On the weekend of 24 April 2026, two data sets pulled in opposite directions inside the same few-hour window. Wall Street was celebrating: the Nasdaq closed at 24,836.60 (+1.63% on the session) and was tracking its best month since April 2020 with April up 15%; Nvidia closed at $208.27 (+4.3%), pushing market cap above $5 trillion — the first publicly traded company to reach that mark; and the VIX fear gauge dropped to 18.71, a one-month low.CNBC

The other side was insider data from the energy industry. The International Energy Agency (IEA) released a report saying the Iran war is forcing the global natural gas market into a tight regime for at least two more years.Yahoo Finance The same day, Baker Hughes released its Q1 2026 results, showing record IET orders of $4.9 billion and a backlog of $33.1 billion — an all-time high.Seeking Alpha

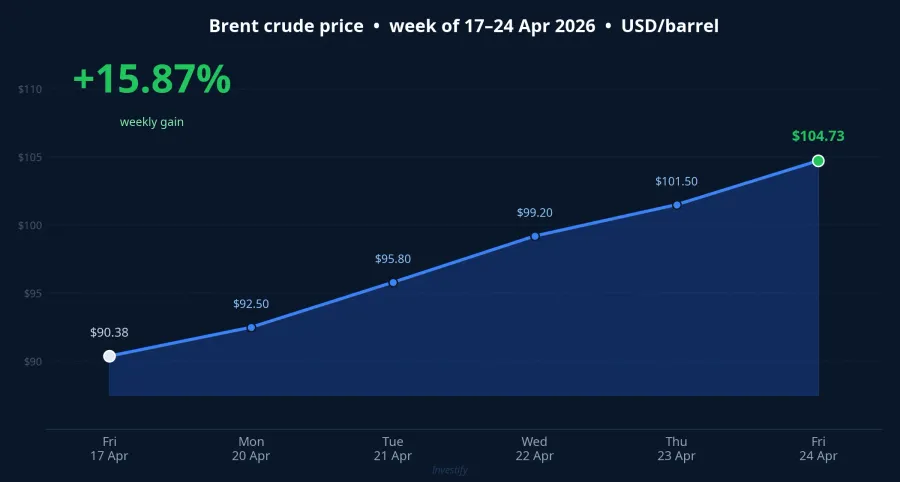

Brent reacted in line with the insider data, closing the week at $104.73 per barrel, up 15.87% from 17 April — the largest weekly move in months. US equities, and AI chip names in particular, traded as if the geopolitical risk had already been fully priced in.

The popular market view: "Iran-Hormuz is already in the price; this will all cool off quickly." The two reports released on 24 April say the opposite, on the record.

Two gauges, two answers, in the same 24 hours

The bigger picture shows the financial market splitting its signal in two. The equity side acts as if the Middle East risk is short-term and already priced. The commodity side — where real buyers and sellers transact actual barrels — is pricing for a multi-quarter supply squeeze.

Capital is flowing along two different logics, but both cannot be right. Over the next 6–24 months, one of the two will have to converge toward the other. The question is no longer "has the risk been priced in?" but "which gauge is lagging?"

IEA: 17% of Qatar's LNG capacity will take years to repair

The IEA report identifies the source of the squeeze precisely. The strikes on Ras Laffan Industrial City in Qatar — the world's largest liquefaction hub — cut 17% of LNG capacity, and the infrastructure damage is expected to take years to fully repair.CBS News For March–April 2026 alone, the IEA estimates a loss of about 20 billion cubic meters of LNG from Qatar and the UAE. Combined with delayed liquefaction expansions worldwide, the system is set to be short roughly 120 billion cubic meters of LNG by 2030 versus the reference scenario.The National

This is not a multi-week disruption. The 120 bcm gap by 2030 is gas that importing nations (in Asia and Europe) will have to compete for in the spot market at elevated prices for an extended period. The long-term LNG contract repricing that analysts expected to "cool from 2027" has just been pushed back by at least two years.

Baker Hughes: $33.1 billion backlog is the clearest insider signal

Baker Hughes's Q1 2026 numbers reinforce the IEA's reading. Q1 revenue came in at $6.59 billion (+2.5% year-on-year), adjusted EPS of $0.58 beat consensus, and net income reached $930 million.Benzinga What matters more than the rear-view numbers is the order book: a record $4.9 billion in IET orders for the quarter, an all-time-high backlog of $33.1 billion, and a 1.5x book-to-bill ratio.Oil and Gas 360

Lorenzo Simonelli, Chairman and CEO of Baker Hughes, struck a measured tone on the earnings call: Q1 IET revenue was already affected by shipping delays through Middle East sea lanes, management sees a "normalized environment" only in the second half of the year, and the OFSE oilfield services segment will absorb more logistics impact than IET. This is how an industry CEO speaks when geopolitical risk is not over but customers are still placing record orders for LNG and gas equipment — because they believe gas prices will stay elevated for an extended period.

The diplomatic side is not flashing a quick risk-off signal either. Middle East Special Envoy Steve Witkoff and Senior Advisor to the President Jared Kushner traveled to Pakistan over the weekend of 24 April to negotiate with Iranian Foreign Minister Abbas Araghchi.CNBC The first round, led by Vice President Vance two weeks earlier, "ended without an agreement," and this second round saw Iran publicly deny that any meeting had been scheduled before the plane even took off.Al Jazeera

Why Wall Street cannot measure Hormuz

Wall Street's risk-on sentiment has its own internal logic. The VIX at 18.71 is not a reading on geopolitical risk — it is a reading on AI capital flows. Intel reported a Q1 beat and the stock jumped 24% on Friday (its best session since 1987); Nvidia's 4.3% gain pushed market cap past $5 trillion; the Nasdaq is up 15% for April.Yahoo Finance When a handful of mega-cap AI chip names run on their own beat, the broad indices (S&P 500, Nasdaq) get pulled higher by a few heavyweight stocks, and the volatility implied on the broad basket (VIX) compresses.

But that is sentiment, not an assessment of oil and gas supply. Brent +15.87% on the week is a reading on the physical market. When two gauges give two different answers, that does not mean one is wrong and the other right. They are measuring different things, and the risk lies in the fact that one of them will eventually have to converge.

Three alternative explanations need to be ruled out before committing to a scenario:

- "Brent rose because of a short squeeze, not supply": short squeezes typically resolve in 1–3 sessions. This is a five-session run (20–24 April), from $90.38 to $104.73. The pattern fits supply repricing better than position covering.

- "VIX 18.7 already prices the risk": VIX measures S&P 500 volatility. The S&P 500 does not have enough energy weighting for VIX to reflect Hormuz risk (XLE is only about 3% of the S&P 500). Volatility on a basket of chip + financial + consumer names is not a gauge of Middle East geopolitics.

- "Pakistan talks will defuse the situation": possibly, but the first round failed and the second was disowned by Iran before it even began. The short-term probability is not high enough for the IEA or Baker Hughes to revise guidance. Both have set the equilibrium point in H2 2026.

The more accurate framing: Iran-Hormuz risk is moving from a short-term tail risk (1–3 months) to a base case lasting 6–24 months, and the equity gauge (VIX, Nasdaq) is lagging the commodity gauge (Brent, LNG, IET orders).

Pass-through to Vietnam: a thin price-stabilization buffer

Vietnam is a net energy importer. A 15.87% weekly Brent move passes through to the domestic economy via two channels: retail fuel prices and gas prices for fertilizer and power generation.

In the 24 April adjustment cycle, domestic retail prices moved against the global tape: E5 RON92 gasoline came in at 21,830 VND per liter, RON95 at 22,880 VND, diesel at 26,690 VND, and mazut at 18,810 VND per kg, all 820–1,160 VND below the previous cycle.Eva.vn The reason: the inter-ministerial price authority drew 400 VND per liter of diesel and 400 VND per kg of mazut from the Price Stabilization Fund, while contributing 200–600 VND per liter on other products.

This is a buffer with limits. The Stabilization Fund is replenished and drawn down cycle by cycle. If Brent stays above $100 per barrel for several consecutive weeks, the disbursement headroom shrinks. Each cycle that goes against the global tape is a cycle of net withdrawal.

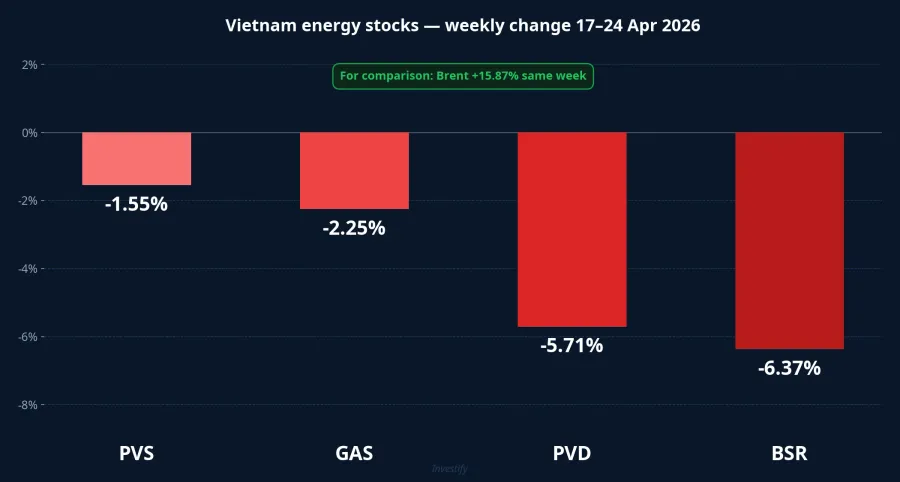

On the exchange, Vietnam's energy stocks reacted weakly last week, not yet pricing the scenario of an extended high-oil regime. Versus the 17 April close: PVS down 1.55%, GAS down 2.25%, PVD down 5.71%, BSR down 6.37%. Domestic retail investor sentiment is leaning toward "ceasefire is coming soon," aligning with Wall Street and against the IEA and Baker Hughes data.

The VN-Index closed 24 April at 1,853.29, down 0.91% on the session.

Asset allocation framework under an H2 2026 scenario

Once energy risk is reclassified from a short-term tail risk to a 6–24 month base case, the portfolio structure needs to shift accordingly. This is an analytical framework, not a stock-by-stock recommendation.

The natural beneficiaries of sustained high energy prices are energy commodities (Brent, gas) and upstream operators, accessible via MXV (Vietnam's Commodity Exchange under the Ministry of Industry and Trade, with Nano Contracts lowering the capital threshold). Vietnamese energy stocks (PVS, PVD, GAS, BSR) are a secondary channel: cyclically sensitive to oil but also dependent on inventory cycles, retail price reset windows, and domestic gas planning.

The pressured layer includes urea producers (DCM, DPM), shipping and aviation, and consumer-goods firms with heavy logistics costs. Gross margins are vulnerable when oil holds above $100 per barrel for several quarters, and the ability to pass input cost into selling prices depends on global demand and inventory. Q1 results should be reviewed before committing to this layer.

The stable layer in an extended shock consists of 12-month bank deposits (Big4 5.0–5.5%, smaller banks 7–8% per year) and fixed-income products yielding 9–11% per year, providing liquidity while waiting for the energy risk to resolve. A 15–25% cash weight is a typical defensive range when the macro base case is upgraded.

Signals to watch

The question is no longer "has Iran-Hormuz been priced in?" because Wall Street and industry insiders are giving opposite answers. The real question is "which side is lagging?" — and four signals over the next 4–6 weeks should answer it:

- Brent staying above $100 for four consecutive weeks confirms a structural premium. Brent dropping below $90 within two weeks signals tail risk has receded.

- The Witkoff–Kushner–Araghchi talks in Islamabad: whether a concrete deal emerges within two weeks.

- The IEA Oil Market Report in May: whether it maintains the "tight for two years" guidance or revises it.

- Baker Hughes's Q2 guidance (next quarter): whether it holds to a "normalized environment in H2" or pushes the timeline into 2027.

Allocation decisions should account for the cost of repositioning before the energy price gap fully feeds through into equities, inflation, and the USD/VND exchange rate. When two gauges sit at opposite ends, those who play defense early pay a lower premium than those who play defense late.