On the morning of 23 April 2026, the AGM of Saigon Beer–Alcohol–Beverage Corporation (SAB) approved the final 30% face-value cash dividend for 2025, equivalent to roughly VND 3,846 billion paid out to shareholders.Dan Tri Combined with the 20% advance (VND 2,000 per share) settled on 12 February 2026, total cash dividends for 2025 land at VND 5,000 per share — the second consecutive year Sabeco maintains a 50% face-value payout ratio.Vietstock

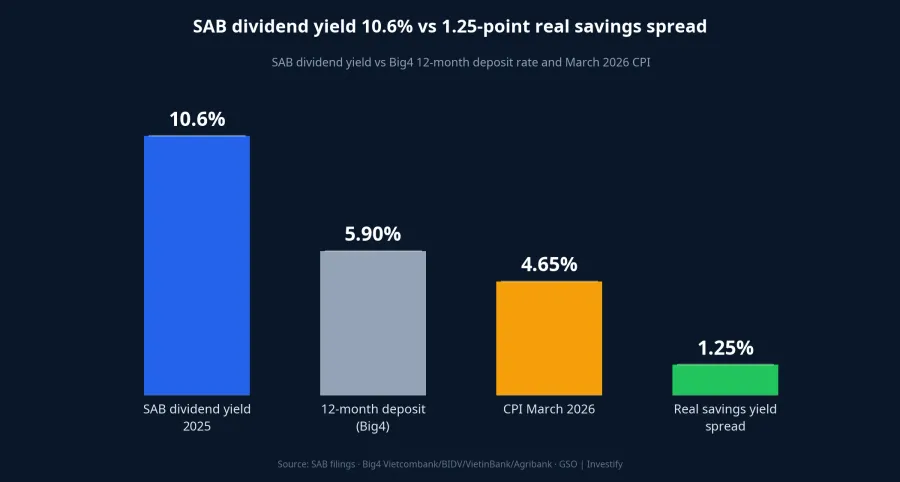

At the 24/4 closing price of VND 47,000 per share (market cap roughly VND 60,300 billion), SAB's 2025 dividend yield works out to about 10.64%. After a 5% personal income tax on cash dividends, retail investors take home around 10.1% per year. That number doesn't say SAB is a buy at today's price. It's a reminder that cash dividends — the steady-income channel that many Vietnamese retail investors overlook while chasing capital gains — just opened a natural window for re-evaluation.

Why now: the real savings yield spread is down to 1.25 points

12-month deposit rates at the Big4 banks now sit around 5.9% per year; ACB pays 5.2%, MB 4.85%. March 2026 CPI hit 4.65%, the highest in five years according to the General Statistics Office. The real yield spread for ordinary savers has shrunk to about 1.25 percentage points — the thinnest in six years.

In that environment, a cash-dividend portfolio yielding 6–10% with a steady payout history offers a meaningful income advantage over deposits. But equities aren't deposits. Principal swings with the market, companies can cut dividends in a bad year, and a high yield sometimes signals risk rather than opportunity. That's why you need a framework before buying — not just sorting the "yield" column on a stock screener.

Four criteria for picking cash-dividend stocks

Criterion 1: After-tax yield of at least 5% per year. This is the threshold for a dividend stock to compete with 12-month deposits. After the 5% dividend tax, the nominal yield needs to be roughly 5.3% per year to deliver 5% net — on par with the Big4. Below that, you're accepting equity volatility without earning a premium over deposit insurance.

Criterion 2: At least five consecutive years of cash dividends. One year of high dividends means nothing. Five consecutive years signals a stable revenue base and a board genuinely committed to cash distribution. SAB paid cash dividends every year from 2020 to 2025 at 35–50% of face value. VEA, BMP, MCH and ACV also belong to the group that has sustained cash dividends across cycles.

Criterion 3: Sustained positive free cash flow. Sustainable dividends must come from cash the company generates after maintenance capex — not from new debt or asset sales. A simple read: open the cash-flow statement, take operating cash flow minus capex to get free cash flow. The minimum bar: positive in at least three of the last five years.

Criterion 4: Payout ratio under 80% of net income. The dividend-to-net-income ratio tells you how much room the company has to maintain payouts when profit dips for a year. A 95–100% payout means a single bad quarter forces a cut next year. A 50–70% payout absorbs a weak cycle without breaking the commitment to shareholders.

This is the criterion to read most carefully for SAB itself. 2025 net income came in at VND 4,573 billion,Dan Tri while total dividends of VND 5,000 × 1,282 million shares outstanding equal about VND 6,410 billion. That puts the payout ratio near 140%, well above the criterion 4 threshold. So why can SAB still pay it? Because cash and deposits accumulated over years on the balance sheet allow distributions in excess of current-year profit. That cushion isn't infinite — investors should read the balance sheet alongside, to estimate how long the cash buffer can sustain dividends if earnings stay weak.

Applying the framework to high-yield Vietnamese stocks

The list below is for illustration only, not a buy recommendation. Every investor should read the financials and assess sector-specific risks before deciding.

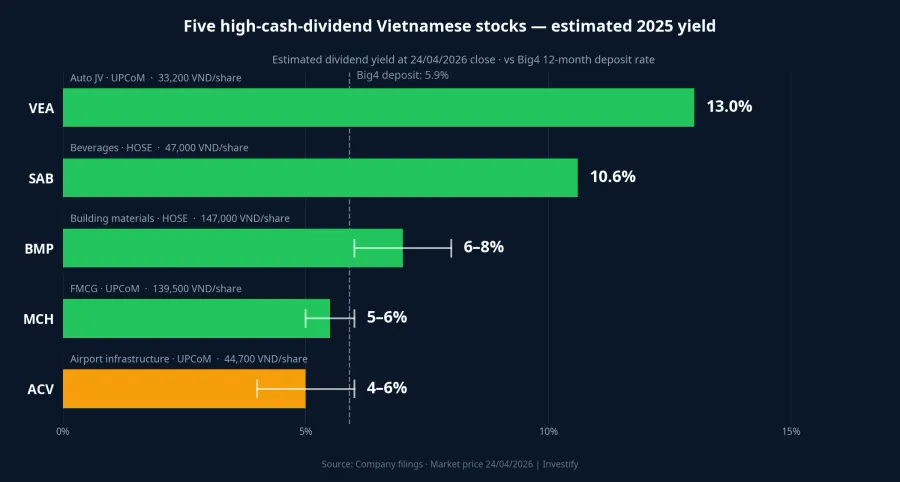

- VEA (VND 33,200/share): UPCoM-listed company collecting dividends from its Honda, Toyota and Suzuki Vietnam joint ventures, with an estimated 2025 yield of about 13%. Two cash dividend payments per year, every year from 2020 to 2025. Risk: dependence on the auto sales cycle and vehicle tax policy.

- SAB (VND 47,000/share): roughly 10.6% yield in 2025, consistent payout history 2020–2025. The key caveat is that 2025 payout exceeds 100% of net income, so sustainability depends on the cash buffer; 9-month 2025 revenue fell 17% year-on-year under the new special consumption tax and Decree 100.Vietstock

- BMP (VND 147,000/share): payout ratio 80–90%, cash dividends of VND 3,000–4,000 per share sustained for years, estimated 2025 yield of 6–8%. Low debt, stable operating cash flow from its construction-pipe business.

- MCH (VND 139,500/share): FMCG with high dividends over many years, around 5–6% yield. Cash flows are routed primarily to parent MSN, so retail investors receive only a small share of total MCH distributions.

- ACV (VND 44,700/share): state-controlled airport infrastructure, stable airport-fee cash flow, estimated 2025 yield of 4–6%. Sits at the borderline of criterion 1, so weigh carefully.

Three risks to read before treating dividends as a savings substitute

One — dividends from non-recurring sources. Some real-estate and construction names have paid unusually high dividends funded by project divestments or land transfers, not core operations. Phat Dat (PDR) booked higher profits in several quarters from exiting Cadia Quy Nhon and selling much of the Thuan An 1 project; TAL recorded large gains from transferring the Tay Ho Tay and Landmark 55 projects. When the one-off income runs out, next year's dividend rarely holds at the same level.

Two — payout exceeds free cash flow. A company can fund distributions with new debt or by drawing down accumulated cash. Quick check: sum cash dividends over the last five years and compare with cumulative free cash flow over the same period. If dividends exceed FCF year after year, the buffer drains — it's only a question of when the cut comes.

Three — sector at a cyclical peak. Sugar, certain commodity names and some industrial-park stocks occasionally show high yields purely because commodity prices or sector cycles are at a peak. When the cycle turns, profits drop, dividends fall the following year, and the share price corrects at the same time. Investors lose income and principal simultaneously, exactly when the position was supposed to be the safest.

Conclusion: a supplement when the savings spread is thin, not a replacement

In a world where the real savings spread is just 1.25 points, a cash-dividend portfolio with a 6–8% after-tax yield and 4–6 stocks meeting all four criteria can be a sensible allocation. A common weighting for income-oriented retail investors is 15–30% of the portfolio, depending on tolerance for principal volatility.

But equities remain equities. Principal moves with the VN-Index, dividends can be cut in a bad year, and a sector-specific shock can drop a price 20–30% in just a few sessions. Cash dividends are a supplement to deposits when the real spread is thin — not a wholesale replacement.

The four-day 30/4–3/5 holiday is a sensible pause to audit the portfolio: open every holding, run it through the four criteria (after-tax yield, five-year history, free cash flow, payout), and strike the names that don't pass. When the market reopens on 4 May, what remains is a starting framework — not a buy list, but a screen to keep a clear head when a 13% yield on the ticker tape tempts you to click the button now.