On 26 April 2026, BIDV announced the second tranche of its public bond offering: nearly 37 million bonds totalling approximately VND 3,698 billion at par value.MarketTimes Each bond has a face value of VND 100,000, meaning retail investors can participate with as little as VND 10 million. The full three-tranche programme totals VND 9,000 billion across 90 million bonds. Registration opens 28 April and closes 20 May 2026 at BIDV branches nationwide.

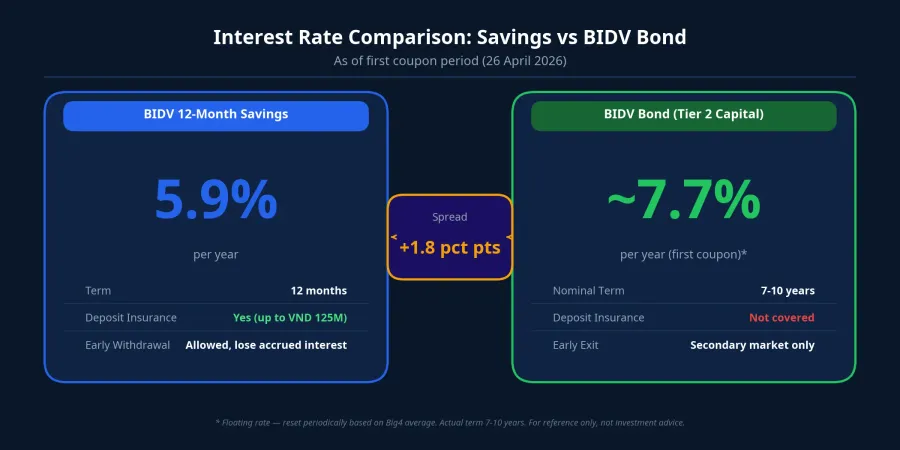

This is one of the few fixed-income products from one of Vietnam's largest state-owned banks made accessible to ordinary investors. The initial yield sits at approximately 7.7% per annum — roughly 1.8 percentage points above BIDV's own 12-month savings rate. But before deciding whether this product belongs in your portfolio, the more important question is not "how much does it pay?" It is: "what do you give up to earn that extra 1.8 points?"

A Floating Rate, Not a Fixed One

Here is a simple way to think about it: a 12-month savings deposit at BIDV currently pays 5.9% per annum, fixed for the entire term.MarketTimes You know exactly what you will receive at maturity. No monitoring required.

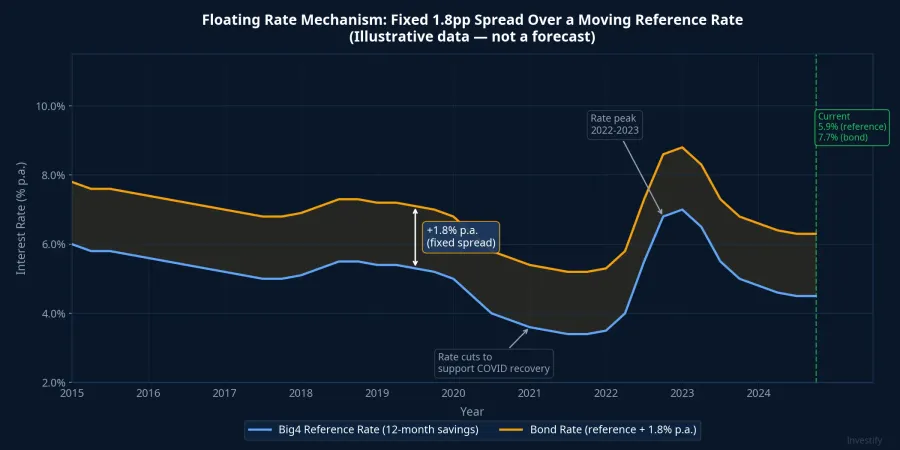

BIDV's bond works differently. Its coupon is floating, reset periodically using a formula: the average 12-month savings rate for individual customers across the four state-owned banks (BIDV, Vietcombank, Vietinbank, Agribank) plus a fixed margin of 1.8% or 1.9% per annum depending on whether the tenor is 7, 8, or 10 years. Coupons are paid every six months and do not compound. With the Big4 reference rate currently at 5.9%, the opening coupon lands around 7.7% per annum.

The 1.8 percentage-point margin is fixed; the base it sits on is not. When the savings rate environment rises, bond yield rises with it — partial protection against prolonged inflation. When rates fall, the bond yield falls too. If Big4 savings rates drift down to 4.5% over the next few years, the bond's yield would drop to roughly 6.3%. Today's 7.7% is a starting point, not a guaranteed return for the full 7 to 10 years.

Capital Protection: the Gap Between "Insured" and "Not Insured"

This is the single biggest structural difference between the two products — and the one most easily overlooked when attention is fixed on the yield number.

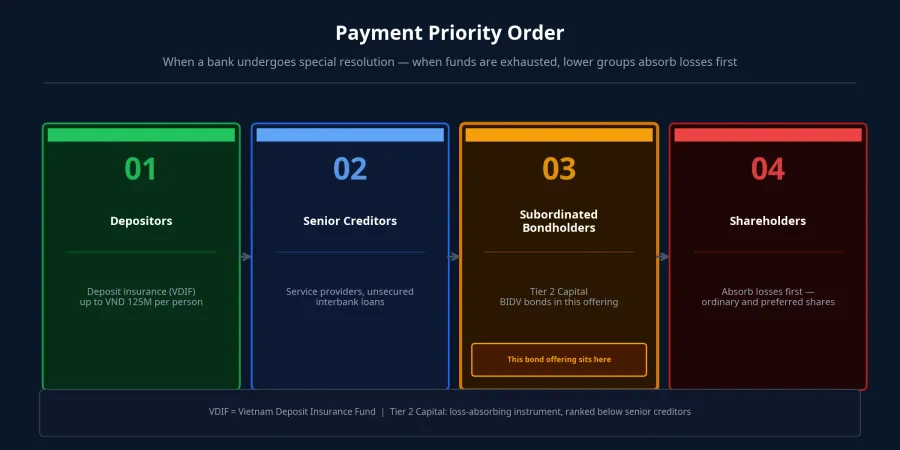

Savings deposits at BIDV are protected by the Vietnam Deposit Insurance Fund (VDIF) up to VND 125 million per person per institution, covering both principal and accrued interest, under Decision 32/2021/QD-TTg effective December 2021.Government Portal This threshold covers approximately 91% of all individual depositors in the Vietnamese banking system.VDIF

BIDV's bonds carry no deposit insurance. More importantly, the offering document classifies them as unsecured, direct, and subordinated obligations of BIDV.MarketTimes "Subordinated" has a precise legal meaning: in the event of bank insolvency or special resolution, subordinated bondholders rank after depositors, after senior creditors, and only ahead of shareholders in the repayment queue. The bonds exist specifically to provide Tier 2 Capital — and that structure is exactly why bondholders bear more risk than depositors and receive a higher margin in return.

To be fair to BIDV: the bank holds approximately VND 3.26 quadrillion in total assets as of end-2025, pre-tax standalone profit of approximately VND 35,509 billion, and a non-performing loan ratio of approximately 1.26%.MarketTimes The probability of insolvency for a state-owned bank of this size and asset quality is very low under current market conditions. But "very low" is not "zero" — and that 1.8 percentage-point spread is the market's price for the gap between those two risk levels.

Liquidity: the Right to Withdraw Is Not Automatic

A 12-month savings deposit at BIDV allows early termination at any time. The trade-off is that early-exit interest falls to the demand-deposit rate, roughly 0.2–0.5% per annum. You lose accumulated interest, but you receive your principal back on the same business day. That is near-perfect liquidity.

BIDV's bonds have a nominal term of 7, 8, or 10 years. To exit before maturity, you must sell on the secondary market. The corporate bond trading platform at HNX has been operational since 2023, but liquidity varies widely across individual bond series.MarketTimes Sale price depends on the prevailing interest rate environment at the time you want to exit: if market rates have risen since you bought, bond prices will have fallen and you may sell below par. Bid-ask spreads are also wider than for listed equities.

There is also an embedded call option worth noting: subordinated bank bonds typically give the issuer the right to redeem early after five years. This is BIDV's right, not the investor's. If market rates fall sharply, BIDV may choose to call the bonds and refinance cheaper — leaving investors to reinvest at lower rates. Conversely, if rates rise, BIDV keeps the bonds outstanding and investors remain locked in at the original 1.8% margin over a now-lower base.

Which Product Belongs in Which Part of Your Portfolio

Think of it this way: these two products are not better-or-worse versions of the same thing. They serve two distinct needs within the same portfolio.

12-month savings makes sense when you need emergency liquidity, are building a safety fund, or have under VND 125 million that you want fully insured. Trading away 1.8 percentage points to retain the ability to exit at any time and the full protection of deposit insurance is a rational decision for the safe-capital layer of your portfolio.

BIDV bonds are a better fit if you have an established financial base, want to diversify beyond equities, can genuinely commit capital for five or more years, and understand your position in the subordination stack. For a portfolio of sufficient scale, allocating a portion to Tier 1 bank bonds can raise the blended yield without significantly altering overall risk — provided you accept secondary-market price volatility and the reinvestment risk that comes with the issuer's call option.

The right question is not "which one is better?" It is: what does each part of your portfolio need right now, and how long can you genuinely afford not to touch this money?

The Real Lesson This Offering Provides

The number of individual brokerage accounts in Vietnam reached approximately 11.9 million by end-2025, yet the vast majority of those investors have never purchased a corporate bond.MarketTimes This means a large share of Vietnam's retail investment community has never read a bond prospectus, never distinguished subordinated debt from senior debt, and never had to evaluate secondary-market liquidity.

This offering — with its VND 100,000 face value and registration window from 28 April to 20 May 2026 at BIDV branches — is a genuine opportunity to experience corporate bonds for the first time through a high-quality issuer. The most valuable lesson is not the 7.7% per annum yield. It is the ability to read and understand three phrases in a bond disclosure: "unsecured — direct obligation — subordinated." Those three terms describe precisely where you stand in the protection queue, and that skill will serve you in every fixed-income decision you make going forward.

The variable to watch in coming periods: whether Big4 savings rates continue to adjust — that is the direct determinant of the actual yield bondholders receive in coupons beyond the first payment.