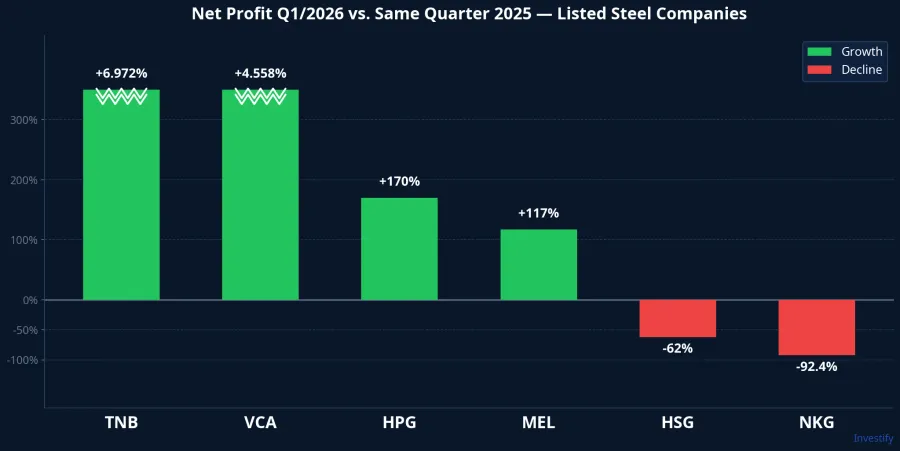

Q1/2026 delivered a striking paradox in Vietnam's listed steel sector: how can the same industry in the same quarter produce one company with nearly 7,000% profit growth while another loses 92% of its earnings?

Thep Nha Be (TNB) — whose predecessor VITHACO was established in 1967, nearly 25 years before Hoa Phat was founded — reported net profit of VND 5.25 billion in Q1/2026, up 6,972.71% year-on-year.DNSE Steel VICASA (VCA) grew 4,558% in the same quarter. Me Lin (MEL) rose 117%. Hoa Phat (HPG) posted net profit of VND 9,056 billion, up 170%.Tinnhanhchungkhoan On the other side: Nam Kim (NKG) barely earned VND 5 billion, down 92.4%. Hoa Sen (HSG) lost 62% of its earnings.

Four triple-to-quadruple-digit gains alongside two deep declines in the same earnings table — this is not irrational. It reflects three concurrent mechanisms: domestic demand recovery, margin expansion in the electric arc furnace (EAF) construction steel segment, and an extremely low Q1/2025 earnings base that was close to zero. Breaking down each mechanism reveals which figures reflect real structural change and which are purely numerical artifacts.

Mechanism 1: Domestic Construction Steel Demand Recovery

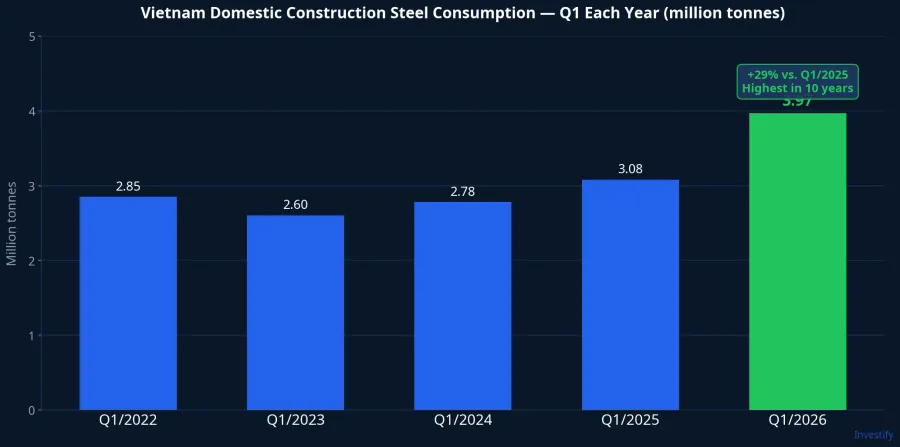

Q1/2026 domestic construction steel consumption reached approximately 3.97 million tonnes, up roughly 29% year-on-year.Bao Xay dung This is the highest Q1 figure in 10 years for the construction steel segment — a direct result of a public investment cycle that was activated in mid-2025. The North–South Expressway Phase 2, metro lines in Hanoi and Ho Chi Minh City, regional ring roads, and new industrial zones in Hai Phong and Binh Duong all drove construction steel demand to a multi-year peak. Construction steel output grew over 24% in the same quarter.

TNB and VICASA benefited most directly from this mechanism. Both companies focus on producing wire rod, rebar, and structural steel for the domestic construction market. They have no significant galvanized steel export capacity like NKG or HSG, and they are not exposed to competition from cheap Chinese imports in overseas markets. When domestic construction demand recovers, their volumes translate directly into revenue without needing favorable exchange rates or international logistics support.

HPG shares the same mechanism: it sold approximately 3 million tonnes of steel in Q1/2026, up 26% year-on-year.CafeF The key difference is absolute scale: a 26% volume increase at HPG pushed profit from roughly VND 3,350 billion to VND 9,056 billion. The same demand tailwind applied to TNB produces only VND 5.25 billion in net profit — because HPG's market cap is roughly 700 times larger than TNB's.

Mechanism 2: EAF Margins Expand While Galvanized Is Squeezed From Both Ends

Domestic construction steel selling prices rose approximately 10–13% year-on-year in Q1/2026.Bao Xay dung At the same time, steel scrap — the primary input for the electric arc furnaces (EAF) operated by TNB and VICASA — rose only approximately 3.5% year-on-year. This spread creates roughly 7–10 percentage points of gross margin expansion for domestic EAF producers.

The picture on the other side is the complete opposite. Coking coal — the input for Hoa Phat's basic oxygen furnaces (BOF) — rose approximately 22.5% year-on-year. Hot-rolled coil (HRC), the imported raw material that NKG and HSG use to produce galvanized and color-coated steel, rose approximately 22.6%. NKG and HSG faced the worst of both worlds: sharply higher input costs while export selling prices were kept low by cheap Chinese steel competition. Galvanized steel margins were compressed from both ends simultaneously.

Same quarter, same sector, two different furnace technologies — two completely different cost pictures. This is not a temporary stroke of luck. It is a structural position in the steel value chain that determines who benefits when two types of raw material inputs diverge in price.

Mechanism 3: Q1/2025 Earnings Base Was Near Zero

The third mechanism is pure arithmetic. TNB's net profit in Q1/2025 was approximately VND 75 million — not 75 billion, but 75 million. VICASA's in the same quarter was approximately VND 37 million. When the denominator is close to zero, any recovery in absolute profit terms — however modest by industry standards — produces an extreme percentage growth rate.

To illustrate: TNB's absolute profit increased by VND 5.175 billion in Q1/2026. That figure represents approximately 0.06% of the incremental profit HPG recorded in the same quarter. Yet the 6,972% percentage figure placed next to HPG's +170% makes TNB appear to be the sector's most dramatic turnaround. This is why percentage growth rates cannot be used to compare investment quality across companies of vastly different sizes when prior-year earnings bases are uneven.

Three Mechanisms, Three Different Durability Levels

What matters more than the percentage figures is how each mechanism is likely to evolve in coming quarters.

Mechanism 1 is the most structurally durable. Vietnam's public investment program is in peak disbursement for the North–South Expressway, metro lines, and high-speed rail preparation phases. Construction steel demand could sustain double-digit growth through 2026 and into 2027. This force continues to benefit TNB, VICASA, MEL, and HPG in upcoming quarters.

Mechanism 2 is the most fragile. The 7–10 point spread between domestic selling prices and scrap costs is a temporary result of inventory cycles and raw material sentiment. If domestic scrap prices start tracking coking coal and HRC internationally (both up approximately 22%), this margin could compress sharply as early as Q3/2026. This is a variable to monitor monthly, not quarterly.

Mechanism 3 is a one-time effect. When TNB reports Q2/2026, the comparison will be against Q2/2025 — a quarter that already had higher earnings than Q1/2025 due to seasonal construction patterns. The percentage growth rate will naturally fall back to double or low triple digits, even if absolute profits continue to increase. This is not deterioration; this is the arithmetic returning to earth once the base-effect tailwind expires.

How to Read Steel Sector Earnings Reports

Absolute profit figures matter more than percentage growth rankings when comparing companies of radically different sizes. TNB trades at approximately VND 9,000 per share with a market cap of roughly VND 300 billion and near-zero trading liquidity across many recent sessions. The +6,972% narrative is a structural signal about the industry, not a trading call on a stock with negligible liquidity.

The real fault line in Q1/2026 steel sector earnings is not company size — it is sales channel. Companies focused on the domestic market and construction steel (HPG, TNB, VICASA, MEL) all improved earnings, regardless of their scale. Companies in the galvanized steel export business (NKG, HSG) all lost earnings, regardless of their scale. The differentiator is output structure and furnace technology, not balance sheet strength.

For investors with a 12–24 month analytical horizon, HPG completing approximately 41% of its full-year profit target in Q1 alone is a more meaningful reference point for assessing sector opportunity than chasing stocks with dramatic percentage headlines but negligible liquidity. When Q2/2026 arrives, Mechanism 3 drops out of the picture and the market will need to reprice the steel group based on Mechanisms 1 and 2 alone — that is the real test of the structural recovery thesis. Two variables worth tracking before Q2 results: domestic scrap prices (Mechanism 2 signal) and public investment disbursement progress (Mechanism 1 signal).