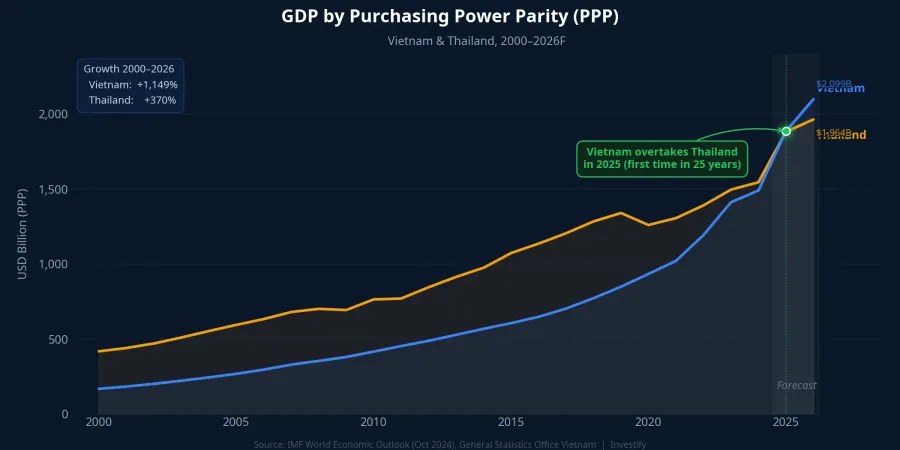

On April 28, 2026, Vietnam's General Statistics Office released a figure that analysts had been watching for years: Vietnam's 2025 GDP by purchasing power parity (PPP) reached approximately $1.885 trillion, edging past Thailand at $1.881 trillion.Tuổi Trẻ The gap is approximately $4 billion — thin in absolute terms, but it marks the first reversal in a 25-year ranking.CafeF This did not happen overnight. In 2000, Vietnam's PPP-adjusted economy was less than 40% the size of Thailand's. The gap narrowed steadily across two decades — not through a single policy breakthrough, but through the compounding of structural shifts. And by current forecasts, it is set to widen further in Vietnam's favor.

PPP vs Nominal GDP: Two Different Stories

Before drawing investment conclusions, the measurement distinction matters. PPP converts national output using a standardized basket of goods, stripping out domestic price-level differences. A bowl of pho in Hanoi costs far less in dollar terms than an equivalent meal in Bangkok — but PPP records the real consumption value, not the exchange-rate-adjusted dollar price. Nominal GDP, by contrast, converts via market exchange rates, making it the measure of cross-border financial weight and the scale that international capital flows respond to.

By nominal GDP, Vietnam has not yet overtaken Thailand. The GSO and IMF both project that nominal parity could arrive between 2027 and 2030. The gap between the two measures reflects Vietnam's lower domestic price level — the same consumption basket costs fewer dollars in Vietnam than in Thailand. For investors, PPP tells the story of productive capacity and real domestic demand; nominal GDP tells the story of asset pricing in dollar terms and cross-border capital weight. The April 28 milestone is a structural marker for the long-run story, not a short-term trading signal.

Three Structural Forces Behind 25 Years of Catch-Up

The journey from 40% to parity compressed three distinct forces into Vietnam's growth model.

First: manufacturing as the backbone. FDI disbursements in 2026 are forecast to grow 9–10%, with approximately 83% flowing into manufacturing. The sustained scale of Samsung's investment commitments signals that the high-tech factory model has durable foundations, not a transient wave. Industrial parks in Bac Ninh, Hai Phong, and Binh Duong now have sufficient capacity to absorb large-scale supply chain relocations out of China.

Second: geopolitical positioning. Vietnam's extensive free trade agreement network — the broadest in Southeast Asia — combined with its geography between China and major consumer markets has placed it at the center of supply chain diversification over the past five years. Thailand, meanwhile, is contending with rapid demographic aging and softening exports as US demand weakens and tariffs rise.

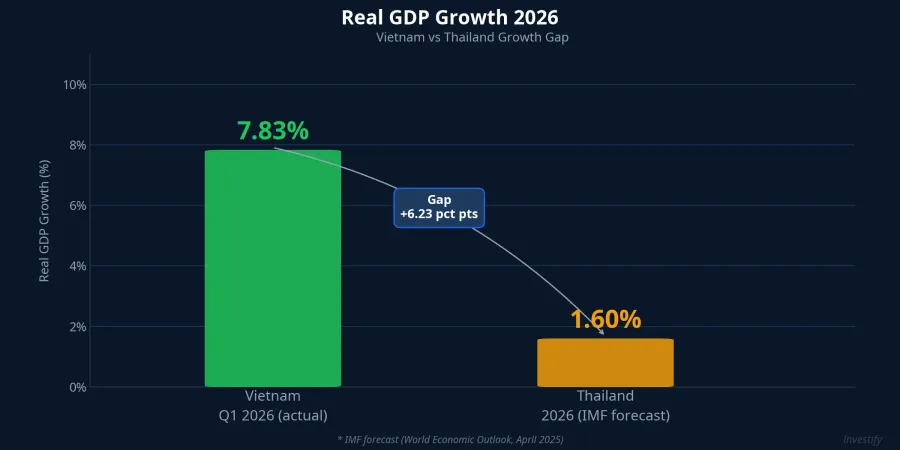

Third: the growth differential. In Q1 2026, Vietnam's real GDP grew 7.83% year-on-year, while the IMF projects Thailand's full-year 2026 growth at approximately 1.6%.VietnamPlus A gap of nearly 6 percentage points, sustained across consecutive years, is the arithmetic reason PPP forecasts put Vietnam at approximately $2.099 trillion versus Thailand's approximately $1.964 trillion for 2026 — the gap expanding from roughly $4 billion to roughly $135 billion in a single year.

What This Means for Investors

The PPP milestone does not trigger a buy or sell order on its own. But it reframes three layers of medium-term decision-making.

Foreign capital flows and the upgrade roadmap. FTSE Russell confirmed Vietnam's upgrade to Secondary Emerging Market status, effective September 21, 2026, with multiple allocation phases extending into 2027.LSEG Passive flow estimates range from $500 million to $1 billion in mandatory inflows; index-tracking ETFs could add meaningfully to that figure. On the MSCI side, a potential watchlist inclusion in 2026–2027 could open the door to a full upgrade around 2028 — at substantially larger capital scale than FTSE. Having a macro backdrop where Vietnam has now crossed Thailand in PPP, exactly as the FTSE upgrade cycle begins, gives the re-rating narrative a credible structural anchor.

Relative valuation in regional context. The VN-Index closed at 1,875.84 on April 28, having swung through a 16.38% range in Q1. Vietnam's market P/E remains below comparable emerging markets in the region, despite listed-company earnings growth tracking closely with GDP momentum. That valuation discount does not close instantly — re-rating takes time and real capital inflows — but a superior structural growth profile is one of the inputs that narrows it in the medium term.

Access options for individual investors. The economic growth story plays out over years, not sessions. For retail investors, three natural access points fit different participation levels: direct equities suit investors who have time to track individual names and are comfortable with sector-specific volatility; Vietnamese equity fund certificates suit those who want exposure to the aggregate growth story without stock selection, accessible from VND 100,000 through fund distribution platforms; and ETFs tracking VN30 or indices likely to be included in FTSE offer intraday liquidity that open-ended funds do not.

Risks to Hold Alongside the Milestone

A long-run structural milestone does not eliminate short-term volatility. Foreign net selling through April 28 has totaled approximately negative VND 43.9 trillion in 2026, reflecting a wait-and-see posture ahead of the FTSE upgrade and global market uncertainty. FTSE inflows are phased across multiple tranches rather than entering in a single event — which creates both a buffer and a risk that market expectations run ahead of actual inflows.

The 7.83% Q1 growth rate is partly supported by a low base from Q1 2025. The more important signal is whether that pace holds through H2 2026 as the comparison base rises. On Thailand's side, an unexpected recovery — from aggressive fiscal stimulus or a sharp rebound in tourism — could temporarily narrow the PPP gap, though the full-year 2026 forecast still tilts heavily toward Vietnam.

Signals Worth Tracking

The question is no longer when Vietnam catches Thailand in PPP terms — that answer arrived on April 28. The next question is whether the gap widens fast enough to pull regional capital allocation meaningfully toward Vietnam, and at what pace.

Four signals worth tracking through the second half of 2026: foreign flow dynamics around the FTSE effective date of September 21 and subsequent allocation tranches; MSCI's mid-2026 semi-annual review and whether Vietnam earns watchlist placement; Q2 and Q3 GDP growth, specifically whether the above-7% pace holds as the base rises; and actual FDI disbursements for the full year 2026, especially in the manufacturing segment.

The 2026 PPP forecast showing approximately $135 billion of separation suggests structural momentum is on Vietnam's side. The April 28 milestone is a confirmation point, not a starting point. How quickly that structural shift translates into market repricing will depend on the specific events ahead — but the direction of the macro case has become harder to argue against.