April 2026 rewrote the record books across Asian equity markets. KOSPI closed at 6,599.72 on April 27, up 20.9% in a single month. Five sessions earlier, on April 23, Nikkei 225 crossed 60,000 points for the first time in its history.Japan Times Over the same stretch, VN-Index sat at 1,853.29 — effectively sideways through the second half of the month.

These are not two markets rising in parallel by coincidence. The bigger picture reveals a single capital flow running through two different addresses, powered by three structural forces — none of which touches Vietnam.

HBM Converging in Seoul

High Bandwidth Memory (HBM) — the chip stacked directly beside GPU units in AI training servers — is the single most critical supply constraint in global AI infrastructure today. The world's two largest HBM providers, Samsung Electronics and SK Hynix, both trade on the Korea Exchange in Seoul. As US technology conglomerates poured capital into AI infrastructure buildouts, orders flowed directly into these two companies and lifted the broader KOSPI with them.

The scale of those orders showed up clearly in Q1/2026 earnings. SK Hynix reported quarterly revenue of KRW 52.2 trillion (+60% year-on-year) with operating profit of KRW 37.5 trillion and an operating margin of 72% — surpassing both TSMC and Micron.CNBC HBM capacity for the next three years is already sold out.KED Global Samsung Electronics reported preliminary Q1/2026 operating profit of KRW 57.2 trillion (~USD 37.9 billion), more than eight times the prior-year figure, driven mainly by HBM revenue tripling versus Q1/2025.KED Global

When three years of HBM capacity are already committed and operating margins run at 72%, stocks do not need fresh news catalysts to keep rising. On April 8 alone, Samsung gained approximately 7.3% and SK Hynix approximately 9.2% as capital rotated heavily into semiconductors.Yahoo Finance That is how a national index can surge 20.9% in a month without requiring geopolitical tailwinds or fiscal stimulus.

Japanese Semiconductor Equipment and the Weak Yen

Nikkei does not have HBM manufacturers, but it does have the critical upstream layer: semiconductor fabrication equipment and testing companies. Every new HBM fab built by Samsung or SK Hynix requires lithography systems from Tokyo Electron and testing equipment from Advantest. When SK Hynix announced plans to invest approximately KRW 19 trillion in new plant capacity, the resulting equipment orders flowed to Tokyo.CNBC When Nikkei touched 60,000 on April 23, the leading stocks were Lasertec, Fujikura, Advantest, and Ibiden — all semiconductor equipment and AI supply chain names.Bloomberg

A second amplifying force came from the exchange rate. USD/JPY held in the 158–159 range throughout April, closing at 159.78 on April 24. Toyota, Sony, Hitachi, and Tokyo Electron all collect most of their revenue in USD or EUR while paying wages and operating costs in yen. Every point of yen weakness versus the prior year translates directly into expanded operating margins across the exporter cohort — without changing unit volumes by a single item. These two forces combined explain why Nikkei moved in sync with KOSPI in April, but through an entirely different engine.

Hormuz Risk Cannot Penetrate a Tech-Heavy Index

Iran–US negotiations stalled again on April 27 and Brent crude rose approximately 2% in that session, yet KOSPI and Nikkei both closed near record highs. The reason is sector composition, not short-term market psychology.

Both South Korea and Japan are net energy importers, so a sustained oil price spike does, in theory, weigh on their trade balances. But KOSPI and Nikkei are heavily weighted toward technology, automobiles, and machinery — with negligible upstream energy exposure. When negotiations had already reduced the bulk of Hormuz risk earlier in April, input cost pressure lifted for the manufacturing-heavy components of both indices. The April 27 news created brief intraday volatility — it did not alter three years of pre-committed HBM orders or the USD/JPY level sitting at 159.

Why VN-Index Is Sitting This One Out

Over the same window, VN-Index moved sideways between 1,850 and 1,900. The explanation is structural, not a matter of bad luck.

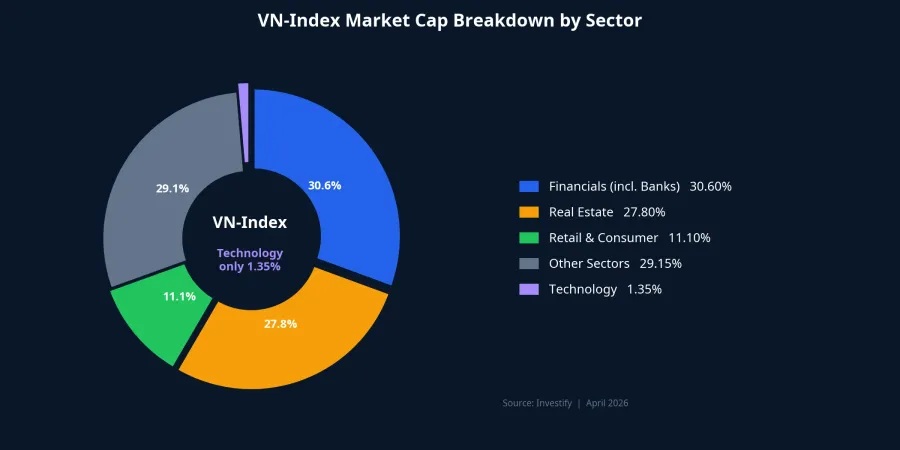

VN-Index is dominated by two traditional sectors: financials (including banks) at approximately 30.6% of market cap and real estate at approximately 27.8%. Technology accounts for roughly 1.35% — too small to move the index regardless of how fast the AI cycle accelerates. Within the more selective VN30 basket, technology and telecommunications reach 8.9%, comprising FPT, VNG, and CMG,The Shiv still well short of the 25–35% technology weighting in KOSPI or Nikkei. More critically, no Vietnamese company sits in the HBM supply chain or semiconductor equipment space. FPT operates in software services and chip design — not AI memory manufacturing. When SK Hynix's factory expansion order flows out, the capital goes to Seoul and Tokyo; it does not stop in Hanoi or Ho Chi Minh City.

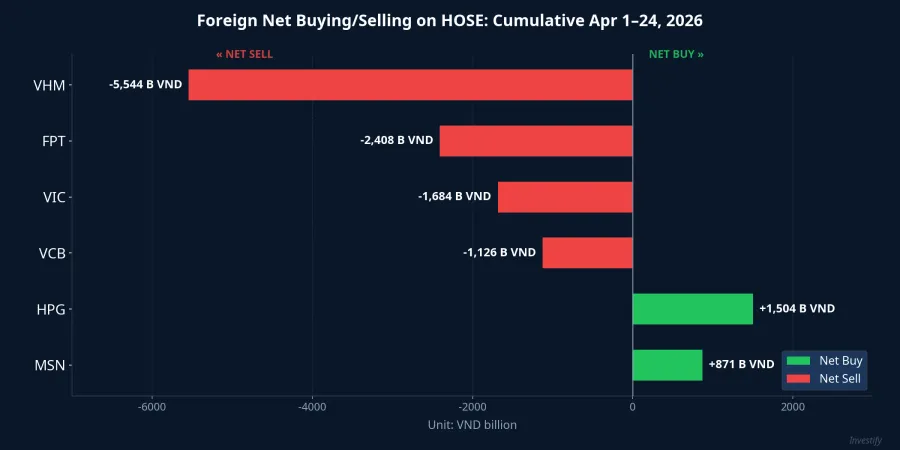

On the capital flow side, foreign investors pulled a net approximately VND 13,850 billion from HOSE between April 1 and April 24. The heaviest net sellers: VHM (-5,544 billion), FPT (-2,408 billion), VIC (-1,684 billion), VCB (-1,126 billion) — concentrated precisely in the index's largest-cap constituents. Net buyers shifted to materials and consumer names: HPG (+1,504 billion) and MSN (+871 billion). When large capital exits the very pillars of the index, there is no floor to launch a regional sympathy rally from.

Both forces point the same direction: a structural absence of AI-cycle beneficiaries in the index composition, compounded by active foreign distribution in the heaviest-weighted names. Even if KOSPI gains another 5% next month, VN-Index has no automatic transmission mechanism to follow.

What to Watch For

The KOSPI–Nikkei record run in April 2026 is the AI cycle running through the addresses already embedded in its supply chain. VN-Index's absence from that cycle is a structural fact — but three internal catalysts are worth monitoring to understand when the picture might shift.

FTSE Emerging Markets upgrade, expected to take effect in September 2026, is the clearest near-term trigger. When it does, passive funds will be required to buy Vietnamese equities at the new index weight — mandatory flows independent of sector composition. The cumulative net foreign selling figure on HOSE is the most relevant contrarian indicator to track weekly between now and then.

Q1/2026 bank earnings — representing 30.6% of the index's total market cap — are the nearest domestic catalyst. If net interest margins and profits hold up after the Big 4 raised deposit rates to 5.9%, selling pressure on VCB, BID, and CTG may ease. This is where VN-Index can generate upside momentum from within, without waiting for AI spillover effects.

Domestic semiconductor supply chain participation is the longer-horizon story — two to three years out. Any Vietnamese company that enters chip packaging, testing, or AI-focused chip design can establish a new leadership cluster in the index. This is not a near-term trade, but it is worth tracking when assessing the market's structural trajectory.

Global capital is not avoiding Vietnam — it simply does not have a local address to stop at in the current cycle. The catalysts for VN-Index are domestic: the FTSE upgrade and bank earnings season are two concrete milestones to watch over the next six months.