Vietnam's real estate sector Q1/2026 earnings reports do not paint a picture of uniform recovery. In the same quarter, Dat Xanh Group's (DXG) brokerage segment more than tripled year-on-year, putting the company at 80% of its full-year profit target after just three months. Meanwhile, DIC Corp (DIG) posted another net loss, and DRH Holdings received a formal warning from HOSE for late financial filing. Same market, same quarter — two business models operating on completely different timelines.

DXG: Brokerage Triples, 80% of Annual Profit Target Cleared in Q1

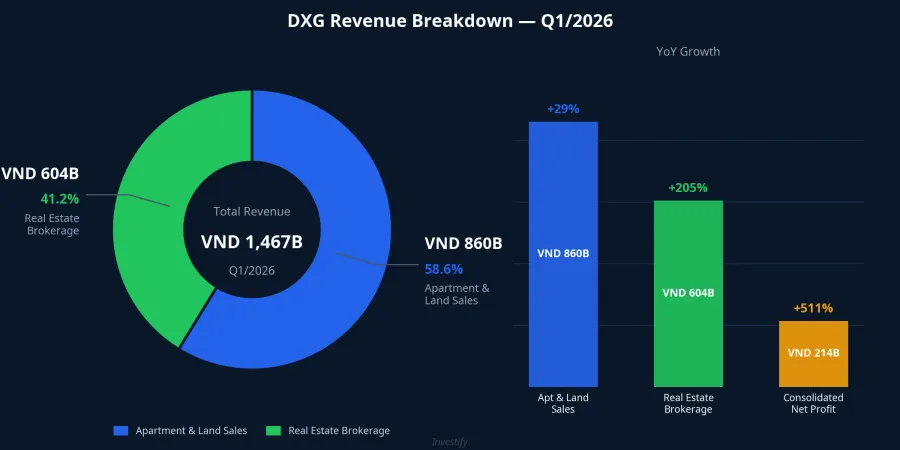

The headline numbers for DXG in Q1/2026 are strong, but the revenue breakdown is where the real story sits. Consolidated revenue reached over VND 1,467 billion, up 59% year-on-year. Net profit after tax came in at over VND 214 billion, equivalent to 80% of the company's full-year profit target — achieved in a single quarter.VietStock

The growth gap between the two main revenue streams is striking. The real estate brokerage segment contributed nearly VND 604 billion, more than three times the year-ago figure. The apartment and land sales segment brought in over VND 860 billion, up approximately 29%. That is a solid result, but roughly one-third the growth rate of brokerage.VietStock Two revenue lines in the same report, reflecting two different realities in the underlying market.

One balance sheet item warrants a separate read-through. Loans to other parties ballooned to over VND 3,300 billion — approximately 2.9 times the balance at the start of the year.VietStock This line item does not undermine the brokerage recovery narrative, but it does raise questions about asset quality and how the company is deploying its cash. Investors following DXG should keep this on their monitoring list through coming quarters.

DIG and DRH: Developers Facing an Unfinished Pipeline Problem

DIC Corp's Q1/2026 numbers tell a different story. Net revenue came in at VND 144.55 billion, down 5.4% year-on-year, with a net loss of over VND 9.9 billion.Tin Nhanh CK The loss did improve significantly versus the VND 45.4 billion loss in Q1/2025, but it still reflects a core business where revenue is not yet sufficient to cover finance, selling, and administrative costs.

The issue with DIG is not weak sales capability — it is that the company's flagship projects have not yet reached the revenue recognition threshold. The Bac Vung Tau project is expected to break ground in Q3/2026 and Long Tan in Q4/2026, after years of regulatory approvals.VietTimes Full-year 2026 targets stand at VND 3,000 billion in revenue and VND 600 billion in pre-tax profit. With Q1 results as a baseline, DIG has a very long road ahead.

DRH Holdings is in a more difficult position. The DRH stock was placed under a formal warning by HOSE effective April 24, 2026, following submission of its 2025 audited financial statements more than 15 days past the deadline.CafeLand Prior to this, DRH had reported losses for 10 consecutive quarters before recording a VND 93 billion profit in Q4/2025, narrowly avoiding three years of back-to-back losses that would have triggered a mandatory delisting.VnBusiness The late filing is a disclosure red flag. For retail investors, it is a material risk factor to price in before approaching this stock.

Why the Two Groups Diverge: Revenue Recognition Mechanics

The split between brokers and developers is not a story of one outperforming the other in business execution. It is a story of how each business model is required to record revenue.

Brokerage commissions are recognized as soon as the service is delivered: the moment a transaction closes and the deal is confirmed. Every contract signed flows directly into that quarter's revenue line. When transaction volumes pick up, brokerage revenue responds immediately, in the same reporting period.

Developers operate under a different set of rules. Under applicable accounting standards, revenue from real estate sales may only be recognized when control of the asset transfers to the buyer. In practice, this is typically tied to physical delivery of the unit, completion of infrastructure, or specific contractual milestones. A signed purchase agreement does not equal recognized revenue. When legal approvals are delayed or construction timelines extend, revenue recognition is deferred even if sales have already occurred on the ground.

The practical result: in the same market recovery wave, the two types of business respond on different clocks. Brokers benefit in the first quarter; developers have to wait until projects cross the finish line.

Primary Market Recovery: Transaction Volume Leads, Pricing Follows

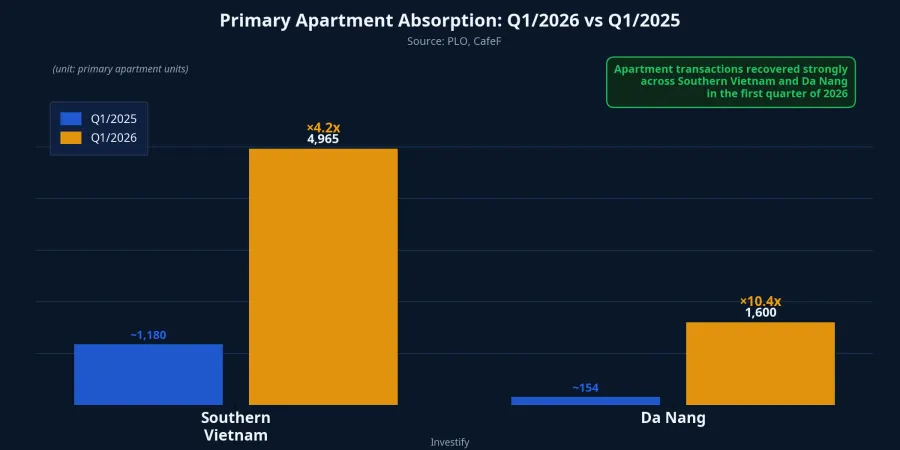

The Q1/2026 transaction data confirms that real demand has returned. Southern Vietnam recorded absorption of approximately 4,965 primary apartment units, up roughly 4.2 times year-on-year.PLO Da Nang absorbed over 1,600 apartment units, up more than 10 times, with the majority coming from newly launched projects during the quarter.CafeF This transaction recovery is precisely what explains the strong brokerage performance at service firms like DXG.

But transaction recovery is not the same as margin recovery. Primary prices rose only modestly — around 1–3% — and the secondary market remains sluggish as home loan rates sit higher than in the 2021 cycle. Transactions came back first; developer margins have not followed yet. This is a recognizable feature of the early stage of a real estate recovery cycle.

Reading Property Stocks During a Divergence Cycle

The most important takeaway from Q1/2026 data is that the Vietnamese property sector does not behave as a monolithic group. Differences in business model are now producing materially different outcomes on financial statements within the same quarter.

First, do not read "real estate recovery" as a uniform sector condition. In the same quarter, a brokerage-driven company can clear 80% of its annual profit target while a developer posts a loss. Both outcomes are accurate at the same time. Segment by business model first, then read the sector narrative.

Second, for developers, the meaningful signal to watch is not quarterly revenue but the legal and construction timeline of key projects. For DIG, the milestones that matter are Bac Vung Tau (Q3 groundbreaking) and Long Tan (Q4). Until those milestones are confirmed — and projects enter the phase where revenue can actually be recognized — quarterly earnings will continue to reflect costs rather than commercial progress.

Third, a liquidity recovery at one end of the value chain does not guarantee the same recovery at the other end. If home loan rates remain elevated and the secondary market stays slow, brokerage firms may maintain their momentum for several more quarters while developers continue to wait. These two threads deserve separate tracking, not a single sector headline.

Signals worth monitoring in coming quarters: Q2 pre-sales results at developers with projects approaching completion; legal progress updates on Bac Vung Tau and Long Tan; and any movement in home loan rates as monetary policy evolves.