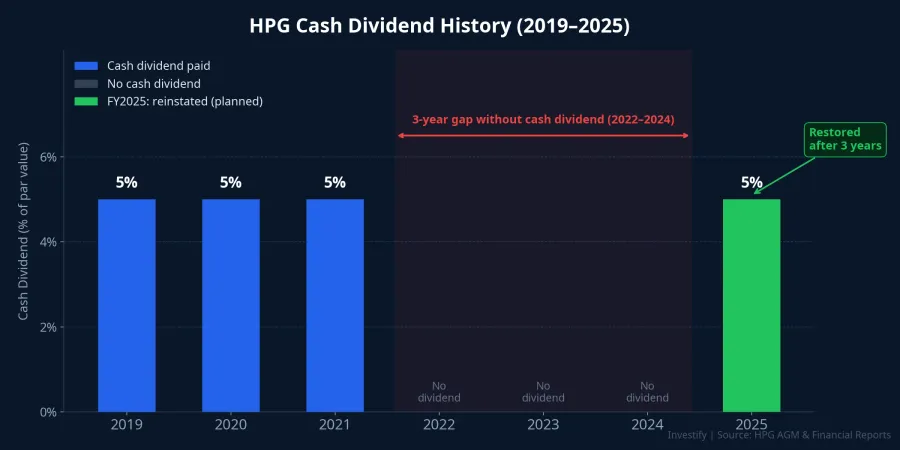

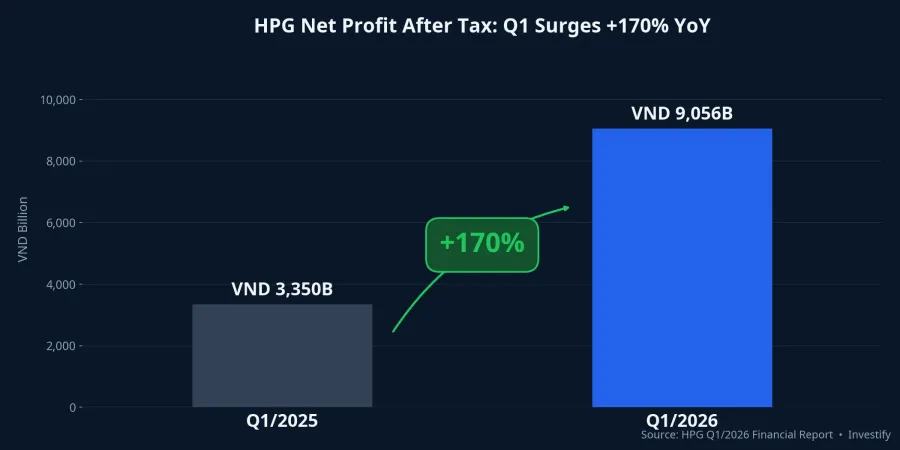

Hoa Phat's Annual General Meeting on April 21, 2026 handed shareholders two pieces of news at once: Q1/2026 net profit after tax hit VND 9,056 billion, up 170% year-on-year; and the FY2025 dividend was approved at 15% of par value — 5% in cash — marking the first cash payment since July 2022.Tinnhanhchungkhoan

The market's instinctive read is straightforward: Vietnam's leading steelmaker is returning cash after four years, signaling that the heaviest phase of investment is behind it and that cash is starting to flow back to shareholders. That reading is clean, intuitive, and emotionally satisfying. But set the dividend resolution alongside two other figures from the same meeting: the capital committed to Dung Quat 2 and the newly launched rail steel plant. A more complex picture emerges.

What the financials confirm: a governance commitment

The FY2025 dividend is structured as 10% in shares plus 5% in cash, equivalent to VND 500 per share.VnEconomy With approximately 7.68 billion shares outstanding, the cash portion amounts to roughly VND 3,838 billion returned to shareholders. The three fiscal years without a cash dividend (FY2022, FY2023, and FY2024) coincided with the trough of Vietnam's steel cycle and the period when capital was being funneled into the Dung Quat 2 complex.

What matters most is not the 5% rate itself but the commitment that came with it. Chairman Tran Dinh Long of Hoa Phat Group (HPG) stated at the AGM that the company commits to maintaining a cash dividend from 2026 onwards, with the specific rate depending on annual business performance.Etime This is a deliberate governance decision: management chose to bind itself to a distribution policy even while the investment cycle is still running. As long as operating cash flow stays sufficient, this commitment can be sustained in parallel with new capital spending.

Two readings lead to very different expectations: "no more use for the money" versus "profits large enough to invest and distribute at the same time." HPG sits firmly in the second scenario, and that distinction matters for anyone holding the stock.

Two major projects running in parallel

The Dung Quat 2 complex carries a total investment of approximately VND 85,000 billion, designed for a capacity of 5.6 million tonnes of hot-rolled coil (HRC) per year, which would lift HPG's total crude steel capacity to roughly 14.5 million tonnes.VnEconomy While several blast furnace and refining units came online during 2025, the full complex has not yet reached design capacity. Remaining capex and working capital requirements for the new capacity continue to weigh on cash generation through 2026.

Alongside that, HPG broke ground on a rail steel and specialty steel plant at the Dung Quat Economic Zone on December 19, 2025: VND 14,000 billion total investment, 700,000 tonnes per year capacity, equipment sourced from Germany and Austria.Government Newspaper By the time of the April 2026 AGM, construction was roughly 35% complete, with imported equipment installation scheduled to begin in June 2026 and first production targeted for Q1/2027. This is a brand-new investment cycle just getting underway, not an old one winding down.

Put the numbers side by side: shareholders receive approximately VND 3,838 billion in cash while the company simultaneously carries a VND ~85,000 billion project still not at full capacity and a fresh VND 14,000 billion project just started. This is deliberate capital allocation, not surplus cash after the spending is done.

Profits large enough to fund both

The end-2025 balance sheet shows HPG entering 2026 with VND 8,301 billion in cash and equivalents, against total debt of VND 92,174 billion (short-term VND 64,695 billion, long-term VND 27,479 billion). Full-year 2025 operating cash flow reached VND 17,366 billion, reflecting the group's strong self-funding capacity even at this scale of investment.

Q1/2026 added VND 9,056 billion in net profit after tax, representing 41% of the full-year profit target of VND 22,000 billion in just three months.Tinnhanhchungkhoan The 2026 full-year revenue target stands at VND 210,000 billion (up 32.6%), with projected net profit growth of 41.8%.Doanhnhan

The key insight here is that the same dividend action carries entirely different meaning depending on its origin. "Profits have crossed the threshold where investing and distributing can happen simultaneously" is a fundamentally different situation from "there is nowhere left to put the money." HPG is in the former position, which is precisely the message management is communicating.

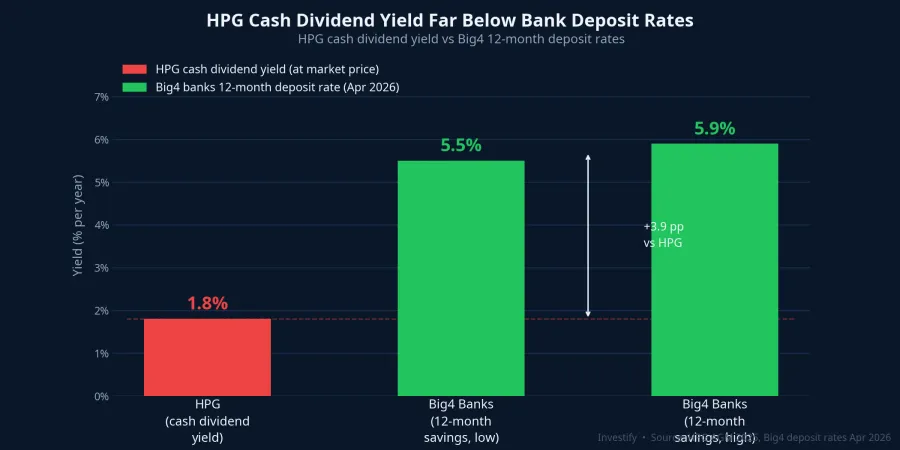

A 1.80% yield: calibrating the right expectation

At HPG's closing price of VND 27,750 on April 29, 2026, the VND 500 cash dividend translates to a cash dividend yield of approximately 1.80% at market price. By comparison, 12-month deposit rates at Vietnam's Big4 state banks currently range from 5.5% to 5.9% per year.

A 1.80% yield places HPG clearly in the growth-stock-with-a-token-payout category, not alongside high-yield names like Sabeco or the banking sector. Investors expecting HPG to become a reliable income machine will be disappointed when they compare it directly to bank deposits. The cash dividend at this level is a supplemental return on top of price appreciation expectations, not a competitive passive income stream on its own.

Chairman Long's candid remark at the AGM — "As long as I'm Chairman, I will never advise shareholders to buy Hoa Phat shares" — is entirely consistent with this picture: this is the posture of a management team running a company in the middle of a massive, unfinished investment programme, not one that has pivoted to steady-state distributions.

Signals to watch in the coming quarters

The 5% cash dividend is genuinely good news and a clear governance commitment. But it is the opening move of a new distribution policy, not confirmation that the investment cycle has closed. A harder conclusion, that HPG has truly entered a mature distribution-focused phase, requires more data.

Three signals are worth monitoring: the pace at which Dung Quat 2 ramps toward its target of roughly 15% higher HRC output in 2026; the progress of equipment installation at the rail steel plant from June 2026 and whether the Q1/2027 production target holds; and critically, whether profit margins hold up as HRC prices and iron ore costs move through their own cycles. If the cash dividend is maintained or raised in 2027–2028 while operating cash flow remains stable, that will be the real confirmation that HPG has entered its mature phase. This first reinstatement, however welcome, is not yet that confirmation.