At Petrolimex's Annual General Meeting on the morning of 24 April 2026, CEO Lưu Văn Tuyển announced the company expected a loss of over VND 1,000 billion from its fuel business in Q1/2026, even as other business lines continued to operate normally.VnExpress The cause, Tuyển said, was global oil price swings of USD 20–50 per barrel per day since late February — a range he called "unprecedented in history".CafeF

The statement puts individual investors face-to-face with a paradox: why does Vietnam's largest fuel company report a loss in a quarter when Brent crude is moving up? The answer is not in the direction of the price, but in its velocity.

Volatility, not direction, is what broke margins

The default assumption of many retail investors is simple: when oil goes up, fuel distributors make money. For an upstream distributor like Petrolimex, that logic only holds when prices trend smoothly. When daily volatility widens too much, the opposite happens.

The mechanism lies in the inventory cycle. By regulation, fuel distributors must maintain around 30 days of reserves to secure supply. Cargo imported this week gets sold at a base price the regulator sets two weeks later. When the global price trends smoothly, that lag is harmless — purchase and selling prices glide along the same curve. But when Brent swings USD 20–50 per barrel per day, peak-priced cargo gets sold after the market has fallen; trough-priced cargo gets sold after the market rebounds. Both sides grind down the margin.

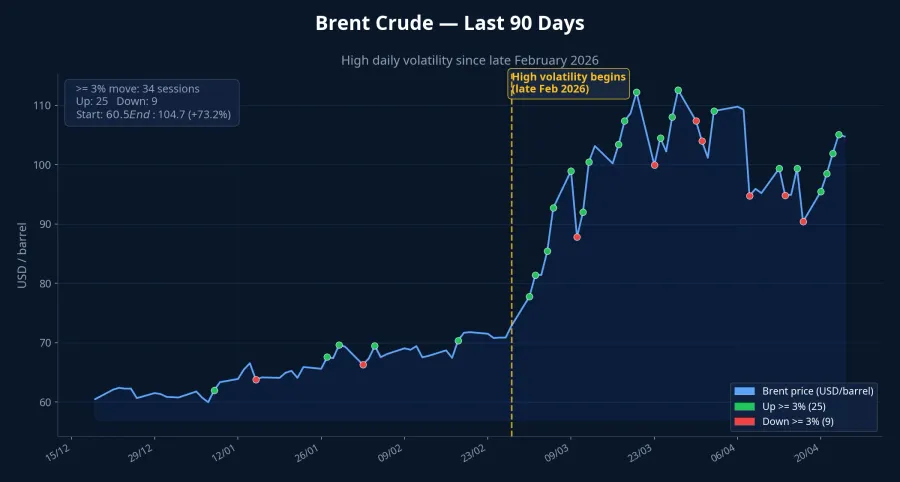

The past 90 days of data show the scale of the shock. Since late February 2026, Brent has recorded 34 sessions with moves of 3% or more out of roughly 60 trading days — more than half the sessions. In the 20–24 April window alone, prices rose from USD 95.48 to USD 104.73 per barrel, or +9.7% over five consecutive sessions, including a +5.64% move on 20 April and a -13.29% drop on 8 April. This is a range that Vietnam's 7–10 day domestic price-adjustment cycle has no chance of tracking.

Price management cycle and Stabilization Fund both ran out of cushion

The adjustment round starting at 15:00 on 23 April shows the scale of the correction: E5 RON92 fell VND 100 per litre to VND 21,830, RON95 dropped VND 162 to VND 22,880, and diesel fell VND 1,159 to VND 26,690 per litre.Techz Diesel alone has fallen more than VND 18,000 per litre from its historical peak — roughly 40%. But domestic retail adjustments only happen on a 7–10 day cycle, while input prices change daily. That lag is exactly where an upstream distributor's inventory gets stuck.

The Fuel Price Stabilization Fund is supposed to cushion precisely this situation, but the fund is thin. The total fund balance stood at around VND 390 billion as of 23 April 2026, down sharply after the joint ministries drew continuously from it from 10 March onwards, at VND 4,000–5,000 per litre, to soften price shocks during the oil surge. The 23 April round made no gasoline contribution to the fund, taking only VND 400 per litre from diesel and mazut — far below the shock-period levels and a clear signal that intervention headroom has narrowed.

Both traditional cushions — the 7–10 day adjustment cycle and the Stabilization Fund — have proven insufficient to absorb the current swing range. The VND 1,000 billion Q1 loss is the direct financial consequence of those two layers failing together.

Three problems to solve at once

Layer one: the 2026 plan has not been revised down. Despite the Q1 loss, Petrolimex is sticking to its 2026 plan: consolidated revenue of VND 315,000 billion (up 2% versus 2025, a historical high), pre-tax profit of VND 3,380 billion (down 7%) and 19.4 million tonnes of sales volume (up 10%).Nhịp sống Kinh doanh The remaining three quarters must absorb the entire Q1 loss and still hit the plan. The precondition is that Brent volatility normalizes and the domestic price-management cycle resumes its cushioning role — neither is in the company's hands.

Layer two: long-term consumption structure. At the AGM, Tuyển confirmed Petrolimex will establish a new subsidiary for batteries and electric vehicles in early May 2026.Vietstock The integrated-station model with EV charging, battery swapping and clean fuels will roll out on the existing network of around 3,000 retail stations, with partners from Singapore, China and Korea. Petrolimex itself has flagged in its 2026 submission the pressure on sales volume from EV adoption hitting the traditional business.CafeBiz That is a rare case of a leading company openly acknowledging its core business will shrink over the long run.

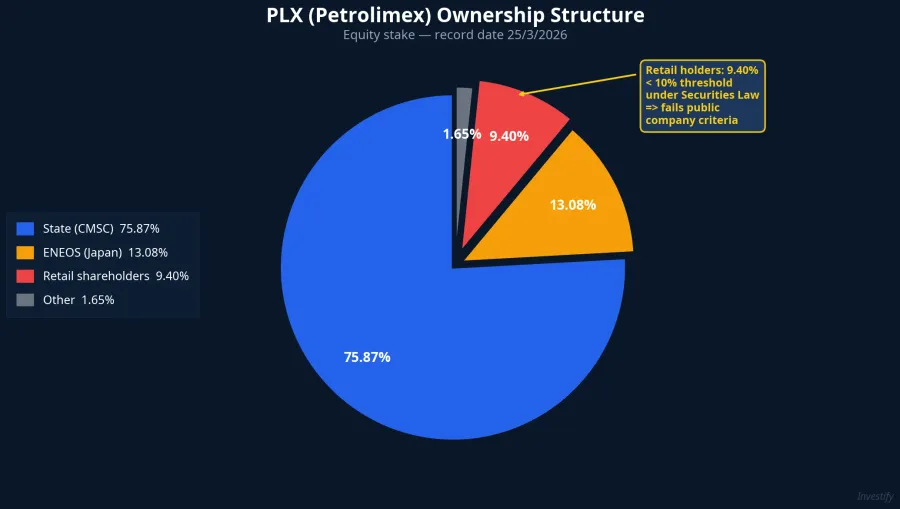

Layer three: the ownership problem. As of the record date 25 March 2026, Petrolimex had 43,266 shareholders, but the retail group holds only 9.4% of voting capital — below the 10% threshold that the 2019 Securities Law requires for public company status.Dân Trí The reason is concentrated ownership: the State holds 75.87% and strategic shareholder ENEOS Corporation holds 13.08%, combining for 88.95%.ZNews The company has a one-year window to remedy this; failing that, it must file to deregister its public company status.

The two remedies Petrolimex proposes are selling down treasury shares or reducing State ownership.CafeF Both require approval from the State Capital management authority and cannot be executed within a few months. Loss of public company status is an extreme scenario, but even with an extension, concentrated ownership remains the factor pinning PLX's valuation below peers of similar size.

Re-reading expectations for PLX stock

Look at the market's reaction in numbers. PLX closed 24 April at VND 39,700, up 1.02% on the day the loss was announced, and 12.5% higher than the VND 35,300 close on 31 December 2025. Market cap is around VND 50.4 trillion, P/E around 15.1x and P/B at 1.55x.

What stands out is that the market did not react strongly to the Q1 loss news. For institutional investors, this loss had already been within view since the 2026 plan was published in early April — pre-tax profit was proactively guided 7% lower versus 2025, implying management saw the pressure coming. The VND 39,000–40,000 range has priced in this news fairly fully; further upside or downside depends more on the three structural factors already discussed.

For retail holders treating PLX as a state-owned dividend stock, three signals worth watching over the next 2–3 months:

- Brent's daily volatility range in May. If daily swings compress below USD 5 per day, the domestic price-management cycle can resume normal operation and inventory-driven loss risk eases meaningfully.

- Capital size announcement for the new battery/EV subsidiary. The specific number signals how deep the revenue-structure shift is. If allocation is small relative to the core business, the EV story remains a pilot; if large, it becomes the long-term valuation catalyst.

- The plan to lift the free float. If the State divests part of its stake, or Petrolimex sells treasury shares into the market, liquidity and valuation could be re-rated.

The core thesis holds: Petrolimex sits in a transition zone, absorbing a short-term shock from oil volatility, having to shift structurally into a decade of EVs, and dealing with a legacy ownership problem. This is not a cyclical stock that benefits directly when oil rises — it is an energy retail infrastructure stock rewriting its own business model. The three signals above form the framework for judging how far the company has actually moved along that path.