While Vietnam's markets were closed for the national holiday from April 30, three major events unfolded almost simultaneously on the global stage. Brent crude hit an intraday peak of $126/barrel before falling to $110 after President Donald Trump's Iran ceasefire declaration. The S&P 500 closed May 1 at a record 7,230.12, capping a quarter where Big Tech earnings blew past expectations.CNBC And the U.S. core PCE inflation print for March 2026 came in at 3.2% — the highest since November 2023 — cementing the view that the Fed will not cut rates in May.CNBC

The big picture is that these three forces do not add up to a single direction. VN-Index closed the April 29 session at 1,854.10 and reopens Monday morning facing three distinct mechanisms: each with its own transmission channel and its own sectoral implications. Rather than asking "will VN-Index go up or down?" the more useful question is: "which sectors have the wind at their back, and which face headwinds?"

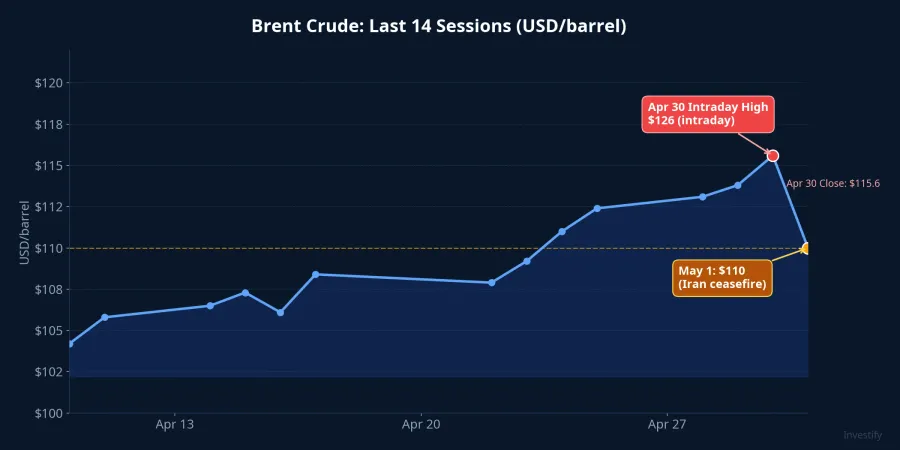

Brent Crude: $126 Intraday, $110 Close

On May 1, President Trump sent a letter to Congress declaring the conflict with Iran "over," stating that a ceasefire had been in effect since April 7 with no further hostilities.CBC This announcement dissolved the war premium that had accumulated throughout April, pushing Brent from roughly $90 at the start of the month up to an intraday spike of $126 on April 30, then back to $110 within hours of the letter's release.

The supply picture, however, is not yet clear. Senator Tim Kaine immediately pushed back: "We are still using the military to blockade all Iranian ports — that is an act of war."CBC Iranian crude has not returned to the market. The $110 level reflects a "ceasefire but blockade intact" equilibrium, not a return to normal. If the naval blockade eases in May, Brent could fall further toward $95-100; if it holds or tightens, the $110 floor could break upward.

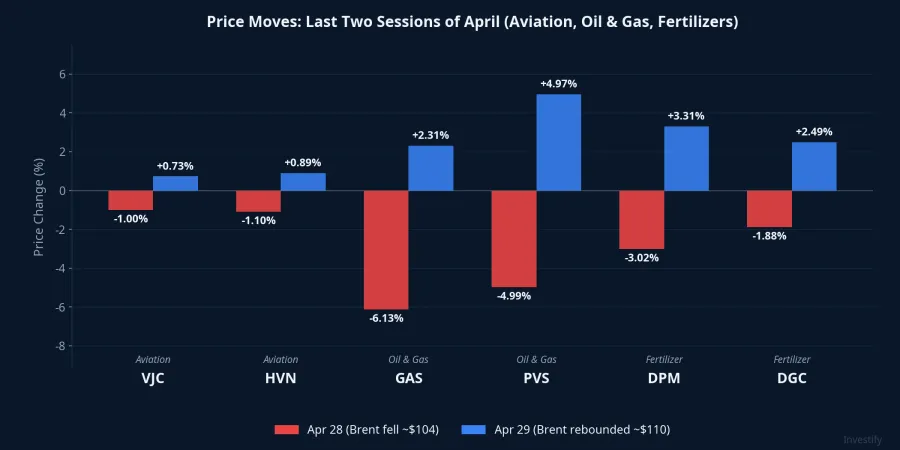

The transmission into Vietnamese equities is highly uneven across sectors.

Aviation is the direct beneficiary. Jet fuel typically accounts for one-third to two-fifths of airline operating costs. A $16/barrel drop from the peak translates to roughly a 13% reduction in fuel costs over the same period. VJC closed April 29 at VND 180,000/share (+0.73%) and HVN at VND 22,600. The margin improvement will flow through to Q2 results gradually. It does not create a one-session gap-up.

Upstream oil and gas faces the opposite. GAS fell 6.13% on April 28 when Brent slid to $104, then recovered 2.31% on April 29 as Brent rebounded to $110. PVS followed closely: -4.99% then +4.97% across those two sessions. Both stocks show tight short-term correlation with spot crude. If Brent stabilizes around $110 through the May 4 week, upstream names will find a new equilibrium below their April peaks; if Brent continues adjusting toward $100, Q2 revenue for GAS and PVS will face meaningful compression.

Fertilizers give a mixed signal. DPM gained 3.31% and DGC gained 2.49% on April 29. Natural gas — the primary feedstock for urea — tends to reprice faster than urea output prices. When Brent retreats from its peak, short-term margins for DPM and DGC improve because input gas costs fall before urea selling prices adjust. Over the medium term, however, the revenue base for both companies will be lower than under a sustained high-oil scenario.

Wall Street Records: Behavioral Tailwind, Not a Capital Channel

The S&P 500 hit a record 7,230.12 and the Nasdaq Composite surged 16.3% in April, driven largely by blowout Q1 results from Big Tech. Apple reported record quarterly revenue of USD 111.2 billion, a clear signal of robust global risk appetite after a strong earnings season.CNBC

The spillover to HOSE, though, is indirect. VN-Index has no large tech components, captures no direct AI-driven capital flows from the U.S., and the day-to-day correlation between the two indexes in recent months has been lower than many retail investors assume. What does cross over is sentiment: when global financial media runs "Wall Street hits a record," local retail investors tend to place larger ATO orders Monday morning. This is a behavioral channel, not a structural capital flow.

For investors watching the 1,877-1,900 resistance band on VN-Index, the distinction matters. Global risk-on sentiment is a supporting condition but not a sufficient catalyst to break through that level. Domestic liquidity would need to climb from roughly VND 22,000 billion per session in April to VND 25,000-28,000 billion before resistance becomes attainable. That is the more important signal to watch over the first three sessions of the week.

PCE 3.2%: Fed on Hold, Foreign Outflows Continue

Core PCE for March 2026 came in at 3.2%, the highest reading since November 2023 and well above the Fed's 2% target.CNBC In the same week Wall Street was celebrating record highs, this data point was the counterweight that markets are currently choosing to look past in the short term. Expectations for the Fed's first 2026 rate cut have continued to drift later, and the May window is essentially closed.

For VN-Index, the consequence sits in foreign flows. In April, foreign investors net-sold VND 13,785 billion on HOSE. The mechanism is straightforward: high U.S. rates create a structural yield advantage for U.S. Treasuries relative to emerging-market equities. With PCE at 3.2% reinforcing the "Fed holds" message, the pressure on emerging-market capital, including Vietnam, extends into May. The exact magnitude of May's net selling is uncertain, but a reversal to net buying would require at least one of two conditions: April PCE falling to 3.0% or below (released late May), or an explicit Fed signal of an earlier-than-expected cut. Neither is on the table for the May 4 week.

One partial offset is worth noting. The DXY index fell 2.1% in April, helping stabilize USD/VND near 26,355. A weaker dollar gives the State Bank of Vietnam room to hold its policy rates without intervening aggressively in the foreign exchange market. This is a constructive signal for domestic VND liquidity, separate from the foreign outflow story driven by U.S. inflation.

Positioning for May 4: Sector Analysis Over Market Direction

The three global shifts that accumulated during Vietnam's holiday break do not resolve into a single market call. Aviation and logistics face a supportive energy backdrop. Upstream oil and gas (GAS, PVS, PVD) face earnings headwinds. Fertilizers receive a mixed signal. Total market liquidity may get a sentiment lift from Wall Street, but foreign capital continues to flow out as long as PCE keeps the Fed sidelined.

The practical framework for May 4 focuses on sectors, not the index.

For positions in aviation or logistics, the supportive factor is in place. VJC and HVN Q2 margins improve if Brent holds at $110 or lower. The key variable to watch is the U.S. naval blockade of Iran, which can reverse quickly.

For heavy positions in upstream oil and gas (GAS, PVD, PVS), Q2 earnings are under pressure if Brent continues correcting from its April peak. A defensive cash allocation of 15-20% is a common portfolio management benchmark when the core sector faces adverse input cost dynamics.

For portfolios positioned at the 1,877-1,900 VN-Index resistance zone, the decisive indicator over the first three sessions is daily turnover. If liquidity does not exceed VND 25,000 billion per session, the higher-probability scenario is continued consolidation in the 1,840-1,880 range rather than a breakout.

Data to track over the next two weeks: Q1 earnings from listed companies (confirming or denying the sector margin story), developments in the Iran naval blockade (determining whether Brent drifts to $95-100 or rebounds), and the April PCE print at the end of May (the signal for the Fed's June decision).