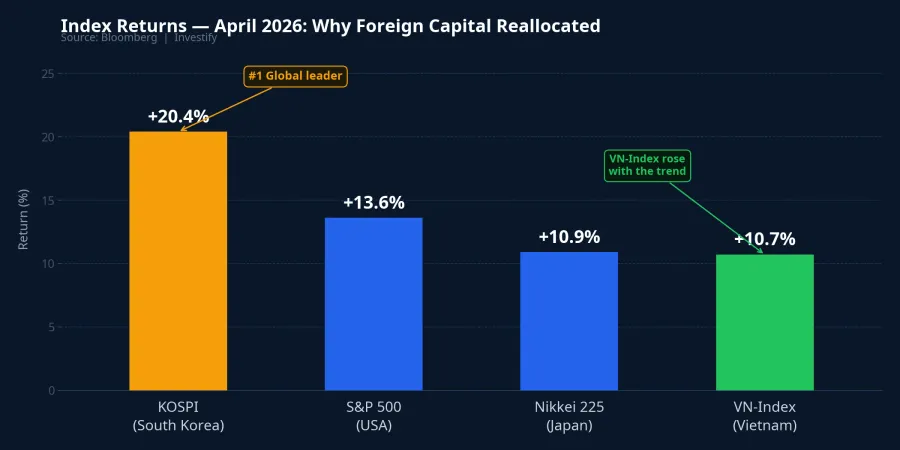

VN-Index closed April 2026 at 1,854.10 points, adding nearly 180 points from the end of March, a 10.7% gain for the month.NguoiQuanSat Over the same period, foreign investors net sold VND 13,785.5 billion on HOSE.TinNhanhChungKhoan Reading those two numbers together, it's tempting to frame them as a paradox: foreigners exit heavily while the index rallies strongly. The real question is more pointed than that. Who bought the other side of those VND 13,785 billion in sales, where did the capital come from, and what risks does a market driven entirely by domestic money carry going forward?

Why Foreign Investors Sold

April's net selling was not a flight from Vietnam. Global context explains most of it: KOSPI gained 20.4%, its best month in 28 years; S&P 500 added 13.6%; Nikkei rose 10.9%.TinNhanhChungKhoan When major markets accelerate simultaneously with superior returns, regional capital flows naturally shift toward deeper liquidity and wider upside. VN-Index at +10.7% is a solid number by domestic standards, but measured against KOSPI at +20.4% within the same month, the competitive pull had clearly reversed direction.

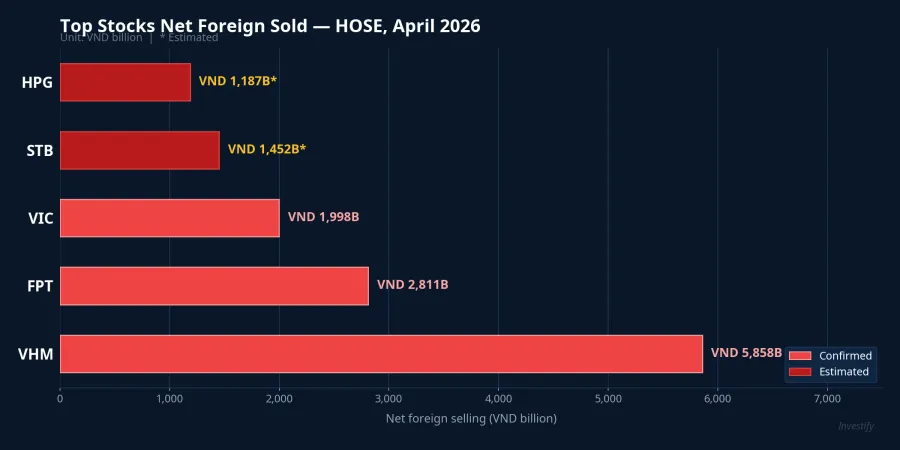

The composition of the selling confirms this was portfolio reallocation, not a panic exit. VHM was net sold for VND 5,858.5 billion; FPT for nearly VND 2,811 billion; VIC for approximately VND 1,998 billion. These three large-cap names accounted for roughly 76% of total foreign net selling for the month.TinNhanhChungKhoan They are the most liquid positions in the Vietnam portion of regional portfolios, the natural first choice when reducing emerging market exposure to fund a KOSPI position.

One observation stands out: VHM, VIC, and NVL were precisely the stocks leading VN-Index's 180-point gain.NguoiQuanSat Foreign investors were selling hardest into the very stocks rising the fastest. Domestic buyers were not merely providing liquidity. They were paying higher prices to take on the exact positions that global professionals were trimming.

Who Absorbed VND 13,785 Billion

Trading data compiled by Vietstock and VnEconomy shows domestic institutions maintained strong net buying throughout the month, with some sessions exceeding VND 4,000 billion in matched orders alone.VietstockVnEconomy Retail investors entered more slowly but steadily. Securities firms' proprietary trading flipped in and out by session, not a primary driver. Cumulatively across the month, the VND 13,785 billion gap left by foreign sellers was filled almost entirely by domestic institutions, with retail investors covering the remainder.

These institutions include open-end funds, insurers, investment companies, and some corporate treasury flows. Their rationale was coherent: VN-Index valuation at end-March sat in an attractive range relative to the region, FTSE has confirmed an upgrade for September 2026, and some upgrade-premium was being priced in early. But institutional flows have finite scale. Retail investors carried the balance. And the mechanism behind their buying is where the risk picture sharpens.

Record Margin Debt: Where the Real Risk Lives

At the end of Q1/2026, total securities industry lending reached approximately VND 415,000 billion, with margin lending alone accounting for roughly VND 405,000 billion, a record high for the market.ThoibaotaichinhVN Margin debt grew by approximately VND 13,000 billion in Q1 alone compared with end-2025. Fifteen securities firms now carry outstanding lending above VND 10,000 billion; five have surpassed the USD 1 billion mark: TCBS, SSI, VPBankS, VPS, and HSC. TCBS leads with nearly VND 45,000 billion.TinNhanhChungKhoan

The VND 415,000 billion figure does not directly represent capital deployed in April, since most of the outstanding balance predates the month. But the record level confirms one thing clearly: the buying pressure that absorbed the blue-chip shares foreigners were unloading was not primarily funded by cash equity. It was levered capital, borrowed from securities firms and sitting just above margin call thresholds. When VHM, FPT, and VIC were rising while foreign investors sold, the buyers on the other side were mostly retail investors using borrowed money.

The mechanism is straightforward. At a 1:1 margin ratio, every VND 100 of retail equity becomes VND 200 of buying power on the exchange. Margin interest rates at several securities firms currently sit at 13 to 14% annually.ThoibaotaichinhVN This leverage amplification is what physically enabled domestic capital to fill the entire VND 13,785 billion foreign gap while the index still climbed 10.7%. It is also the exact feature that makes the structure fragile in the other direction.

Looking Back at 2021, Looking Ahead to 2026

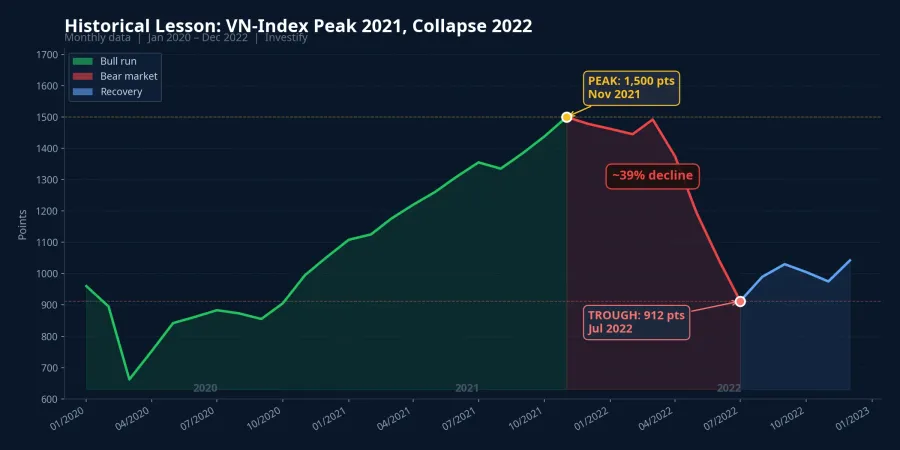

The last time foreign investors sold at a comparable pace, the full-year 2021 total reached approximately VND 58,000 billion.VnEconomy April 2026 alone produced VND 13,785 billion, nearly a quarter of that annual figure compressed into four weeks. The pace of foreign outflows is running at historically elevated levels.

2021 was also the year VN-Index reached its peak riding exclusively on domestic flows and leverage. Margin debt set consecutive records throughout that period. In 2022, when market sentiment reversed alongside the shock from the Tan Hoang Minh and Van Thinh Phat bond scandals, VN-Index shed more than 30% and forced liquidations cascaded through the market.

The lesson is not that high margin guarantees an imminent crash — history does not replay that mechanically. The real lesson is: when a market rises entirely on domestic capital and leverage at peak levels, its sensitivity to a small shift in retail sentiment becomes disproportionately large. A systemic shock is not required. It only takes one of the three supporting pillars to retreat for selling pressure to amplify across the others.

Two Signals to Watch in May

April's market rested on three pillars: domestic institutions buying on valuation and the FTSE upgrade thesis; retail investors buying into price momentum; and securities firm leverage multiplying the retail buying power. Foreign investors are no longer a buffer. They are the sellers. This structure is strong when all three pillars push up together, but when any one pulls back, the remaining two must absorb the full load.

Two specific signals are worth tracking in May. First: does margin debt continue climbing above VND 420,000 billion, approaching the 200% equity capital ceiling at leading securities firms? Second: do retail investors shift from net buying to net selling as VN-Index approaches the resistance zone between 1,877 and 1,900 points? Either signal appearing alongside continued foreign net selling would remove the final cushion supporting the index.

The central question is not whether VN-Index will continue higher or reverse. The central question is what kind of structure is doing the work. The three pillars currently holding this market — domestic institutions, leveraged retail, and record margin debt — differ meaningfully from a market with foreign capital as a stabilizing counterweight. When all three legs are domestic, the margin of safety in each individual portfolio matters more than any index forecast.

April's question has been answered: who bought when foreigners sold, and with what capital. May will answer the follow-up: whether that structure holds when the pressure builds.