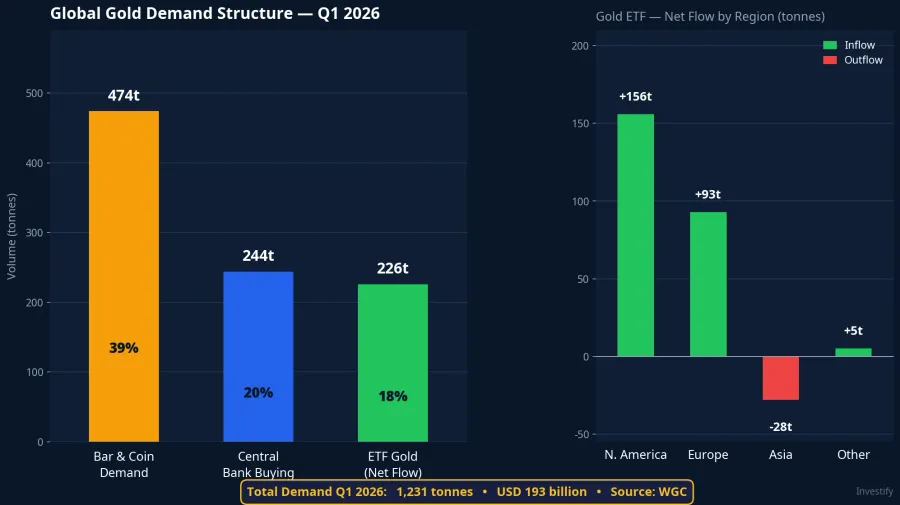

On April 29, the World Gold Council (WGC) published its quarterly report: global gold demand in Q1 2026 reached USD 193 billion in value, up 74% year-on-year and an all-time record by dollar terms.WGC Yet physical volume rose just 2%, to 1,231 tonnes. That figure remains far from any volumetric record.VnExpress The bulk of the "record" traces back to a single variable: the average gold price in Q1 2026 rose 81% compared to the same period a year earlier.WGC

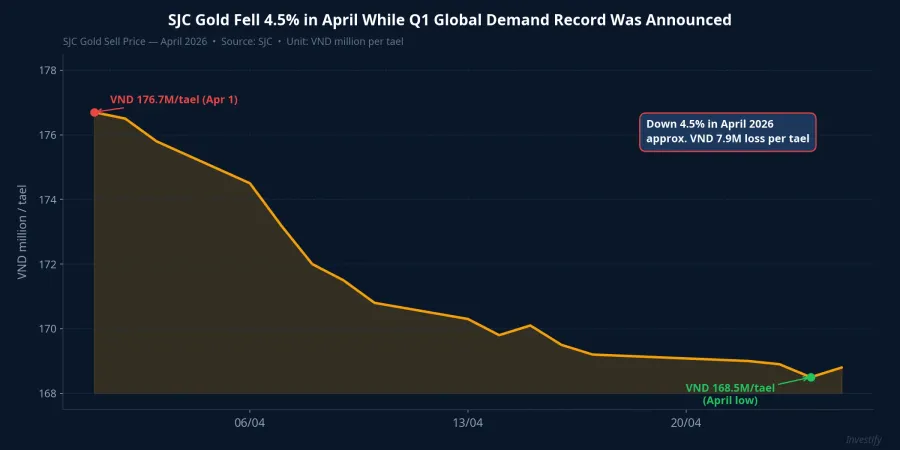

That distinction matters. When the headline says "record," the bigger picture is this: the price ran first and pulled total dollar value up, while physical demand grew only modestly. Set against that a separate fact: buyers who purchased SJC gold bars in early April are sitting on a loss of roughly VND 7.9 million per tael in less than four weeks. These two pictures are not in conflict: they complement each other, and reading both together is the only way to properly interpret the USD 193 billion record.

Group 1: Central Banks and the Long-Term Price Floor

Central banks worldwide purchased 244 tonnes net in Q1 2026, up 3% year-on-year and above the 5-year average. This extends a consecutive streak of net buying quarters that began when the wave of reserve diversification away from USD-denominated assets accelerated after 2022.WGC

The specifics: Poland accumulated approximately 31 tonnes during the quarter, Uzbekistan added around 25 tonnes, and China reported reserve increases in all three months of the quarter. On the other side, Turkey sold over 118 tonnes to support the lira, and Russia sold gold to meet budget pressure. Net out everything, and aggregate net buying remains dominant.

The defining characteristic of this group is price insensitivity on any short-term horizon. The objective is strategic reserves measured in decades, not quarterly returns. It is precisely this steady demand that kept gold around USD 4,500–4,700 per ounce throughout April, even on days when ETF outflows were substantial.

Group 2: Physical Gold in Asia, the Quarter's Real Surge

Global bar and coin demand reached 474 tonnes in Q1 2026, up 42% year-on-year.WGC This is the genuine volume driver of the quarter, and the surge was heavily concentrated in Asia.

China alone contributed 207 tonnes of bar and coin demand, up 67% year-on-year, the highest single-quarter figure WGC has ever recorded for any country.WGC India maintained steady jewellery and small-format investment demand. Thailand, Indonesia, and other markets with strong gold-hoarding traditions also contributed meaningfully.

A critical distinction: the dominant motivation for this group is long-term wealth preservation, not short-term price speculation. When prices rise, these buyers increase allocations precisely because their conviction in gold as a store of value is reinforced. That logic is entirely different from ETF flows.

On the ETF side, capital flows diverged sharply by region. North America and Europe saw meaningful net inflows, but SPDR Gold Shares — the world's largest physically backed gold ETF — sold over 20 tonnes across multiple consecutive sessions in March before buying back 3.43 tonnes in early April. ETFs carry fast money that reverses quickly with Fed rate expectations. That is volatility, not structural support.

Vietnam: Moving Against the Regional Trend Due to Supply Constraints

This is where Vietnam's picture diverges sharply. Jewellery demand reached USD 472 million in Q1 2026, a new record and up 28% quarter-on-quarter.VnExpress But WGC noted that consumers shifted toward lower-purity jewellery as 24-karat gold became unaffordable at prevailing prices. The record in dollar terms mainly reflects price inflation, not volume growth.

More significantly, the bar and coin segment — the primary savings vehicle for Vietnamese retail investors — declined 24% to just 9 tonnes, the steepest drop in Southeast Asia.VietnamNet In the same quarter that China set a physical gold record and Thailand led the region, Vietnam moved in the opposite direction.

The explanation almost certainly isn't that Vietnamese investors suddenly lost their appetite for gold. It is a supply problem. The SJC bar monopoly lasted until Decree 232/2025 partially liberalized it in October 2025, but the mechanism for importing raw gold material still rests with the State Bank of Vietnam's discretionary permit system. Licensed producers must apply for import quotas on a case-by-case basis. The result: genuine demand is suppressed. Buyers who want gold cannot find enough supply, and those who already hold SJC bars face a domestic price that diverges widely from the world price.

The consequence of that divergence shows up directly in April's price series: SJC's sell price on April 1 was VND 176.7 million per tael; by April 25 it had fallen to VND 168.8 million, a decline of approximately 4.5% in the month. Over the same period, the world gold price fell roughly 2.4% in the last week of April. SJC fell more steeply because the domestic premium compressed as market sentiment eased, not because underlying Vietnamese demand suddenly weakened.

Reading the USD 193 Billion Record Correctly

Three buyer groups produce three distinct conclusions from the same headline.

First, gold's long-term price floor remains solid. Central bank buying and Asian physical demand are not dependent on Fed rate policy or short-term risk sentiment. As long as both groups continue purchasing systematically, gold faces a structural buffer against deep declines in the medium and long term.

Second, short-term price swings are driven primarily by ETF flows. ETFs reverse quickly with rate expectations, and SPDR demonstrated this in March. Holders who monitor gold prices through the ETF lens will experience significant volatility in both directions.

Third, Vietnamese SJC holders carry an extra risk layer that no other market faces: the domestic premium relative to the world price can compress at any time as the import licensing mechanism under Decree 232/2025 is broadened. This is domestic policy risk, entirely separate from gold-as-asset risk.

The big picture is one of a three-tier structure: central banks provide the price floor, Asian physical demand creates medium-term support, and ETFs generate short-term volatility. Understanding which layer is operating at any given moment is the minimum prerequisite before sizing a gold allocation.

Within a standard asset allocation framework, gold remains a legitimate component at roughly 5–10% for long-term hedging against systemic risk and currency erosion. Two caveats apply at the current entry point: world gold prices have already risen 81% year-on-year, meaning entering at elevated levels without a long time horizon (5–10 years or more) leaves a portfolio highly exposed to an ETF-driven pullback; and SJC gold in Vietnam carries an additional premium-compression risk that is distinct from the underlying gold price.

Signals to watch in May. The pace of import license issuance under Decree 232/2025 is the most direct indicator for Vietnamese holders: more licences means the SJC premium narrows toward the world price. Whether SPDR's modest 3.43-tonne repurchase in early April develops into a sustained inflow will indicate fast-money sentiment. And the monthly net buying figures from central banks, especially China, remain the key measure of long-term structural support.