On the morning of 25 April 2026, Techcombank's annual general meeting approved two figures worth reading together. Charter capital rises by VND 42,876bn to VND 113,738bn — the highest in Vietnam's banking system. At the same meeting, Chairman Hồ Hùng Anh reiterated the bank's $20 billion market cap target, the goal he originally set for end-2025 but did not reach.Báo Mới This time there was no new deadline. The quoted line was short: a $20B valuation "is only a matter of time."

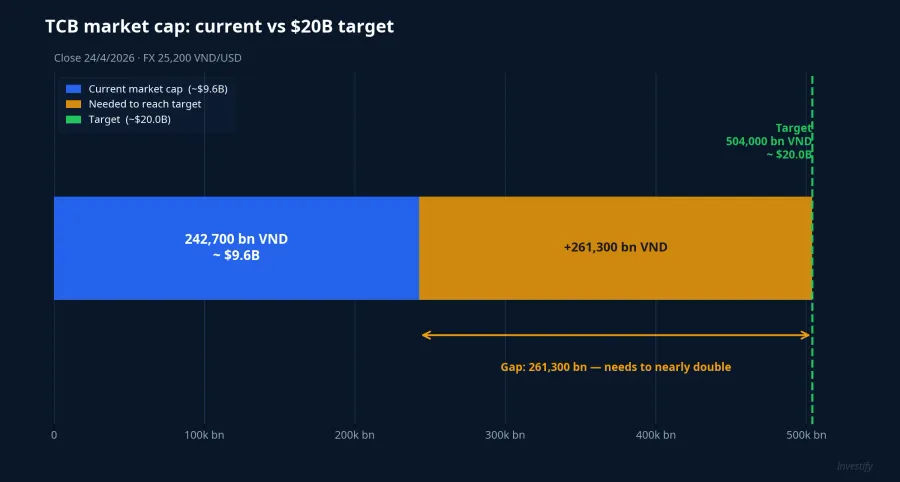

Look at the numbers and the gap is wider than it sounds. At the close on 24 April, TCB stood at VND 34,250, with a market cap of about VND 242,700bn. Converted at the FX rate of 25,200 VND/USD, that works out to roughly $9.6 billion. To reach $20B (~VND 504,000bn), the share price would need to almost double from current levels — a full re-rating cycle, not a session-by-session move.

VND 113,738bn charter capital: above Big4, but not by as much as it looks

Shareholders approved a 60% bonus share issuance funded from equity, lifting charter capital to VND 113,738bn.CafeF The bank also declared a 7% cash dividend — VND 700 per share, total payout close to VND 4,960bn.

To put VND 113,738bn in context, place it alongside the Big4. Vietcombank currently sits at VND 83,557bn and is filing a plan to raise it to around VND 94,000bn — close to the VND 100,000bn mark if its private placement completes.24h Money BIDV is at VND 70,213bn with a maximum plan that could push it above VND 100,000bn.Saigon Times

Within the 2026 window, TCB takes the lead in charter capital. But if both VCB and BID execute their plans, the gap among the three narrows materially — not as wide as the absolute numbers suggest. The "largest in the system" position depends on execution speed on both sides. The Big4 typically face procedural constraints around private placements and state ownership — a layer of uncertainty TCB does not have to navigate.

A "low risk, high return" strategy and the VND 5,000bn annual price tag

The most striking part of the AGM was not the charter capital figure but the way TCB acknowledged the opportunity cost of its conservative posture. The bank holds a high-quality liquid asset stack and a capital buffer above regulatory thresholds. It accepts an estimated opportunity cost of roughly VND 5,000bn per year — the profit it could have booked had this capital been redirected into higher-yielding lending or investment.Dân Việt

In return, TCB gets three buffers. Equity is large and the capital adequacy ratio runs above the regulatory minimum, reducing reliance on short-term wholesale funding. The high-quality liquid asset book can be converted to cash quickly under Basel III standards. The liquidity cushion is thick, with a meaningful share coming from CASA and low-cost funding — together helping the bank meet the full Basel III framework.

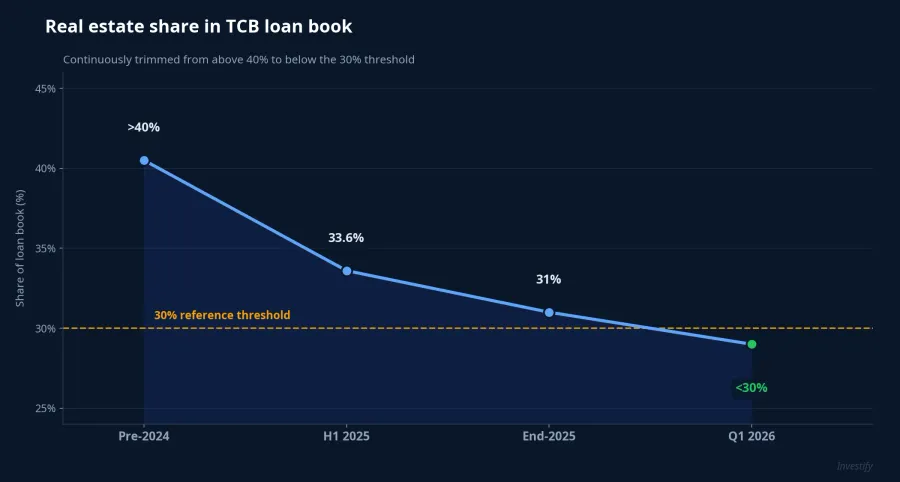

The share of real estate in the loan book has been trimmed step by step: from above 40% before 2024, to 33.6% in H1 2025, to 31% at year-end 2025, and to below 30% in Q1 2026. Management said recovery rates on real estate credit — including loans that had been reclassified as non-performing — reach 100% within 2–3 years, thanks to financing only projects with completed legal status and clear cash flow. This is a TCB-internal disclosure and should be read as a signal about asset quality, not an industry standard.

Two profit scenarios for 2026 and the framing question

The two pre-tax profit scenarios presented at the AGM fall in the VND 35,000–37,500bn range, depending on whether the macro backdrop is favorable or cautious. Approved credit growth is around 12%; NIM stays stable; service income keeps expanding. Q1 2026 reached over 24% of the annual plan — a pace consistent with the scenarios filed.

That is a meaningful profit zone, but it has to be read against the VND 5,000bn opportunity cost — the profit TCB is actively choosing not to earn. For a bank guiding to VND 35,000–37,500bn pre-tax, the capital "sleeping" inside the safety buffer is equivalent to roughly 13–14% of potential profit. That ratio is large enough for shareholders to question whether the trade is fair.

Can a valuation premium make up for the VND 5,000bn?

TCB's price-to-book ratio currently sits near 1.35. To reach $20B while equity continues to grow with retained earnings, the bank needs a meaningful valuation premium versus the current sector average. That is the implicit message when Chairman Hùng Anh references valuation levels in Thailand and Indonesia — markets where leading private banks typically trade at P/B of 2–3.

The core question for individual shareholders is not "will it hit $20B" but whether a conservative strategy that trades VND 5,000bn of annual profit for safety margin is enough to convince the market to assign a higher valuation that compensates for the foregone profit. The argument cuts both ways. On one side: markets price private banks primarily on asset quality and through-the-cycle earnings stability — areas TCB is reinforcing. On the other: Vietnam's market still tends to value banks on absolute profit growth, which means the "profit not earned" gets penalized faster than the safety margin gets rewarded.

The picture and signals to watch

This is a long-horizon holding decision, not a session-by-session story. A blue-chip bank stock with a conservative strategy and a steady distribution history typically sits as a core sleeve of a portfolio, with weight calibrated to each investor's risk appetite.

Three signals to watch over the next 6–12 months:

- Relative P/B after the 60% bonus share issuance: once the 1.7 billion new shares hit accounts, the P/B ratio will adjust automatically. How quickly the market re-rates the gap versus VCB, ACB, and MBB is a key tell on whether the safety premium is actually being paid.

- VCB and BID capital raise progress: if the Big4 complete their private placements during 2026, TCB's "highest charter capital in the system" position becomes largely symbolic. The real gap then sits in asset quality and return on capital.

- Q2 2026 NIM and CASA: the "low risk, high return" strategy only holds together if CASA and net interest margin defend current levels through a volatile rate environment. If both metrics weaken, the VND 5,000bn opportunity cost becomes a real cost that is hard to defend.

Of the three banks racing toward the VND 100,000bn charter capital mark, each represents a different valuation strategy: VCB on scale and state backing, BID on credit growth that follows FDI flows, TCB on a safety premium. Q2 2026 will be the first window where the market has the data to grade all three.