Strong Numbers, But Structure Tells a Different Story

Total corporate bond issuance in Q1/2026 came in at 2.1 times the same period in 2025.Tin nhanh CK Interest rates on offer run 4 to 5 percentage points above Big4 savings rates. Retail investors are being courted more aggressively than at any point since 2022. On those metrics alone, "recovery" seems like a reasonable label.

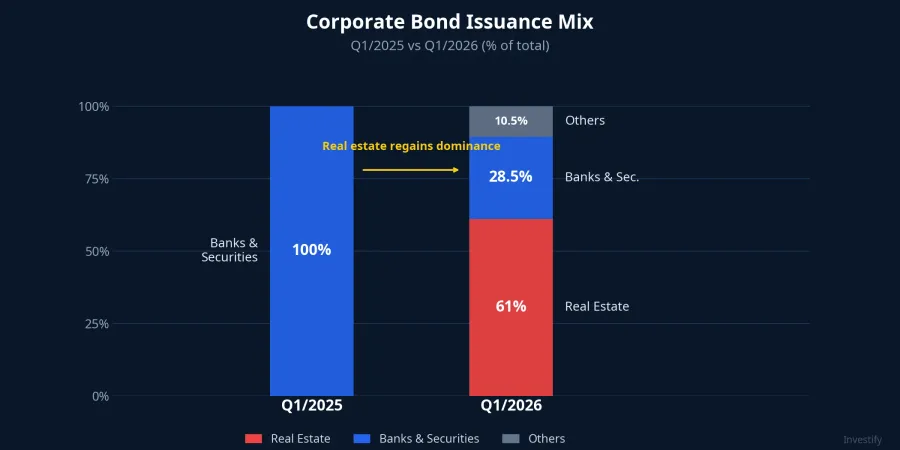

But open the sector breakdown and the story changes. Real estate accounted for 61% of all corporate bond issuance in Q1/2026, with banks and securities firms at just 28.5%.Phụ nữ VN That structure is nearly identical to Q1/2022, the quarter immediately before Tan Hoang Minh had nine bond tranches cancelled and An Dong pulled the whole market into a crisis of confidence. By contrast, Q1/2025 ran in the opposite direction: 100% of issuance came from banks and securities firms. The shift reversed in a single quarter, not gradually.

This does not mean another crisis is certain. It does raise a specific question: what has genuinely changed since 2022, and what has not?

What Has Actually Changed: Barriers Around Investors

Decree 65/2022 and its subsequent amendments through 2025 focused squarely on the buyer, not the seller. Individual investors seeking to purchase privately placed bonds must maintain a listed securities portfolio of at least VND 2 billion continuously for 180 days. Professional investor status expires every three months. Distributing securities firms must independently verify eligibility. The workarounds via investment cooperation contracts and entrustment agreements have been closed off.

These are real barriers. They have meaningfully narrowed the pool of eligible participants.

The regulation screens buyers, not product quality. Decree 65 does not require independent credit ratings for all privately placed tranches, does not mandate substantive collateral, and does not prohibit issuances with no land title backing. An investor who meets the VND 2 billion threshold can still purchase a bond secured only by rights arising from a business cooperation agreement. The improvement is genuine. It covers part of the road, not all of it.

What the Headlines Leave Out

Real estate still dominates issuance. At 61% of Q1/2026 issuance, the share is actually higher than the roughly 50% seen in Q1/2022. As bank lending into real estate has been tightened via credit room controls, bonds have again become the funding alternative of choice. The same macro driver that produced the 2021 issuance surge is running again.

Billions in a single day, secured only by contract rights. On 31 March 2026, Thoi Dai Moi T&T issued VND 8,000 billion in bonds (ticker NTJ12601), 48-month tenor, 10.5% annual coupon.CafeF The collateral: rights arising from a business cooperation agreement with Capitaland Tower and rights related to a transfer contract for the Can Gio project. Not a completed land title. The stated use of proceeds was capital contribution and payment of transfer value for a project that has not yet cleared all legal hurdles.

One week later, on 23 April, Bat dong san Minh An closed two tranches totalling VND 7,500 billion in a single day: MAD32601 for VND 1,300 billion at 10% per year with a 12-month tenor, and MAD12602 for VND 6,200 billion at 10.5% per year, also 12 months. Both tranches carried no collateral at all, both distributed through TCBS.Tin nhanh CK Unsecured issuance from low-disclosure real estate developers was a hallmark of the market that collapsed in 2022.

Secondary market liquidity remains thin. The HNX-Bond platform for privately placed corporate bonds is still a market with few buyers and few sellers. An investor who wants to exit early must negotiate directly with the issuer or sell bilaterally through the distributing firm at a price that is difficult to predict.

The 2022-2023 debt backlog is not resolved. Real estate companies still face approximately VND 141 trillion in bond maturities during 2026, and a significant portion consists of tranches that were extended from 2022-2023.CafeF A portion of Q1/2026's "recovery" issuance is therefore rolling into the same maturity window as deferred obligations from three years ago. That is not the same as stable, on-time repayment from operating cash flows.

Three Minimum Checks Before Buying

The 4 to 5 percentage point spread over Big4 savings rates (currently around 5.9% per year for 12-month deposits)Tin nhanh CK is not a free lunch. It is the market's price for real estate credit risk and 48-month liquidity risk. These three checks are the minimum defence for a retail investor before signing:

Layer 1: What exactly is the collateral, not just whether there is any. "Rights arising from a business cooperation agreement" and "rights under a transfer contract" have very different recovery value from a completed land title. Read the original disclosure document rather than the underwriter's summary, find the exact collateral description, and ask: if the issuer cannot pay, who enforces those rights, and how long does it take?

Layer 2: What cash flow does the stated use of proceeds actually generate. Capital deployed into a project that has not cleared its legal approvals can only service interest if the project sells on schedule. That is not current operating cash flow from the issuer; it is a bet on future project cash flows. A 48-month bond whose proceeds go into an unlicensed-development project carries the same structural risk profile as the tranches that defaulted in 2022-2023.

Layer 3: Secondary liquidity before committing to a long tenor. Search the bond's ticker on the HNX platform and check whether there have been any trades in the past 30 days, and at what price relative to par. A bond with near-zero secondary activity means 48 months with no exit other than direct negotiation.

Real Recovery, Real Risk

Q1/2026 is not a carbon copy of Q1/2022. The professional investor threshold is a genuine improvement. The legal framework for tenor extensions and asset swaps reduces the binary collapse dynamic that played out in 2022. These changes matter.

But for an investor looking at a 10.5% per year, 48-month real estate bond with no completed land title as collateral, the three checks above are the actual distance between "healthy recovery" and "same structural risk, different packaging." The 4 to 5 percentage point yield premium is a risk price, not a discount.

Signals worth monitoring over the coming months: the on-time repayment rate among the VND 141 trillion of real estate bonds maturing in 2026, and whether HNX-Bond starts recording meaningful secondary volume in the private bond segment.