On 25 April, Vietnam's digital banking sector got two concrete valuation benchmarks announced on the same day. At MSB's annual general meeting, CEO Nguyễn Hoàng Linh said the bank would shelve its plan to divest TNEX Finance, instead targeting a USD 1-2 billion valuation for the subsidiary within five to seven years.VietnamFinance On the same day, Indonesia's Kredivo Group announced it had completed a 100% acquisition of the Timo platform, rebranding the Vietnamese lending arm as Timo Credit and committing another USD 15 million over three years.CafeBiz

Two moves, in opposite directions on the same day, hand retail investors their first set of concrete numbers for reading Vietnam's digital banking landscape.

Who holds the capital: domestic build versus foreign buyout

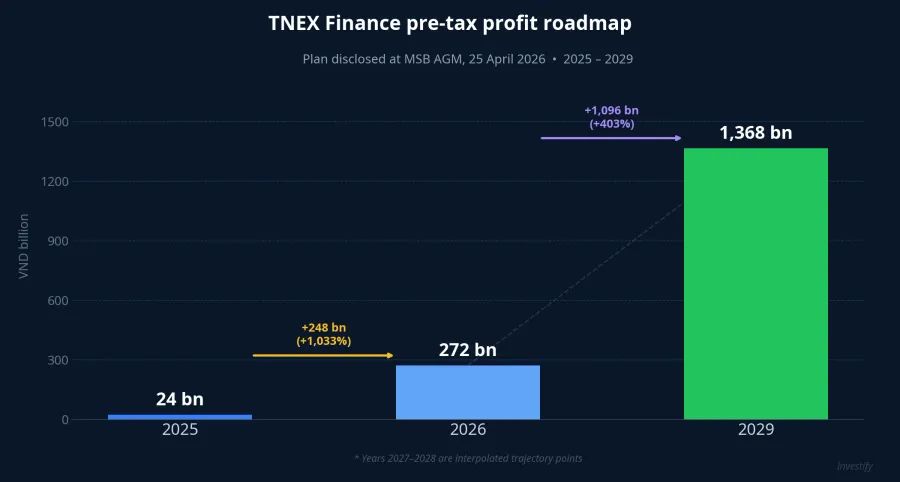

MSB chose to stay with TNEX Finance after years of failing to find a divestment partner. According to the AGM disclosure, the bank worked with McKinsey to reposition TNEX as a full-service finance company rather than a pure consumer-credit lender. Pre-tax profit is mapped to climb from VND 24 billion in 2025 to VND 272 billion in 2026 and VND 1,368 billion in 2029; total assets are projected from VND 8,578 billion in 2026 to VND 22,038 billion in 2029, with the loan book moving from VND 8,273 billion to VND 19,968 billion.Nhịp sống kinh doanh

On the other side, Timo — the pioneering Vietnamese digital bank launched in 2014 — passes fully into Kredivo Group, Indonesia's largest BNPL fintech. Behind Kredivo sits a Series D round of about USD 270 million led by Mizuho Bank in 2023, with co-investors Square Peg, Jungle Ventures, Naver Financial, GMO, and Openspace.TechCrunch Kredivo's cumulative equity raise stands near USD 400 million, supplemented by close to USD 1 billion in committed debt facilities to scale its loan book.

Phoenix Holdings and VinaCapital — Timo's previous strategic shareholders — retain a meaningful minority stake in Kredivo Vietnam. Henry Nguyễn (Chairman of Phoenix Holdings), Don Lam (CEO of VinaCapital), and Brook Taylor (CEO of VinaCapital's asset management arm) join the Kredivo Vietnam board.

Who holds the customers and the ecosystem

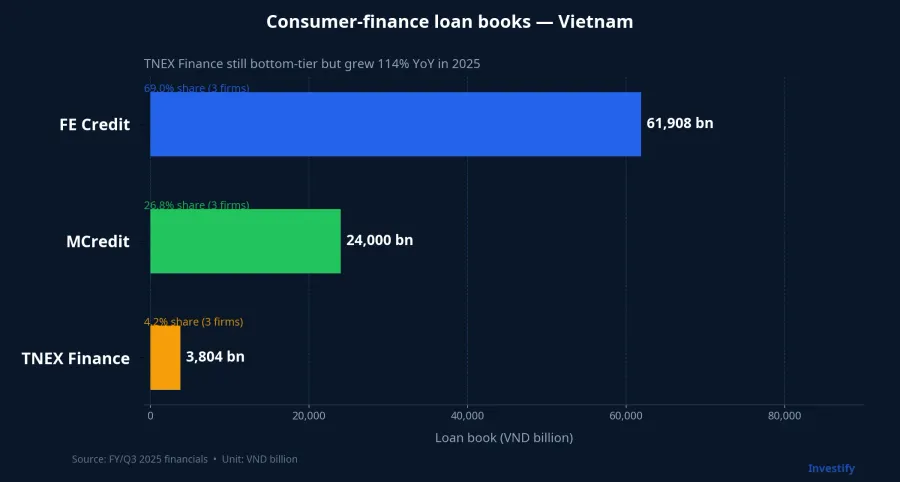

Looking at the numbers, TNEX Finance is small compared with the leading pack. In 2025, total assets stood at VND 7,016 billion, the loan book at VND 3,804 billion (up 114% year-on-year), revenue at VND 698 billion, and pre-tax profit at VND 24 billion, with NPLs improving from 10.3% to 9.1%.Bao Moi Within the consumer-finance peer set, TNEX still sits at the bottom but is the fastest grower.

FE Credit (VPB) had a Q3/2025 loan book of about VND 61,908 billion with a 16.5% NPL ratio; HD Saison (HDB) reported VND 709 billion in first-half 2025 profit with a 7.36% NPL; MCredit (MBB) carries a loan book around VND 24,000 billion. Against that scale, TNEX's 2029 profit target of VND 1,368 billion still sits a long way from where FE Credit operates today, but its 114% loan book growth in 2025 shows the runway is forming.

TNEX's edge is the MSB ecosystem behind it. The bank has more than eight million customers and is expanding into securities, asset management, and insurance, with TNEX positioned inside that financial-group structure. Cross-selling and customer-data sharing give it a leverage point that standalone competitors like Home Credit or Lotte Finance do not have.

Timo took the opposite path. After a 2015-2019 partnership with VPBank, the digital bank moved to BVBank in 2020 and reached close to 700,000 customers by end-2023, approaching the one-million mark in 2024. BVBank credited 92% of new customer acquisition through digital channels to the Timo partnership. But Timo struggled to develop a standalone consumer-lending business — exactly the gap Kredivo plans to plug with its Indonesian credit-scoring engine, under the new Timo Credit brand.

Who carries operating risk, who books the valuation upside

The notable feature of MSB's plan is the cost structure ahead. The bank will absorb five to seven more years of build-out costs: provisioning for the TNEX loan book is set to roughly quintuple from 2026 to 2029, alongside technology investment and the credit risk of a portfolio whose NPL ratio still sits at 9.1%. In return, if TNEX hits the trillion-dong profit milestone in 2029 and reaches the targeted valuation, MSB has room to book a one-off gain by selling a stake to a strategic partner — the same playbook FE Credit ran when SMBC bought 49% at a USD 1.4 billion implied valuation in 2021.Tuổi Trẻ

Kredivo pays today to receive customers and infrastructure that already exist, skipping a five-year build phase. The valuation upside is already locked in via the Series D round, which prices both the Indonesian core and the freshly acquired Vietnamese assets. Behind Kredivo sits Mizuho Financial Group — the same Japanese mega-banking peer group as SMBC, which sits behind FE Credit. The signal is clear: Japanese institutions are systematically building exposure to Southeast Asian consumer finance.

Neither approach is "more correct" than the other. Each model serves a different player: domestic banks want to keep weight inside Vietnam's home-grown digital banking economy, while regional fintechs want to scale credit technology into ASEAN's fastest-growing market.

What it means for retail investors

MSB shares enter Q1/2026 with solid fundamentals: pre-tax profit of VND 1,890 billion (up nearly 16% year-on-year), consolidated assets of VND 412,900 billion, and customer deposits of VND 193.8 trillion (+18.93%).VietnamBiz Full-year guidance is VND 8,000 billion in pre-tax profit (+13%) and a charter-capital increase from VND 31.2 trillion to VND 37.44 trillion. The TNEX story is a long-dated valuation layer stacked on top, and is not yet priced in given that TNEX still represents under 2% of MSB's consolidated assets.

The analytical frame for MSB shares right now has two layers. The first is valuing the parent bank on the usual ratios: P/B, ROE, NIM, and credit room. The second is the long-dated TNEX expectation, which only flows into the price if TNEX hits its interim milestones in 2026-2027 (VND 272 billion and beyond) and a strategic-partner approach surfaces. Three concrete signposts to watch over the next 12-18 months: whether TNEX exceeds VND 272 billion in 2026, whether the NPL ratio drops below 8%, and whether any strategic partner announcement materializes.

The broader picture: international capital is treating Vietnamese digital banking and consumer finance as an asset class worth participating in. Mizuho is behind Kredivo, SMBC is behind FE Credit, and Korean and Japanese banks continue probing HD Saison and MCredit. Retail investors cannot directly access unlisted fintechs, but they can do so indirectly through listed parent banks that house separated consumer-finance subsidiaries: VPB, HDB, MBB, MSB. Each ticker carries a different risk structure and valuation path, with the choice depending on appetite.

The open question for the next five years is not "what is Vietnamese digital banking worth" but "who will hold that value." With TNEX, MSB is betting fully on the domestic answer. With Timo, the answer has moved to Jakarta. Q3/2026 financials for both TNEX and MSB will be the first checkpoint to test whether the profit roadmap is tracking the plan.