The June Brent crude contract closed April 30 at 126.10 USD per barrel, the highest level since early 2022, after a single-session gain of 6.84%.CNBC Vietnam's stock market is closed for the holiday and won't reopen until Monday, May 5. This is not a moment to overlook.

The central question this piece addresses: along the transmission chain from Brent through retail fuel prices through CPI to the State Bank of Vietnam's policy space, where exactly does Vietnam stand right now? And how much of that transmission is still ahead?

Brent at 126 USD: The Big Picture

The Strait of Hormuz normally carries approximately 20 million barrels of crude and petroleum products per day, roughly one-fifth of global oil supply, according to VietnamPlus.VietnamPlus Tehran has refused to reopen the strait unless Washington lifts its naval blockade; Washington won't lift the blockade without a new nuclear agreement. Four weeks of talks have failed to break this deadlock.

The April 30 spike came after the U.S. Central Command (CENTCOM) prepared a short but high-intensity strike option targeting Iranian infrastructure for President Donald Trump to review. The narrative shifted from "diplomatic tension" to "potential military intervention" and markets responded immediately.

Placing 126 USD alongside historical oil shocks puts the pace of this rally in context. In 1990, Brent surged from roughly 17 USD to over 35 USD within weeks after Iraq invaded Kuwait. In the current episode, Brent has climbed from the 95-100 USD range in late March to 126 USD by April 30. The critical difference is that this is not an outright war between two nations but rather a stalemate combined with a gradual escalation. The CENTCOM option on Trump's desk elevates the situation to a new threshold.

Vietnam's Position in the Transmission Chain

At the April 29 adjustment, the ministries of Industry and Trade and Finance raised E5 RON92 retail prices to VND 22,620 per liter and diesel to VND 29,430 per liter, brought forward from the regular schedule because it fell during the holiday period.VOV Measured across the full month of April, E5 RON92 has increased 24.1% and diesel 66.6%. Industrial mazut added another 40.6% over the same window.

Two details matter more than those headline numbers. First, the April 29 adjustment was based on Brent trading in the 110-115 USD range in the days prior; the 126.10 USD reading on April 30 has not yet fed into the price base for the next cycle, expected on May 9 after the holidays. In other words, the transmission from Brent at 120-130 USD into retail fuel prices is not yet complete.

Second, the petroleum price stabilization fund is nearly exhausted, leaving little buffer to absorb the next round of price passthrough.VietnamNet The low-cost inventory accumulated in earlier periods has been drawn down across three previous adjustment cycles. This means the May 9 adjustment will need to reflect most of the gap between the old price base and actual Brent levels.

March CPI and the SBV's Policy Room

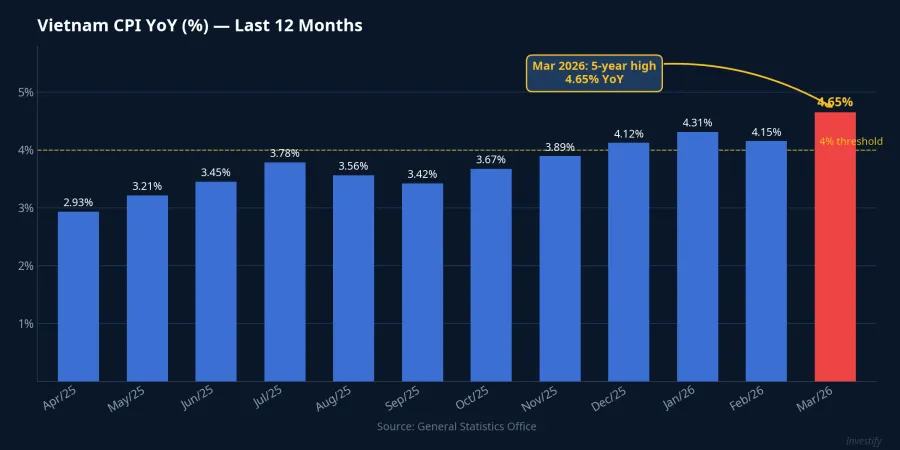

Vietnam's March 2026 CPI rose 4.65% year-on-year, the highest in five years.CafeF Transportation alone contributed 1.28 percentage points to that total, meaning nearly one-third of the monthly CPI increase came from mobility costs.

One important detail: March CPI reflects fuel prices from early March, around VND 18,200 per liter. The 24.1% increase in April has not yet been captured in the March reading.

The transmission from fuel prices into CPI operates through two layers. The direct layer hits the transportation basket almost immediately, within the same month an adjustment occurs. The indirect layer works through logistics costs pushing into food, beverages, and consumer goods; this typically takes one to two months to filter through the basket. March CPI shows the direct layer beginning to bite; the indirect effect has not yet materialized.

The State Bank of Vietnam has held its policy rate at 4.50% since the start of the year. Twelve-month depositors at the Big Four banks currently earn 5.8-6.5%, leaving real deposit yields in the range of 1.1-1.8 percentage points. That looks comfortable, but the picture changes if April CPI rises to 5%: real yields would narrow to below 1 percentage point, a level the SBV has historically treated as a signal to reassess its policy rate.

Using a standard passthrough framework, each 50 basis point increase in retail fuel prices over a quarter tends to add roughly 15-20 basis points to CPI through the direct channel, before accounting for indirect logistics effects. Given the 24.1% rise in E5 RON92 across April, the direct channel alone will apply meaningful upward pressure on April CPI.

Oil and Gas Stocks Heading into May 5

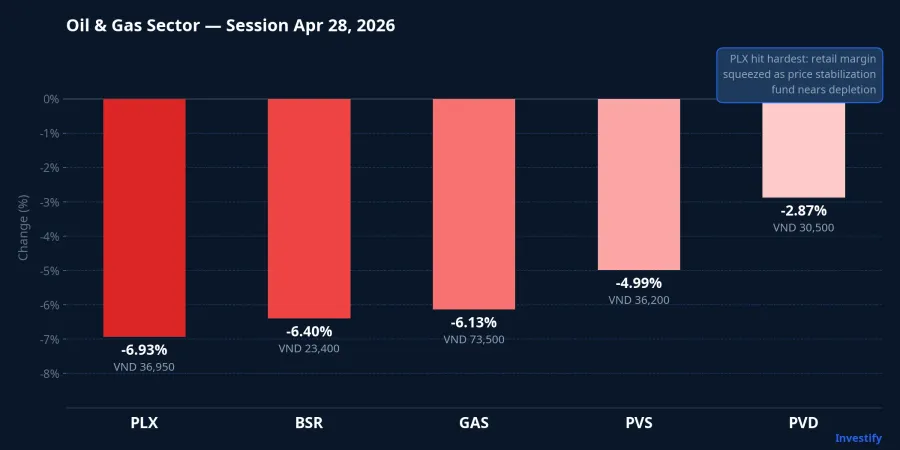

On April 28, the day the VN-Index fell 1.16%, the oil and gas sector divided sharply along business model lines. PLX dropped 6.93% in a single session, moving counter to rising Brent, because the downstream fuel retailer absorbs losses when input costs rise faster than regulated output prices and the stabilization fund can no longer cushion the difference. BSR fell 6.40% and GAS fell 6.13% the same day. PVD and PVS, representing the drilling services and technical services segment, declined 2.87% and 4.99% respectively.

By April 29 the group had recovered modestly: PVS gained 4.97%, GAS and PVD each added around 2%, and PLX and BSR recovered 0.54-0.85%. However, that session's trading occurred before the 126 USD print was public; the market had not priced in the new Brent level. May 5 will be the first session where the sector trades on the information that Brent is at a four-year high.

Reading the group's reaction requires distinguishing three separate forces. The first is the direct revenue impact on upstream production: GAS and, to a degree, BSR benefit when crude prices are elevated. The second is the lagged impact on drilling service order flow, as operators may not immediately commit to increased capital spending: PVD and PVS will depend on those decisions. The third is the squeeze on retail margins: PLX is most exposed here when the stabilization fund is depleted. The three forces are not in phase with each other, which means the simple thesis "oil up, oil stocks up" does not apply uniformly across the sector.

Signals Worth Tracking

Four days of market closure create a window during which the story can develop in multiple directions. Three signals deserve close attention when trading resumes:

CENTCOM news. If the military option is approved, Brent may hold or extend above 120-130 USD. If the option is withdrawn and talks resume, Brent could pull back toward 100-110 USD. This is the primary variable determining the price base going into the May 9 fuel adjustment.

The May 9 fuel price adjustment. This is the most concrete measure of how much remaining transmission from Brent at 120-130 USD flows through to retail prices. The magnitude of this adjustment will show how many additional percentage points are added to the transportation basket for May CPI.

April CPI (to be released late May). This is the most important policy signal. If April CPI exceeds 5%, real deposit yields at Big Four banks narrow below 1 percentage point and the probability that the SBV reconsiders its 4.50% policy rate increases materially.

Monitoring these three data points in order of timing will show how the transmission chain from Brent at 126 USD reaches both savers holding term deposits and investors holding oil and gas equities. The May 9 adjustment and the late-May CPI release will be the two decisive readings of the month ahead.