On Saturday, May 2, 2026, more than 30,000 Berkshire Hathaway shareholders gather at CHI Health Center Omaha for the annual meeting many call the "Woodstock of Capitalism." This year brings one fundamental change: the person stepping up to open the meeting is Greg Abel, CEO of Berkshire Hathaway, not Warren Buffett.CBS News Since 1965, it is the first time the familiar stage has operated without Buffett in the executive seat. Warren Buffett, Chairman of the Board of Berkshire Hathaway, remains in the room, but operational authority transferred to Abel on January 1, 2026.

This milestone raises an interesting question for any investor: can the investment philosophy someone builds over more than 60 years survive after that person steps aside? The question is not just about Berkshire. It touches how we think about personal discipline in investing. Can principles become lasting habits, or does everything fade the moment circumstances change?

The First Test: Hold Steady or Change Course?

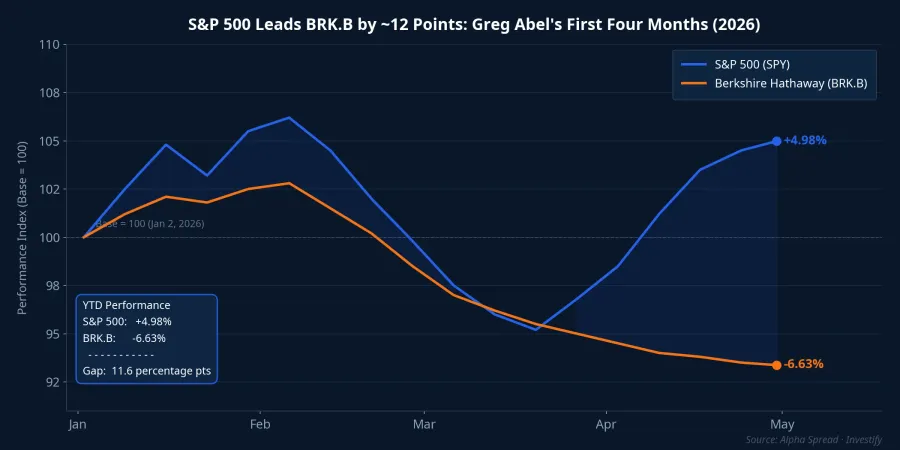

Abel's first four months were not a smooth start. Through the end of April, BRK.B was down 6.63% year-to-date while SPY gained 4.98%, a gap of nearly 11.6 percentage points in the S&P 500's favor.Alpha Spread To make it concrete: VND 100 million placed in SPY at the start of the year grew to roughly VND 105 million, while the same amount in BRK.B was worth approximately VND 93 million.

But the cause is not a mistake by Abel. Berkshire holds a very large allocation in cash and Treasury bills, and relatively little in large-cap technology stocks. When interest rates fall and growth stocks lead the market, a portfolio tilted toward value and cash like Berkshire's will naturally fall behind. This is precisely the structure Buffett chose and maintained for many years. Abel has changed nothing. His message is deliberate silence: no chasing the market's leaders despite very real pressure from analysts and the financial press. That is the most telling signal of the first four months.

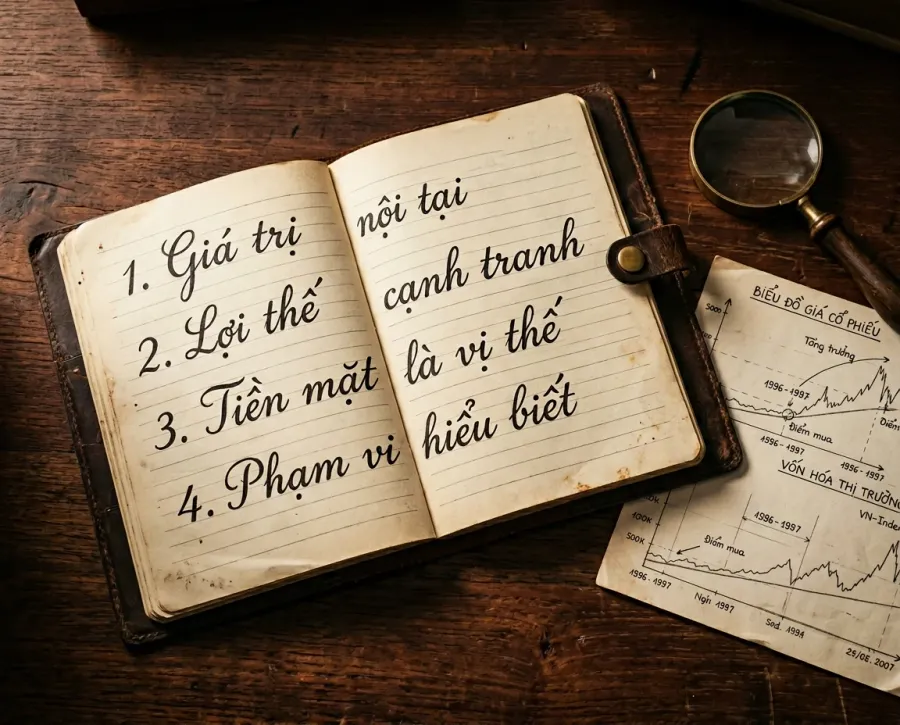

Four Principles Buffett Embedded in Berkshire's Structure

What many people forget is that Buffett's philosophy is not a stock list or a valuation formula. He turned it into a way of organizing and operating a company, which means it can keep running even when its creator is no longer standing there every day.

Intrinsic value before market price. Berkshire repurchases its own shares only when the market price falls below its estimated intrinsic value, and it does not pay a dividend if each retained dollar can generate more than a dollar of value when reinvested. In his first letter to shareholders as CEO, Abel reaffirmed this principle exactly. This is not ceremonial language: it is a concrete capital-allocation discipline applied to every financial decision the company makes.

Durable competitive advantage. Berkshire does not own "stocks"; it owns businesses with high barriers to entry: GEICO in insurance, BNSF in railroads, Berkshire Hathaway Energy in utilities. Each shares the quality of stable, cycle-resistant cash flows that are difficult to replicate in the short term. When buying listed equities, Buffett applies the same standard: what advantage does this business hold that competitors will struggle to copy over the next ten years? That question filters out most things that are compelling in the near term but lack genuine foundations.

Cash as optionality, not idle capital. Buffett has long called Berkshire's cash and Treasury holdings "dry powder." It sits there not out of laziness in deploying capital, but because when markets fall, the investor with cash ready can buy at the best prices. Holding cash while markets rise is not missing an opportunity; it is preserving the ability to act decisively when the market offers you a fair price.

Circle of competence. Through the dot-com bubble of the late 1990s, Buffett passed on nearly every technology stock. The reason was straightforward: he did not understand those business models well enough to value them. Better to miss an entire rally than to buy something you cannot explain how it earns money.

All four principles have been embedded in Berkshire's organizational structure, not merely held in one person's head. The company's decentralized governance model, where the parent allocates capital and each subsidiary runs itself, means Abel inherited a machine that has operated on these four pillars for decades. Leadership changes; the principles do not — at least not yet.

Practical Takeaways for Vietnamese Retail Investors

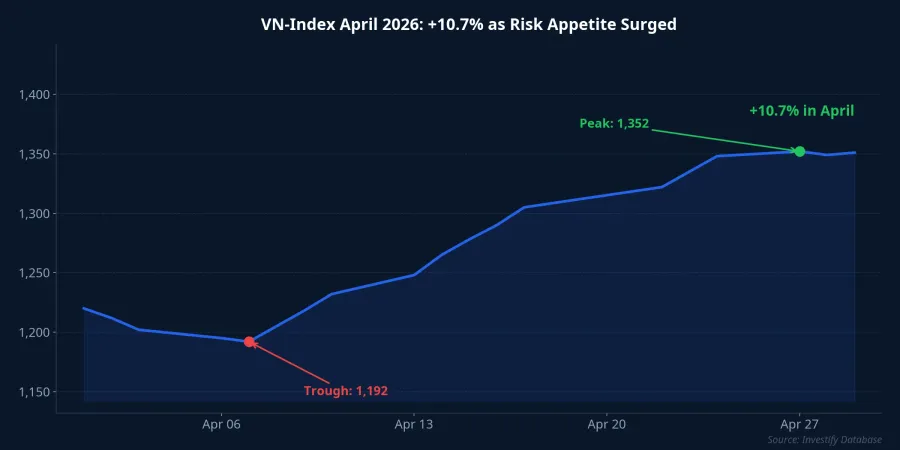

The VN-Index gained 10.7% during April 2026, enough for many investors to feel they are missing out if they do not act immediately. This is precisely the environment where Buffett's four principles become most relevant.

Discipline matters more than short-term results. With BRK.B trailing SPY by nearly 12 percentage points over four months, the pressure on Abel to "do something different" was intense. He did not. Individual investors often face an equivalent situation: their portfolio lags the VN-Index for a few months, and the impulse is to rotate out or chase whatever sector is running hot. Berkshire's 60-year track record suggests that impulse usually leads to buying at peaks and selling at troughs, the opposite of what actually builds wealth over time.

Own businesses, not tickers. Before placing an order, ask yourself this: if the exchange closed for five years and you could not sell, would you still want to own this piece of the business? That question eliminates most "hot" names and keeps the businesses with real, durable advantages. No complex calculation required — just an honest answer.

Cash is a position. When the VN-Index rises sharply, the pressure to deploy all available cash is real. But the way Berkshire keeps a substantial portion of its assets outside the market for years is a useful reminder: participating is not always better than waiting. Maintaining 10–20% cash when an index has risen strongly in a single month is a common defensive posture that preserves room to act when the market corrects.

Leverage destroys long-term thinking. Berkshire virtually never borrows on margin to buy equities. The core reason: borrowed money forces you to be right on the lender's timeline, not the business's timeline. When markets become volatile, high-leverage investors must make decisions under maximum psychological pressure, the worst possible condition for sound investment judgment.

A Question That Takes Years to Answer

On Saturday morning in Omaha, Abel will field hundreds of shareholder questions. But the most important one — whether Buffett's philosophy can survive without him — cannot be answered at a single annual meeting. The answer lies in whether Abel maintains capital-allocation discipline through several quarters of headwinds, whether he resists the pressure to track the S&P 500 by rotating into growth stocks, and whether he preserves the decentralized culture when one of the subsidiaries makes a mistake. Those questions need years to resolve.

For Vietnamese individual investors, this is a good moment to revisit their own discipline checklist. What is the cash allocation right now? Is the portfolio tilted toward genuinely strong businesses or toward whatever names have momentum? What is the leverage level? More than 60 years of Buffett did not leave behind a stock list to copy. He left a set of principles simple enough to remember and durable enough to carry through many market cycles. That is worth far more than any single position he ever held.