shifts the peace scenario from speculation to market reality. Second, Brent's closing price in London afternoon sessions: three consecutive closes below $100 signals the peace path is building momentum; a hold above $105 confirms stalemate; a break above $120 accompanied by a specific Hormuz event activates escalation. Third, China's April rubber import data, due for release this week, will confirm or challenge the demand side of the natural rubber bull case.

The current evidence supports the stalemate scenario as the most probable outcome. In that environment, PHR offers lower downside risk than DPR because of its industrial zone income buffer, while DPR retains higher upside sensitivity to rubber prices. The two signals that would force a scenario revision: a substantive Iranian response to Trump's statement, and whether Brent can sustain its current range through the end of the week.