On April 28, Abu Dhabi announced that the UAE would withdraw from OPEC and OPEC+ effective May 1 — ending more than five decades of membership in the cartel.CNBC In theory, a major producer breaking free from quota constraints to pump at will should signal an increase in supply and push prices lower. The opposite happened: Brent crude closed that same evening at $111.71 per barrel, up 3.22% on the day, while WTI touched $100/bbl for the first time since March.CNBC

Both events happened on the same day, but they do not carry the same weight. The big picture is straightforward: the volume of oil the UAE could plausibly add over the coming months is far smaller than the volume being disrupted every single day through the Strait of Hormuz. That asymmetry — not any confusion about market dynamics — explains why oil rallied on news that should have been bearish.

UAE's Exit: A Million Barrels Over Time, Not Overnight

The UAE is the third-largest oil producer within OPEC, behind Saudi Arabia and Iraq.OilPrice The country has long telegraphed a target of 5 million barrels per day by 2027,EIA and OPEC's quota system has kept UAE production well below its actual capacity. The gap between current output and full capacity is estimated at roughly 1 to 1.5 million bpd — the volume the UAE had effectively been "locking away" under cartel discipline.

UAE Energy and Infrastructure Minister Suhail Al Mazrouei framed the decision as reflecting "a policy-driven evolution aligned with long-term market fundamentals," not a reaction to short-term conditions.The National Abu Dhabi has clashed with OPEC over quota allocations repeatedly in recent years, consistently arguing that its share did not reflect its actual investment in upstream capacity. Exiting the cartel was the logical end-state of that long-running dispute.

That said, even if the UAE begins pumping at maximum capacity from May 1, the incremental supply cannot materialize instantly. Wells require technical ramp-up time, and approximately 1 million bpd of additional output would need to accumulate over many months, not days. Markets priced this timeline correctly.

Hormuz: Subtracting Millions of Barrels Every Day

The Strait of Hormuz carries around 20% of global energy consumption — crude oil and refined products from Saudi Arabia, Iran, Iraq, Kuwait, and the UAE itself all flow through this narrow passage.CNBC This was the ninth consecutive week of US–Iran conflict, and flows through the strait remain severely disrupted.CNBC

Iran relayed a message through Pakistan signaling willingness to pause hostilities if Washington lifted its naval blockade and agreed to a new framework for Hormuz transit. President Donald Trump rejected the proposal on the evening of April 27.CNBC With negotiations stalled, the volume held back every day remains measured in multiple millions of barrels — a magnitude that dwarfs anything the UAE might add incrementally over the next year.

The math is the story. One side is adding roughly 1 million bpd over twelve to eighteen months; the other is subtracting several million bpd each day the conflict runs. Markets are pricing the subtraction — the UAE announcement was background noise by comparison.

Brent Up 14.7% Over 30 Sessions

Brent's 30-session trajectory captures the full picture: a sustained climb from the $97 range into the $111 zone, closing at $111.71 on April 28. The trend reflects three overlapping drivers: the Hormuz supply disruption, resilient global demand, and now the strategic uncertainty introduced by the UAE's restructuring of its output policy.

Vietnam's April 29 Fuel Adjustment and the CPI Pressure Building

Vietnam's Ministry of Industry and Trade moved the next fuel price review to Wednesday, April 29, instead of Thursday April 30, to avoid the public holiday.VietStock Domestic fuel pricing in Vietnam references Singapore product prices, which track Brent closely, averaged over a 7–10 day window before each review. For the April 29 window, Brent moved from approximately $98.48/bbl on April 21 to $111.71/bbl on April 28 — a weekly gain of roughly 13.4%.

E5 RON92 petrol currently stands at VND 21,830/liter since the April 23 adjustment.Petrolimex With the Brent reference price surging through the review window, the April 29 adjustment is likely to push domestic prices higher. The critical unknown is how much buffer the Price Stabilization Fund can absorb — a variable that changes with every review cycle and is not publicly visible in real time.

The inflation baseline offers little comfort. Vietnam's CPI for March 2026 rose 4.65% year-on-year, the highest reading in five years, driven primarily by transport and fuel categories.VnEconomy Any further fuel price increase will feed into April and May CPI readings — not a single catastrophic spike, but a cumulative drag that becomes meaningful if Brent holds in the $105–$115 range through the second quarter.

Two Tiers of Oil Stocks: Opposite Directions, Different Timelines

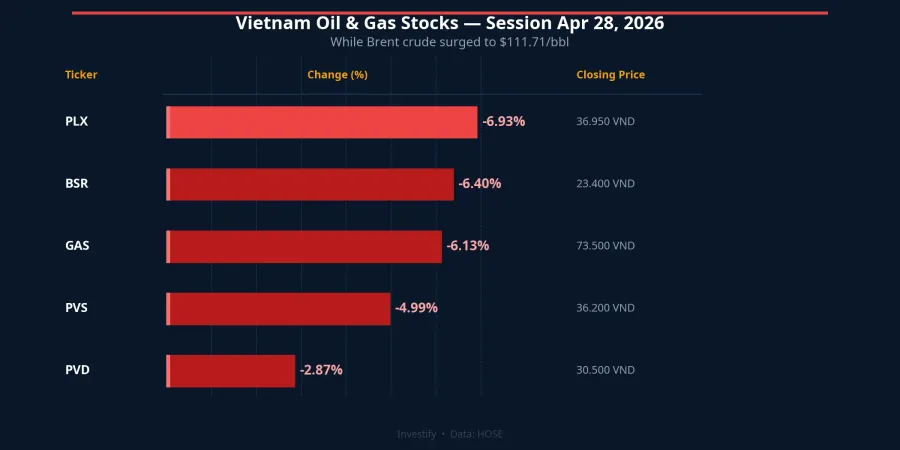

The April 28 session saw the entire Vietnam oil and gas sector fall sharply on the same day crude surged. This is not a paradox — it reflects two structurally distinct mechanisms playing out on different timelines.

The losers in a fast-rising input price environment: Petrolimex (PLX, -6.93%) and Binh Son Refinery (BSR, -6.40%) face the sharpest structural disadvantage in a rapid price spike. Both companies purchase crude and refined products at international spot prices but must sell domestically at the price set by the previous review period. That lag creates realized losses during the gap weeks at the start of every price surge — a mechanism that already pushed Petrolimex's petroleum trading segment to a loss of over VND 1 trillion in Q1 2026.VietStock The market is now pricing the likelihood of a repeat in Q2 if Brent sustains above $105.

The structural beneficiaries on a delayed timeline: PV Technical Services (PVS, -4.99%), PV Drilling (PVD, -2.87%), and PV Gas (GAS, -6.13%) tell a different structural story. Mid-term service contracts and drilling rig agreements are typically priced at fixed rates, insulating near-term revenue from daily Brent movements. The benefit flows through two channels: new contracts signed at higher rates as operators accelerate drilling, and expanded upstream service demand as producers push harder on existing fields. Both channels typically take two to four quarters to materialize. The April 28 selloff in these names reflects profit-taking after a strong April run and the broader VN-Index retreat — not a fundamental shift in the long-term upstream thesis.

The Only Variable That Matters Right Now: Hormuz

For the next two weeks, price direction will be determined by signals from the Strait of Hormuz, not from how OPEC restructures after the UAE's departure. If US–Iran negotiations produce a meaningful breakthrough before early May, a move back below $100/bbl is plausible on short-covering. Conversely, every additional day of disruption adds another increment to the domestic fuel price and CPI trajectory in May and June.

The UAE's OPEC exit is a genuinely significant development for the long-term architecture of global oil supply — it will reshape the cartel's composition, bargaining dynamics, and production ceiling frameworks for years to come. But for the price of petrol on April 29 and the behavior of Vietnam's oil stocks in May, the UAE's decision is close to irrelevant. Hormuz is the signal. Everything else is context.

For investors holding positions in the sector, the PLX/BSR versus PVS/PVD/GAS split remains the core analytical framework — near-term inventory-mechanism risk on one side, structurally positive but time-lagged upstream exposure on the other. Watch for: the outcome of US–Iran negotiations, the magnitude of the April 29 fuel adjustment, and April CPI data when it is released.