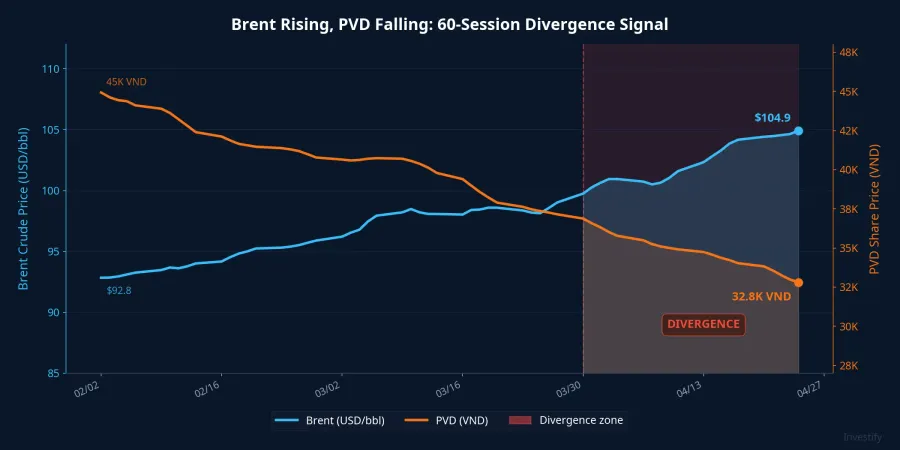

On April 24, two numbers appeared side by side on investors' dashboards: Brent crude closed above $107 per barrel — the highest since early April and the third time in six weeks it has broken the $105 mark — while PVD closed at VND 31,400, representing a 30.2% decline from the VND 45,000 peak reached on March 4. Anyone who heard the news that "oil is surging" and then opened their trading app to find PVD in the red would understandably be confused.

The short answer is that nothing is fundamentally wrong with PVD's business model. This is the expected behavior of a drilling services stock. The rest of the listed oil and gas group told the same story that week: PVS settled at VND 38,100, essentially flat; GAS fell 1.1% to VND 78,300; BSR dropped 4.4% to VND 25,000. The correlation between Brent and the Vietnamese oil and gas sector has turned negative over the past 21 sessions.

Reading this group of stocks correctly requires understanding three structural mechanisms that structurally decouple drilling equities from spot crude.

PVD Sells Rig Days, Not Oil

PVD operates a fleet of four jack-up rigs, one Tender Assisted Drilling (TAD) rig, and one land rig. Its revenue model is built on day-rates: customers — including PVEP, joint ventures with Zarubezhneft, and international contractors — pay a fee based on the number of days a rig is active, multiplied by a contracted rate. Day-rates for jack-up rigs currently run approximately $90,000–$100,000 per day. Critically, those rates are locked in when the contract is signed, not when crude oil trades on ICE Futures.

The consequence is straightforward: when Brent rises from $92 to $107 over six weeks, PVD's revenue for the quarter does not automatically follow. The contracts covering all four jack-ups have already filled out the 2025 schedule, with some extending into 2026–2027 at rates agreed months ago. Quarterly revenue figures reflect rig utilization — the ratio of actual working days to available days — and contracted day-rates, not the day-to-day movement of Brent crude.

Only contracts signed after this period of high oil prices can capture a higher day-rate. And that is precisely what the second mechanism addresses.

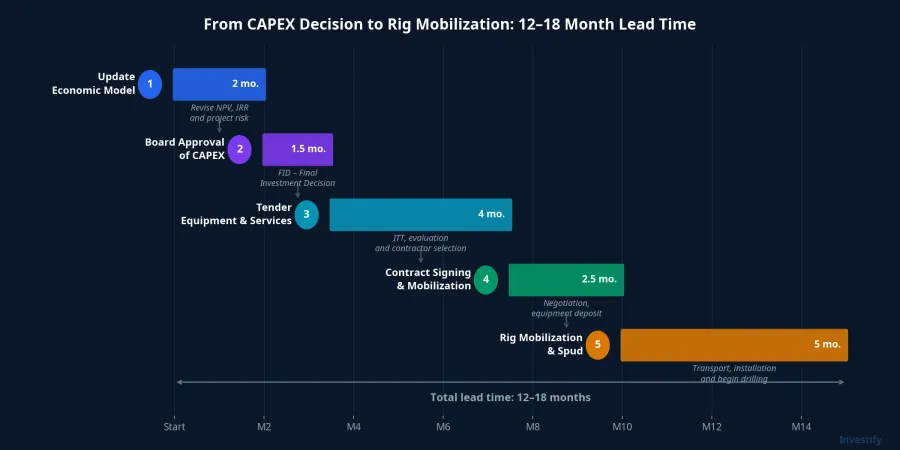

Drilling Contracts Lag by 12–18 Months

When an E&P company sees Brent at $107, it does not immediately pick up the phone and book a rig. The actual process involves several sequential steps: updating price assumptions in the project's economic model, submitting CAPEX for board approval (the Final Investment Decision, or FID), running a competitive tender or negotiating directly with a drilling contractor, signing a contract, scheduling rig mobilization, and finally spudding the well. For an average-sized project, this chain takes 12–18 months. For projects with government approval requirements, such as the Block B – O Mon development, it takes longer.

PVD's current contract backlog therefore reflects CAPEX decisions made in the 2024 cycle, not the oil price on April 27, 2026. PVN significantly expanded its CAPEX in 2025, and several major projects — Block B – O Mon, White Tiger, Dai Hung, Ca Voi Xanh — have entered active development. That is why rig utilization is expected to run around 86% in 2025 and approximately 98% in 2026. But those figures are locked in by existing contracts, not by this week's Brent price.

The same logic applies in reverse. When crude collapsed to around $60 during 2020–2021, regional day-rates fell to $60,000–$70,000 per day. The current level of approximately $95,000 per day reflects the investment cycle recovery that began in 2023–2024. It is the product of decisions made years ago, not of last week's oil market headlines.

Three Concurrent Pressures Unrelated to Brent

Higher oil prices are, in principle, positive for PVD's long-term earnings outlook. But the stock is currently under three simultaneous pressures, each causally independent from Brent crude.

Dilution from a large share issuance. A previously announced bonus share issuance will increase total shares outstanding, reducing EPS even if absolute profit improves. This is a purely technical factor that affects valuation multiples regardless of where oil trades.

Institutional portfolio rebalancing during elevated volatility. It is the volatility of Brent — not its direction — that prompts institutional funds to reduce exposure to oil and gas equities on a risk-adjusted basis. The result is weaker institutional bids even as crude continues to rise.

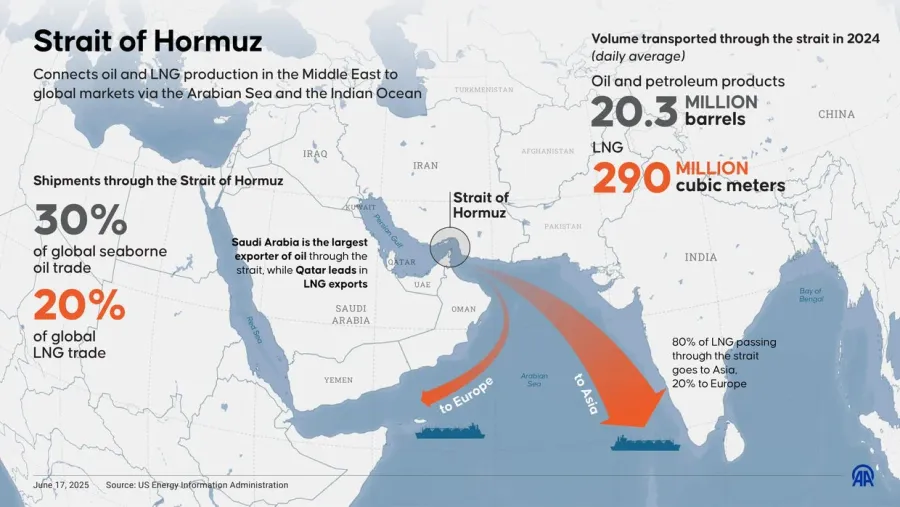

Hormuz adds uncertainty on both sides. This is the most nuanced of the three pressures. PVD does not operate rigs in the Persian Gulf — its regional contracts are concentrated in Vietnam, Malaysia, Indonesia, and Brunei. However, geopolitical anxiety over the Strait of Hormuz makes E&P companies globally more cautious about new CAPEX decisions, which slows the very contract cycle described above. The same event that pushes Brent higher (positive for long-term pricing power) simultaneously delays new contract activity (negative for near-term backlog).

Valuation: Where the Numbers Stand

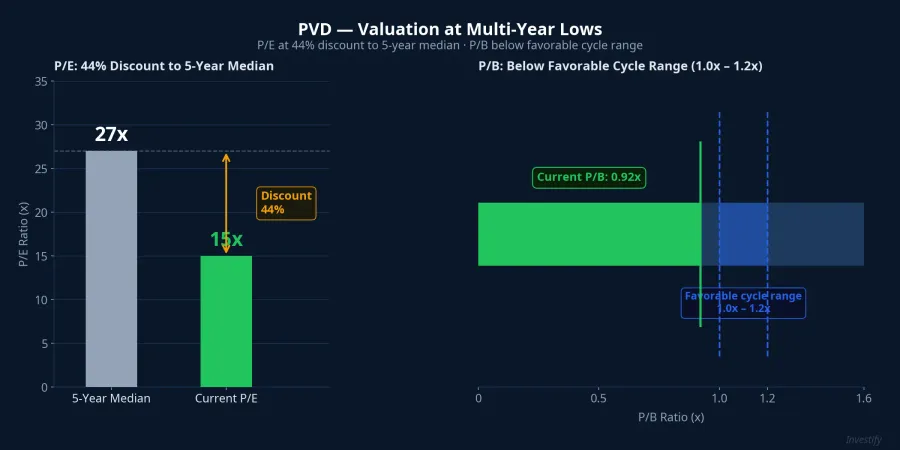

After a 30% drawdown, PVD trades at approximately 15x P/E — a meaningful discount to the 1–5 year median of around 27x, implying roughly a 44% discount. P/B sits at approximately 0.92x, below the 1.0x–1.2x range typically observed during favorable drilling cycles.

Earnings have grown faster than the share price, compressing the multiple. This pattern is not uncommon when share dilution and market sentiment headwinds coincide — both factors weigh on multiples without necessarily indicating deterioration in underlying business quality.

This is a reference framework, not a buy or sell recommendation. Given the day-rate model and contract lag dynamics analyzed above, the more important question is not "are the multiples cheap?" but "will the next CAPEX cycle convert into new backlog?"

What to Watch After Q1

Three forward indicators are more informative than daily Brent moves for tracking PVD's trajectory.

New contract signings in Q2–Q3 2026. This is the most direct signal of whether high oil prices are translating into incremental E&P spending. Watch for new PVEP drilling campaigns or the formalization of pending work scopes such as Phu Quoc POC. New contracts signed at day-rates above the 2024 level would be the first concrete signal that the current price environment is feeding into future revenue.

Quarterly rig utilization. The approximately 98% utilization expected for 2026 leaves almost no schedule gaps. Any quarter falling below 90% would hit revenue and earnings directly, irrespective of where Brent is trading.

Block B – O Mon and White Tiger project timelines. These two projects determine the volume of domestic drilling work available in 2026–2027 — essentially, PVD's workload once the existing backlog is consumed.

When investors see Brent break $107 and reach for oil and gas equities, the right question is not how oil compares to the stock price. The right question is: which contracts have been signed, at what day-rate, and how much of the rig schedule remains open. Today's day-rates reflect CAPEX decisions from 2023–2024. The day-rates for 2027 will reflect Brent 2026 — and that transmission chain has not yet had time to appear in current valuation multiples.

Q2 2026 earnings and any contract announcements this summer will be more meaningful data points than any single Brent session.