April 2026 placed two facts side by side that make life difficult for any retail investor trying to read the Vietnamese real estate market. The Hai Phong Department of Construction confirmed that Vingroup's Vũ Yên island project is qualified to raise up to VND 36,000 billion on a 47.2-hectare plot with total investment exceeding VND 44,000 billion — 32 buildings of 8 to 30 floors and roughly 15,000 apartments.VnExpress Within the same window, owners of resale apartments on Hanoi's outskirts have been cutting prices by VND 500–700 million on larger units and still struggling to find buyers.VnExpress

The two pictures are not contradictory. They are two sides of the same capital-restructuring process now reshaping who gets to stay in the Vietnamese real estate industry. The bridge between them lies in elevated home loan rates and the State Bank of Vietnam's tightened 2026 credit room.

Primary market: capital still flows to the leaders

The decision to clear Vũ Yên for fundraising does not stand alone. Vingroup's annual general meeting on April 22 set a 2026 after-tax profit target of VND 35,000 billion — three times the 2025 result; Vinhomes set a target of VND 60,000 billion, the highest ever for a listed company in Vietnam.Vietstock That ambitious budget rests on launches and revenue recognition from mega-projects spanning tens of thousands of units, of which Vũ Yên is one. CafeF reports the auction-winning project is expected to deliver 32 buildings of 8 to 30 floors and around 15,000 apartments.CafeF

In the same Q1 2026, 1,563 new real estate companies were registered, up 54.3% year-on-year.Cafeland That is a signal that fresh capital is moving into the industry — but mostly toward firms with clean land banks, full legal documentation and diversified funding channels. With credit room being tightened, banks have all the more reason to prioritise lending to projects with proper paperwork and clear collateral — exactly the profile of a mega-project like Vũ Yên.

Secondary market: buyer affordability has snapped

The picture on the resale side tells the opposite story. Also in Q1 2026, 726 real estate firms completed dissolution — double the 363 recorded in the same quarter of 2025.VietnamBiz The bulk of those leaving are small firms dependent on short-term debt, with no fresh land bank, who lose their edge when interest rates stay elevated.

The clearest break has come from the demand side. As of early April, one apartment owner on Hanoi's outskirts agreed to drop another VND 4 million per square metre, bringing total losses to VND 800 million when the buyer's premium is included. Old collective-housing units and large-area apartments (>100 m²) have been hit hardest because their absolute prices exceed what mainstream buyers can afford under the current borrowing environment.VnExpress

Home loan rates: the bridge between the two pictures

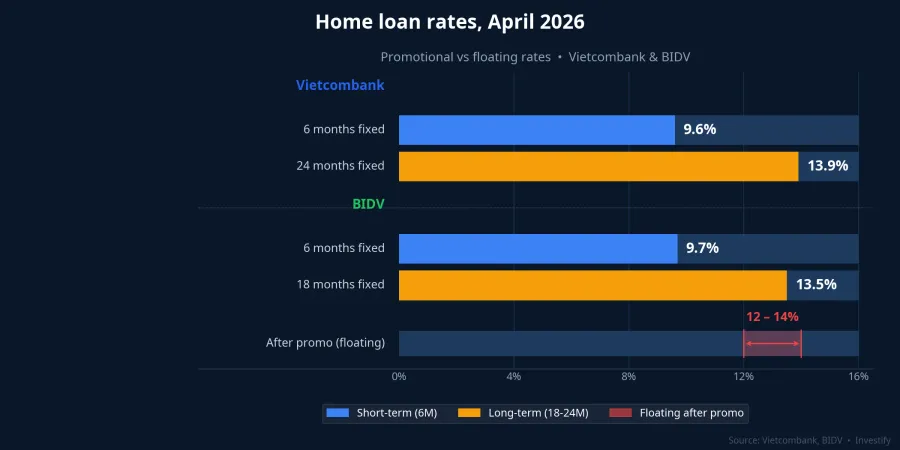

April 2026 home loan rates sit notably above where they were a year ago. Vietcombank applies 9.6%/year fixed for 6 months and 13.9%/year fixed for 24 months; BIDV lists at minimum 9.7%/year for the first 6 months and 13.5%/year for the first 18 months.VPBank After the promotional period, floating rates approach 12–14%/year depending on bank and tenor.VnExpress

Resale buyers absorb this cost in full. They are the borrower of last resort, with no developer subsidy. Primary buyers in major projects, by contrast, can borrow at promotional rates because the developer absorbs the spread for the first 1 to 2 years, pushing the break-even point of the home-purchase math into much more comfortable territory. That is why primary-market liquidity has held up in the very same rate environment that has frozen the resale market.

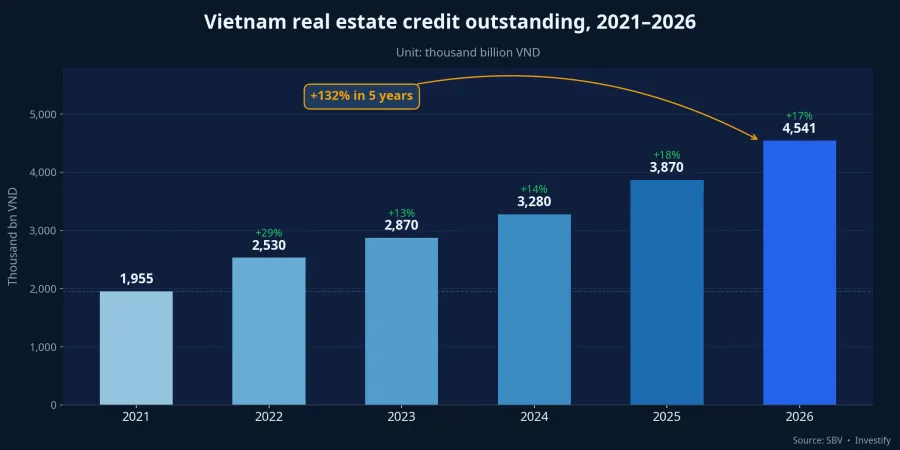

The supply side of money is also bifurcated. Real estate credit outstanding has reached VND 4.541 quadrillion, up 132% over 2021–2025 and 2.4 times the growth rate of the industrial sector.VnBusiness

But starting in 2026, the State Bank of Vietnam requires that real estate credit growth at each institution not exceed the bank's overall credit growth; breaching this rule means losing room.Bao Dau Tu Under that constraint, banks prioritise disbursement to projects with clean legal status, clear collateral and reputable developers — which is exactly where Vũ Yên sits. The same elevated rate environment, combined with developer interest subsidies and bank room channelled to documented projects, has produced a widening gap between primary and secondary markets.

Third signal: the average size of firms is shifting

Subtracting 726 dissolutions from 1,563 new registrations gives a net of 837 additional firms in Q1, but this is not uniform growth. Firms that dissolved were mostly small entities with low charter capital and no clean land bank. Newly registered firms lean toward those with substantial capital, financial partners or links to leading developers. The average size of the industry is rising — not the number of players.

Pressure is also building on the bond side. Some developers are having to top up collateral on bond tranches as their share prices fall sharply, as Novaland has had to do for its Aqua City project.Nhip Song Kinh Doanh That signals the bifurcation runs not just between leaders and exiters, but also through the middle — large but highly leveraged firms still have to post additional assets to retain bondholder confidence.

Implications for retail investors

Two different pictures suggest three different answers, depending on where you sit in the process.

For owner-occupier buyers, primary-market product from a developer with full legal status and a 1- to 2-year interest subsidy carries a clear financial edge over buying resale at the same price band. A high equity ratio (≥ 40–50%) is a necessary buffer when post-promotion rates can hit 13–14%/year and there is no signal of a near-term cooldown.

For those holding resale property at price levels above what mainstream buyers can afford (large apartments, old collective housing on the outskirts), liquidity shows no sign of recovery in the current rate environment. The reasonable choice is to accept a longer holding period than expected and to plan cash flows that do not depend on a quick exit.

For financial investors looking at the sector through equities, valuations of leading firms with strong balance sheets, clean land banks and proven sales execution have decoupled from the rest of the industry. Firms heavily reliant on near-maturity bonds or short-term borrowing are the segment now having to post additional assets just to stay in the market — equity dilution risk and liquidity pressure must be priced in before entering.

Signals to watch in Q2 2026

Three indicators will answer whether the bifurcation deepens or starts to converge.

First, absorption rates at the major primary projects launched in Q2 — if Vinhomes and other leading developers maintain revenue-recognition pace, the "capital flows to the leaders" thesis stays intact. Second, home loan rates at the Big 4 banks: only when floating rates leave the 12–14%/year range will resale buyers have a chance to re-enter. Third, the dissolution count in Q2 2026 versus the 726 firms in Q1 — if the number stays high or rises, the firm-size restructuring process is mid-cycle, not finished.

If all three indicators continue along their current trajectory, the primary–secondary divergence will widen, not converge. That is the scenario to factor in when deciding whether to buy, hold or sell real estate over the next six months.