VN-Index ended April at 1,854.10 points, up 10.7% from the end of March. On the ticker board, the picture looks good. But three internal indicators tell a different story: liquidity fell 25%, market breadth narrowed, and foreign investors sold consistently throughout the month. The index may test the 1,877–1,900 resistance zone in May, but the actual direction depends on two unanswered variables: how long the Strait of Hormuz stays blocked, and where April's CPI lands.

The next trading session opens on Monday, May 4 after a four-day holiday. The gap from the current closing level to the 1,877–1,900 resistance zone is under 3%. Technically, a strong session could touch it. But the index alone does not write May's story.

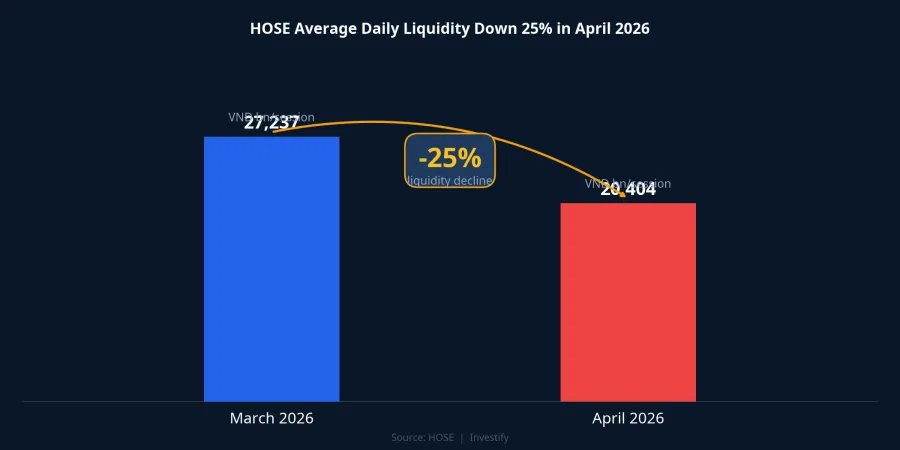

Price Up, But Money Flow Heading Down

Looking at the broader picture, three internal data points are diverging sharply from the headline index level.

Average daily liquidity on HOSE in April came in at approximately VND 20,404 billion per session, down 25% from VND 27,237 billion in March. The index climbed nearly 11%, but trading value fell by a quarter. This is an unusual combination: normally, a strong market rally is accompanied by expanding liquidity. When the index rises while trading volume contracts, the market is climbing on an increasingly thin foundation.

Market breadth in the final three sessions of April was weak. The session on April 24 recorded 130 gainers versus 187 decliners; April 28 was worse, with only 98 gainers facing 203 decliners; the final session on April 29 improved to 155 up and 136 down. For the final week of April as a whole: 383 advancers against 526 decliners. The index was carried by large-cap stocks while most of the market moved in the opposite direction.

Foreign investors continued to sell. Net foreign selling on HOSE in April totalled approximately VND 15,606 billion, roughly matching March's pace. The hardest-hit names were the usual blue-chip leaders: VHM, FPT, VIC, VCB, BID, HDB, VPB, ACB, and MBB. Foreign net buying was concentrated in steel, consumer, retail, and industrial property names: HPG, MSN, VPL, SSI, VRE, MWG, LPB, TCH, and DXG.

Taken together, these three data points suggest April's rally was not driven by fresh money entering the market. It has the characteristics of a large-cap-led recovery while the broader market remains hesitant. The index may post short-term highs, but the foundation for holding them is thin.

Hormuz: The Central Variable for May

Since mid-April, the US has maintained a naval blockade of Iranian ports and the Strait of Hormuz. Vessel traffic through Hormuz fell to very low levels; at certain points Iran further restricted ship movements. Brent crude futures spiked to around $126 per barrel during the April 30 session before pulling back to $110.40 at close, then returning to $111.88 in the May 1 session. A nearly 14% intraday swing is typical of a market waiting on a political decision.

Hormuz is not just an oil story. When crude prices stay elevated, fuel costs rise, CPI comes under pressure, and the State Bank of Vietnam's monetary policy room narrows. Foreign capital flows into emerging markets are also more sensitive to the global interest rate environment. March's CPI at 4.65% was already close to the level many analysts watch closely. April's CPI may come in higher given the significant rise in fuel prices during the month. This is the direct link between Hormuz and domestic capital flows in May.

Three VN-Index Scenarios for May

Bullish scenario: US lifts blockade, Hormuz reopens

The trigger is a US announcement ending the blockade and Hormuz reopening within the first one to two weeks of May. Brent has room to fall back below $100, near the price level on April 21 before the geopolitical spike. Fuel cost pressure eases quickly; if April's CPI comes in at the low end of expectations, the window for keeping policy rates unchanged widens. Capital flows into emerging Asian markets typically recover quickly once geopolitical risk subsides. VN-Index could break through the 1,877–1,900 zone in the second half of May, but only if liquidity rebounds above VND 25,000 billion per session in the first three sessions after the holiday.

Neutral scenario: Hormuz stays partially closed

This is the actual state of affairs as of the end of April. The US holds the blockade, Iran keeps Hormuz constrained, and no new military events occur. Brent oscillates in the $105–120 range with a wide swing but no clear directional bias. April's CPI will likely come in higher than March's 4.65%, given the sharp rise in fuel prices. The market moves into a phase of digesting Q1 earnings results, trading in the 1,820–1,877 range. Sector rotation becomes more pronounced: steel, consumer retail, and exporters benefit from the current exchange rate environment; banks and real estate face pressure from tighter liquidity and continued foreign selling. This is the highest-probability scenario based on conditions through the end of April.

Cautious scenario: escalation or a hawkish Fed

Two types of events could trigger this scenario, independently of each other. First, a new US-Iran military confrontation pushes Brent above $130. Second, the Fed signals a more hawkish stance after Q1 core PCE at 3.2% is referenced in May communications. The consequences: a stronger US dollar, increased pressure for capital outflows from emerging markets. Foreign investors already sold a net VND 15,606 billion in April. If this scenario materialises, a similar pace of selling could continue in May. VN-Index may pull back to the 1,750–1,820 zone, roughly where the index stood at the start of April before the rally began.

Three Signals to Watch in the First Week of May

There is no need to guess which scenario plays out before the market tells us. Three signals will resolve the picture during the week of May 4–9:

First, an official statement from the US or Iran on Hormuz. A blockade-ending announcement or ceasefire carries more weight than any interim update.

Second, Brent crude's opening price on international markets at the start of the week. Below $105 leans toward the bullish scenario; above $120 leans toward the cautious scenario; in between, the neutral scenario holds.

Third, the General Statistics Office's April CPI reading. If CPI exceeds 4.8%, monetary policy room narrows significantly and the probability weight on the bullish scenario falls.

Assessment

The big picture for May is a genuine crossroads, not a predetermined trend. The neutral scenario carries the highest probability based on current conditions at Hormuz. The bullish scenario can materialise quickly if a political decision arrives. The cautious scenario is a tail risk to hedge against, not a central forecast.

With liquidity and market breadth both contracting, a portfolio approaching resistance after a strong run should maintain a reasonable defensive cash allocation. The appropriate level depends on each investor's leverage and holding horizon. What matters most is having a pre-planned response for all three paths rather than betting on one outcome while Hormuz remains unresolved.

The most important signals to watch in the first week of May: Brent's opening price on Monday, May 4, and any official statements from Washington or Tehran on the status of the Strait of Hormuz.