Something striking happened on the morning of April 28, 2026: VIC gained 6.88% to reach VND 226,700, setting an all-time high and pushing Vingroup's market capitalization to VND 1,747 trillion. At the same moment, the real estate sector index dropped 1.53%, placing it among the worst-performing sectors of the session.Tin Nhanh Chứng Khoán Two sharply divergent moves in the same morning raise an important question: what valuation framework is the market now applying to VIC?

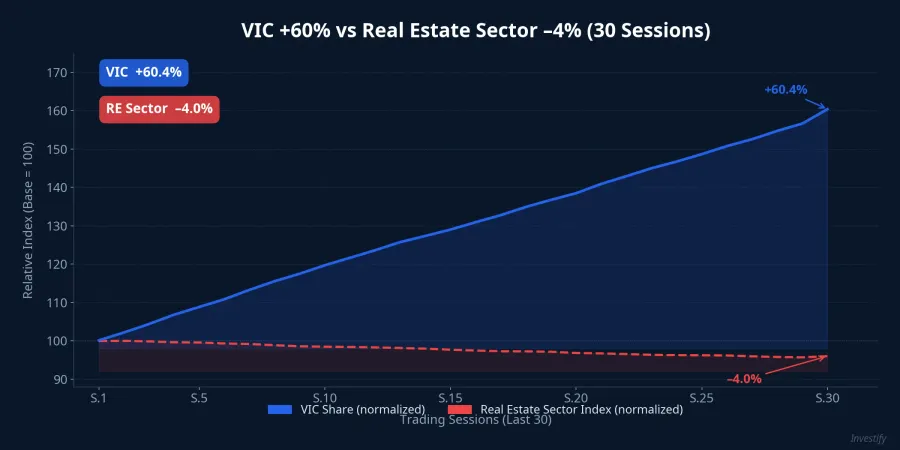

This divergence did not emerge overnight. The data tells the story: over roughly one month, VIC rose from around VND 141,000 to 226,700 — a gain of approximately 60%. During that same period, outstanding real estate loans reached VND 4,541 trillion and a proposed progressive tax on second-home properties continued to weigh on sector sentiment. If VIC were behaving purely as a real estate stock, these two trends could not coexist.

Capital Is Selecting Vingroup, Not the Sector

What makes this divergence more significant is its consistency. On the morning of April 28, VIC and VHM together contributed more than 30 points to the VN-Index, which closed at 1,886.05. VHM gained 6.73% to VND 150,700 — both Vingroup flagships bought aggressively while the rest of the real estate sector was sold. This is not a case of "sector rally lifting large-caps"; this is capital specifically rotating into Vingroup and out of the broader category it is traditionally grouped with.

Institutional signals point the same direction. Finland-based PYN Elite Fund, a long-standing foreign investor in Vietnam, disclosed in its Q1/2026 report that its capital was being concentrated in the Vingroup cluster even as retail investors showed little reaction to earnings.VietnamBiz At the regional level, Vingroup's current market cap has placed it among the top 5 largest companies in Southeast Asia by market capitalization, alongside DBS Group, Delta Electronics, and OCBC — a position that a pure real estate valuation cannot credibly explain.VnExpress

Three Drivers That Have Nothing to Do With Housing

To understand why capital is moving this way, it helps to look at what has changed at the company level over the past month.

Profit target: At the annual general meeting on April 22, Vingroup approved a target of VND 485,000 billion in revenue and VND 35,000 billion in after-tax profit for 2026 — three times the VND 11,100 billion achieved in 2025.Thời Báo Tài Chính A leap of that magnitude cannot come from Vinhomes alone. It implies meaningful contributions from VinFast and the technology segments.

EV tax policy: On April 24, the National Assembly passed an amendment to the excise tax law, locking in a 3% rate for electric passenger vehicles with fewer than 9 seats through the end of 2030 — rather than expiring in February 2027 as previously scheduled.VnEconomy That extension of nearly four additional years is a direct tailwind for VinFast, the only large-scale EV producer listed within the Vingroup ecosystem. At the AGM, Phạm Nhật Vượng, Chairman of Tập đoàn Vingroup (VIC), declared that "VinFast will forever be an electric vehicle company," anchoring the group's identity to its EV division rather than its residential property arm.VietnamBiz

Delivery target: VinFast is targeting approximately 300,000 electric cars and around 1 million electric motorcycles in 2026. If those targets are met, the EV segment would graduate from an "expectation story" to a segment generating substantial operating cash flow. The market appears to be pricing in that outcome ahead of confirmation.

The Valuation Framework: Three Segments, Three Different Multiples

Here is the core analytical point: when investors label VIC a "real estate stock," they are implicitly applying Vinhomes' P/E and NAV to the entire conglomerate. That was a reasonable approximation until recently. But Vingroup today is a three-part structure with fundamentally different businesses and appropriate valuation multiples for each.

Vinhomes is valued on traditional real estate logic: credit cycles, land bank NAV, project completion cash flows. VinFast, at the global level, is valued on EV company multiples — Tesla, BYD, and Li Auto currently trade at roughly 1.5 to 8 times revenue. The remaining piece — VinAI, GSM, Vinhomes Smart City — is valued on tech and smart infrastructure growth rates. These three components do not simply add up under one common multiple.

When VIC hits an all-time high on the day the real estate sector sells off, it likely reflects the market beginning to assign larger weight to VinFast and the tech segment in its blended valuation — rather than anchoring entirely to Vinhomes as before. That is a framework shift, not merely short-term price noise.

Two Data Points That Will Resolve the Thesis

The genuine question is whether this repricing has solid operational backing or is still primarily expectation-driven.

The first signal is Vingroup's consolidated Q1/2026 financial report, expected by end of April. VinFast's contribution share in total consolidated profit will be the clearest read: if the EV segment has already begun delivering meaningful profit, the conglomerate valuation framework is grounded. If Vinhomes still accounts for the bulk, the VinFast narrative remains largely expectation at this point.

The second signal is VinFast's Q2 delivery volume. Hitting the 300,000-vehicle annual target requires sustaining roughly 75,000 deliveries per quarter. If Q2 maintains that pace, the current valuation has operational confirmation. If the quarter misses, the historical pattern for stocks that surge strongly ahead of cash flow confirmation suggests a 10–15% pullback from the peak is a realistic scenario.

The core thesis stands: VIC is no longer a pure real estate stock in the traditional sense. The market has begun shifting to a conglomerate valuation framework in which VinFast is the primary short-term price variable. The key risk is not the housing market — it is whether VinFast can confirm sufficient operating cash flow in coming quarters. Two data points to watch: the consolidated Q1/2026 financials and Q2 delivery volume. Both will be available in May.