Since General Secretary of the Communist Party of Vietnam Tô Lâm signed Resolution 79-NQ/TW into effect on January 6, 2026, one phrase has circulated with growing enthusiasm in investment forums: "Vietnam's Temasek."Government The excitement is understandable — the Resolution mandates a comprehensive restructuring of the State Capital Investment Corporation (SCIC) toward a professional investment model, eventually forming a national investment fund. The problem is that many investors are reading the final destination on the blueprint while the country is still laying the first bricks.

What SCIC Is Today

Understanding where SCIC is going requires a clear-eyed view of where it stands. The corporation, led by Nguyễn Chí Thành, Chairman of the Members' Council of the State Capital Investment Corporation (SCIC), managed approximately 110 enterprises as of end-2024, with a book value of VND 53.4 trillion across an invested capital base of VND 183.2 trillion.Nguoi Quan Sat Key listed holdings include approximately 36% of Vinamilk (VNM), roughly 5.67% of FPT Corporation, 37.1% of Nhua Tien Phong (NTP), 36% of Sabeco, 31.14% of Vietnam Airlines, and 41.31% of DHG Pharma.

The core business model over the past two decades has been straightforward: receive equity stakes transferred from government ministries, collect dividends, and selectively divest. In the first half of 2025, SCIC collected over VND 5.1 trillion in dividends, with Vinamilk's annual dividend for 2025 alone contributing approximately VND 3.65 trillion.Thuong Hieu & Cong Luan The unusually high profit margins — most revenue comes from dividends, not active investing — reveal the structural reality: SCIC has been a state capital custodian, not a growth investor. That is precisely why Resolution 79 represents a genuine directional shift, not a continuation of the status quo.

The Two-Phase Roadmap

What the Resolution actually says about timing matters enormously.

The Resolution mandates a full restructuring of SCIC toward professional capital management, eventually establishing a national investment fund.VnEconomy But the design is deliberately sequenced into two distinct phases. During 2026–2027, SCIC's mandate focuses on four foundation tasks: reclassifying the entire asset portfolio, divesting according to a new decree on state enterprise classification criteria, receiving additional enterprise transfers, and — most critically — "completing the organizational structure, developing human resources, and building the legal framework." This is a consolidation and foundation phase, not a capital deployment phase.

Active investing at scale only becomes possible once the capital base reaches sufficient size. The Resolution permits SCIC to retain all after-tax profit from 2026 and subsequent years to build up paid-in capital, targeting VND 150 trillion within the next two to three years. That places the opening of the active investment phase somewhere around 2028–2030 — not this year, and not next.

Putting the Numbers in Regional Context

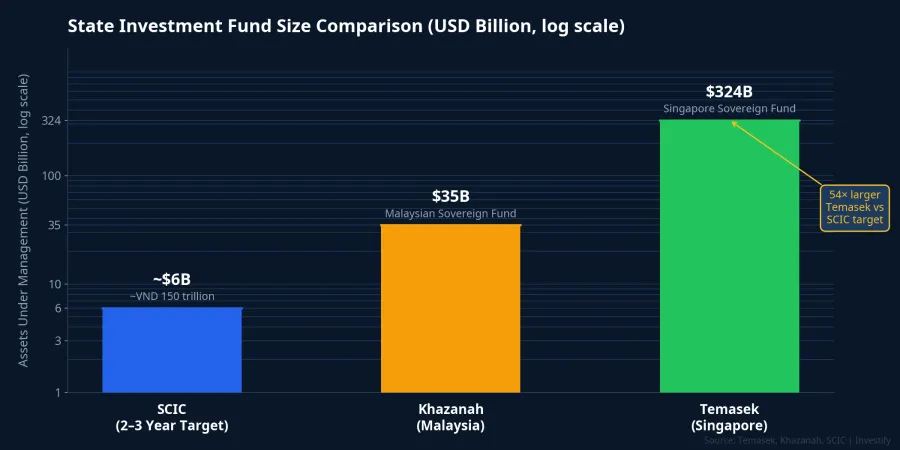

When analysts invoke Temasek as a reference point, the scale gap is the first thing worth internalizing.

As of March 31, 2025, Temasek's net portfolio value reached S$434 billion, equivalent to US$324 billion.CNBC Khazanah Nasional, Malaysia's sovereign wealth fund, reported total assets of RM156 billion — approximately US$35 billion — at end-2025.BusinessToday SCIC's capital target of VND 150 trillion translates to approximately US$6 billion after two to three years of profit retention.

The gap is roughly 54 times relative to Temasek and five to six times relative to Khazanah. Critically, the US$6 billion figure is the target after years of accumulation, not a current balance. Beyond raw capital, the governance gap is equally significant. Temasek reported an 11.8% SGD portfolio return over the twelve months to March 2025 across a globally diversified portfolio; Khazanah recorded a 5.2% annual return in 2025 across a multi-sector portfolio. SCIC currently operates within a state divestment mandate, has no mechanism for free-market capital deployment, and lacks a fund-standard portfolio performance reporting framework. Building that institutional capability is a central objective of the 2026–2027 phase.

Implications for Listed Holdings

If the 2026–2027 narrative is classification and divestment, the direct implication for retail investors is a reassessment of supply-side liquidity risk across SCIC's listed holdings.

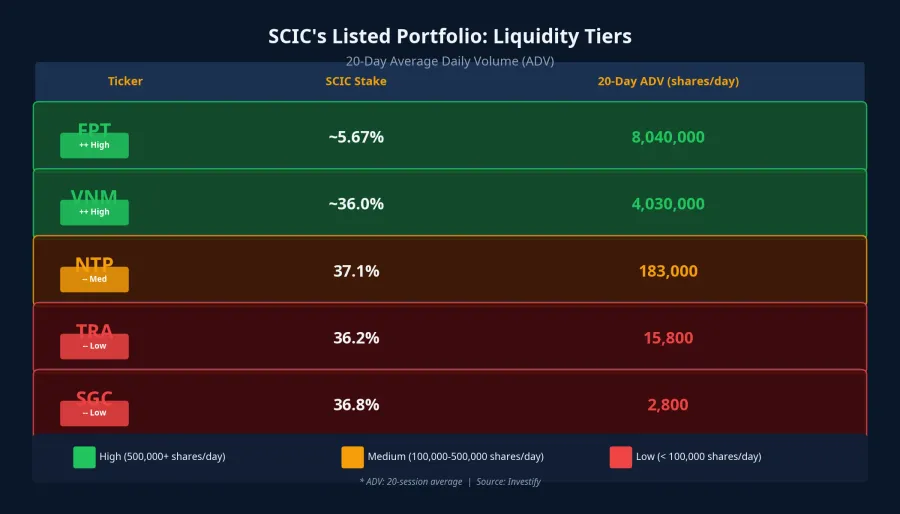

The most exposed names are those combining high SCIC ownership with low market liquidity. NTP carries 37.1% SCIC ownership against a 20-day average daily volume of approximately 183,000 shares — a single mid-sized block trade would absorb many days of normal activity. SGC (approximately 36.8% SCIC stake, ~2,800 shares ADV) and TRA (approximately 36.2%, ~15,800 shares ADV) sit in an even more vulnerable position, where a single negotiated block transaction could represent weeks of typical volume.

VNM and FPT occupy a different tier. With 20-day average volumes of approximately 4.03 million and 8.04 million shares respectively, both stocks have sufficient liquidity depth to absorb large transactions without material price disruption. The relevant question for these two is not immediate selling pressure, but classification: will VNM and FPT be designated as strategic long-term holdings under the new classification decree, or placed in the divestment category? That policy signal will determine supply-side dynamics for the next 18 to 24 months.

Four Signals Worth Monitoring

This policy creates a measurable transition period with four concrete indicators to track. First, the new state enterprise classification decree — this document determines which holdings SCIC retains and which it exits. Reading it carefully when published will be more valuable than any analyst note on the sector. Second, the dedicated SCIC decree that the corporation is proposing to the Ministry of Finance — this legal framework will define the operating model and investment mandate for the fund structure. Third, the pace of capital accumulation — monitoring whether SCIC reaches the VND 150 trillion target within the stated timeline provides a real-time check on the fund transition. Fourth, transaction activity at major holdings, particularly VNM, FPT, NTP, Sabeco, and Vietnam Airlines.

If Resolution 79 is implemented as designed, a genuine sovereign investment fund model should be visible by the second half of this decade. For the next 24 months, the dominant market signal from SCIC remains portfolio classification and divestment, not growth capital deployment. That gap between the long-term policy direction and the near-term operational reality is the most important thing for investors to calibrate before building positions around SCIC-held stocks. Which signal arrives first — the classification list or an early divestment transaction — will answer that question in the months ahead.