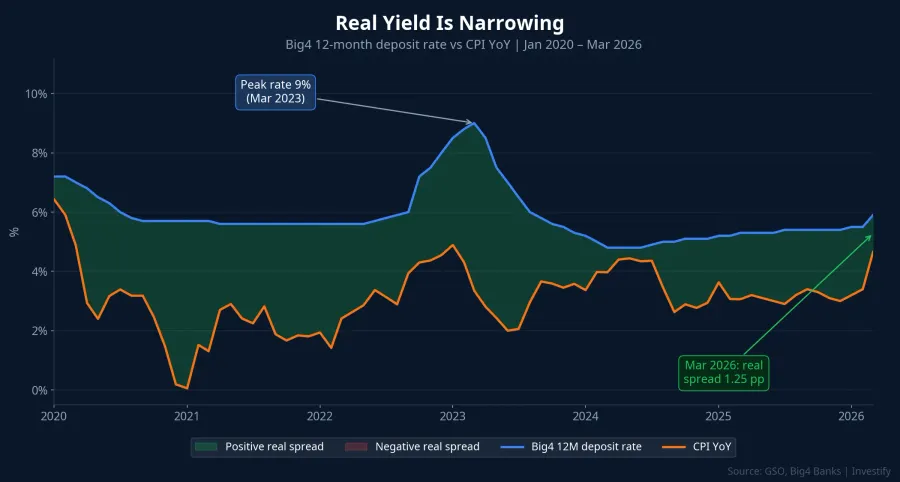

In April 2026, Vietnam's four state-owned banks — Vietcombank, BIDV, VietinBank, and Agribank — all quote a 12-month deposit rate of 5.9% per year.VnEconomy At the same time, the General Statistics Office reported headline CPI of 4.65% year-on-year for March 2026 — the highest March reading in five years. A simple subtraction puts every saver in front of the same small number: 5.9 minus 4.65 leaves a real positive yield of just 1.25 percentage points for each year you keep the money on deposit.

To put it plainly: park VND 100 million in a 12-month deposit at the Big4 and you'll receive VND 5.9 million in nominal interest after a year. But if prices rise by exactly 4.65% during that year, the purchasing power of your VND 100 million falls by roughly VND 4.65 million. The "real interest" left in your wallet is only about VND 1.25 million — the price of one nice family dinner per month. Meanwhile, household deposits in the banking system have crossed VND 7.83 quadrillion, a fresh record, according to the State Bank of Vietnam.ThuongTruong

These two data points together tell a six-year story: how nominal rates moved through cycles, how the real-yield spread shifted for savers, and why Vietnamese household money still chooses to sit at the bank counter even when the headline rate no longer looks attractive.

Six years of cycles: from a wide spread to 1.25 pp

2020–2021: low nominal rates, even lower inflation. The pandemic forced the State Bank of Vietnam to cut policy rates by a cumulative 200 basis points in 2020.SBV Big4 12-month rates fell into the 5–5.5% range. But average 2021 CPI came in at just 1.32% — the lowest reading of the entire decade. A saver locking in 100 million at 12 months that year took home a real yield north of 4 percentage points. This was the widest real-rate spread of the six years.

Q4 2022: a global inflation shock and a brief peak. In late Q3 and Q4 2022, the State Bank raised policy rates by a combined 200 basis points to keep up with the Fed's tightening cycle and to defend the dong. Twelve-month deposit rates at many private banks jumped to 9–10%. Average 2022 CPI was 2.82%, and the real spread peaked at 6–7 percentage points. But that peak only lasted a few months — savers who didn't lock in a long tenor in time missed it.

2023: four rate cuts and a narrower spread. Through 2023, the State Bank cut policy rates four times for a cumulative 150 basis points.ThoiBaoTaiChinh Big4 12-month rates slid to 5–6%, while average 2023 CPI reached 3.74% — the highest of the 2020–2025 stretch. The real spread compressed to 1.5–2 pp. This was the first year savers genuinely felt the pinch: the same money lost purchasing power faster than the year before, while the interest received was smaller.

2024 to early 2026: a stable low-rate plateau. From early 2024 through February 2026, the State Bank held the policy rate steady at 4.5%. Big4 12-month rates drifted between 4.7% and 5.5%. Average CPI was 3.17% in 2024 and 3.26% in 2025, so the real spread settled into a 1.5–2.5 pp range. Savers got used to the new normal: nowhere near the highs of 2022, but still a positive real yield large enough that the money didn't visibly erode.

March 2026 breaks the equilibrium: CPI tops 4.65%

March 2026 broke a five-year record. CPI YoY hit 4.65%, driven by the transport group rising 12.85% (diesel +57.03%, gasoline +29.72%) on Middle East tensions and a global supply shock in oil.CafeF Average Q1 2026 CPI came in at 3.51%.TinNhanhChungKhoan

Set against the Big4's 5.9% 12-month rate, the real-yield spread for that tenor shrinks to just 1.25 pp. At the 6-month tenor, the Big4 are quoting around 3.5% — a negative real yield of 1.15 pp versus March CPI. Anyone with a short-tenor Big4 deposit today is accepting that purchasing power is falling faster than the interest they're receiving.

For a more concrete picture: VND 1 billion at 12 months earns VND 59 million in nominal interest, but loses around VND 46.5 million in purchasing power if CPI holds at the current level for a full year. Real interest left: VND 12.5 million. That figure is lower than what a private bank would pay you on demand deposits compounded over the same year — something hard to imagine three years ago.

The 7.83-quadrillion paradox: why money stays at the counter

The real spread has narrowed but household deposits still hit a record VND 7.83 quadrillion. The paradox isn't irrational — it's explained by mechanisms independent of nominal interest rates.

SJC gold has just fallen 13–16% from the January 2026 peak of USD 5,600/oz, after roughly doubling in 2025; bottom-fishers are hesitant and waiting for a clearer signal. Hanoi secondary real estate is frozen even as Vingroup keeps pushing primary inventory at the high end. The VN-Index whipsawed through Q1 and is down about 6%. Among the four main household channels — gold, real estate, equities, deposits — the simplest, most liquid, and the one covered by deposit insurance up to VND 125 million per person per bankDIV is still saving at the bank.

A second factor is holiday psychology. Four days off from April 30 to May 3, plus an unsettled geopolitical backdrop, means defensive instincts beat yield-seeking. The third factor — and probably the most important — is the savings habit itself: for most households, deposits are not a quarterly investment decision but the default residual flow of monthly income after spending. Money lands in the account, part stays in the savings book, the term matures and is rolled. That mechanism doesn't change for 1.25 percentage points.

The Big4 are not the only option

When the real spread narrows to 1.25 pp on long tenors and turns negative on short tenors at the Big4, a saver's portfolio has a few standard adjustments — the kind that mature markets typically make under similar conditions.

Private banks. Top private banks are paying 0.3–0.8 pp more than the Big4 at 12 months: TCB 6.25%, VPB 6.7%, STB 6.3%, ACB 5.8%. Hong Leong leads the foreign bank cohort at 7.5% per year.VnEconomy That spread, multiplied by VND 7.83 quadrillion, is not a small amount. Moving part of your deposit from the Big4 to top private banks can lift the real yield by 0.3–0.8 pp — pushing your "real positive" share from 1.25 up to 1.5–2 pp. The personal call still depends on how comfortable you are with the receiving bank's balance sheet, since deposit insurance only covers up to VND 125 million per person per bank.

The yield curve and a laddering strategy. Per April 2026 data, the spread between 6–9 months and 1–3 months averages around 1 pp, and the spread between 12 months and 6–9 months around 0.5 pp. A portfolio sitting entirely in 1–3 months for liquidity is paying a hefty price for that flexibility. Laddering — a small slice in short tenors as a buffer, the bulk at 6–12 months to capture the steepest part of the curve, and a slice at 12–18 months to lock in if rates fall further — lifts the average yield without locking up all the capital long-term.

Fixed-yield products. Bank-issued retail bonds and long-tenor certificates of deposit typically pay 1–2 pp more than a savings deposit of the same tenor, in exchange for lower liquidity and dependence on the issuer's credit. Retail government bonds offer better liquidity but lower yields — in Q1 2026, the auction yield on 10-year Vietnamese government bonds was around 4.06%. Fixed-yield products on regulated distribution platforms are running at 7–11% per year depending on tenor — more attractive than a Big4 deposit, but with credit risk and specific early-redemption terms attached.

Marginal inflation hedges. Gold has fallen sharply from the peak but is still a channel many Vietnamese households use to balance CPI risk; bond fund certificates let you earn yields close to government bonds with T+3 liquidity.

What to watch in the second half of 2026

The question for H2 is whether CPI holds in the 4–5% zone or drifts higher — which depends on energy prices and the stability of the Strait of Hormuz. If CPI stays at 4.65%, a 5.9% Big4 12-month rate keeps the real spread at 1.25 pp; if CPI moves to 5%, the spread compresses to 0.9 pp. On the other side, every 0.5-pp uptick at private banks — like the March 2026 round of moves at BIDV, VPB and TCB — widens the gap between Big4 and private banks and pushes yield-sensitive savers to reconsider where their money lives.

Six years of saving have moved from a wide real spread to a narrow one. What's left for a saver is not to walk away from the bank — deposit insurance and liquidity still matter — but to stop letting the entire VND 100 million, 500 million, or 1 billion sit in a single tenor at a single bank, when the yield curve and product menu are far broader than they were in 2020.

A worthwhile question to ask yourself, looking at your portfolio today: of every 100 dong of savings you currently hold, how many are sitting in short Big4 tenors — where the real yield is roughly zero or negative — and how many are in tenors, banks, or products that actually capture the April 2026 yield curve?