On April 23, 2026, three US tech giants made announcements that look unrelated at first glance but tell a single coherent story when you place them side by side. Meta cut 10% of its workforce. Microsoft opened its first voluntary retirement program in 51 years of corporate history. Intel delivered a Q1 beat that surprised even optimists. One day, one mechanism: the product side of the AI stack is freeing up payroll to fund infrastructure, while the chip and server side is already booking that capital as revenue.

The bigger picture matters because it shows the AI investment cycle has entered a stage where capital flows visibly from one set of companies to another — and the same framework reads across to tech stocks listed in Vietnam.

Meta: 10% headcount cut, capex nearly doubled

Meta is cutting 8,000 jobs (10% of its workforce), effective May 20, while also closing 6,000 unfilled roles.CNBC Measured against its 78,865-person headcount at the end of 2025, this is the sharpest restructuring since the 2023 "year of efficiency."TechCrunch

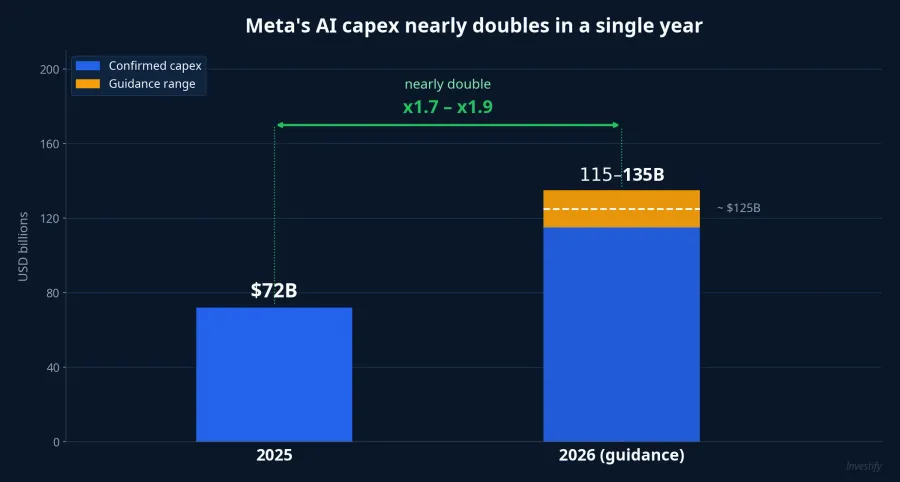

The more important number isn't the layoff headcount — it's where the freed capital is going. Meta set 2026 capex guidance at $115–135 billion, roughly double the $72 billion spent in 2025. Put differently, the payroll savings don't even come close to offsetting the extra capex; they're a rounding error. The real capital stream flows into three buckets: next-generation AI data centers, custom silicon (both in-house MTIA and external GPUs), and foundation models like Llama.

This is a clear signal of strategic priority. Meta isn't restructuring to cut costs — it's restructuring to shift the cost mix, from payroll toward depreciation on hardware. For investors, the thing to watch is operating margin over the next 2–3 quarters: if capex scales faster than ad revenue, EPS pressure shows up well before the AI payoff lands in the P&L.

Microsoft: first voluntary buyout in 51 years

On the same day, Microsoft opened a voluntary retirement program to roughly 7% of its US employees — about 8,750 people.CNBC This is the first time in Microsoft's 51-year history that it has used this instrument. Eligibility is capped at senior director level and below, with age plus tenure summing to at least 70 years; employees on sales incentive plans are excluded. Program details are set to reach eligible staff on May 7.Bloomberg

Voluntary buyouts are a familiar tool in telecoms and legacy manufacturing, but Big Tech has historically leaned on direct layoffs. Microsoft's pivot to a buyout signals two things. First, the payroll relief the company needs is large enough to justify paying upfront for a voluntary package rather than forcing the change through layoffs. Second, Microsoft is willing to absorb that short-term charge in exchange for cleaner cost discipline over the medium term — fewer legal fights, less morale damage. The freed budget continues to flow into Azure, supercomputing infrastructure, and AI products.

Intel: Q1 beats across the board, data center up 22%

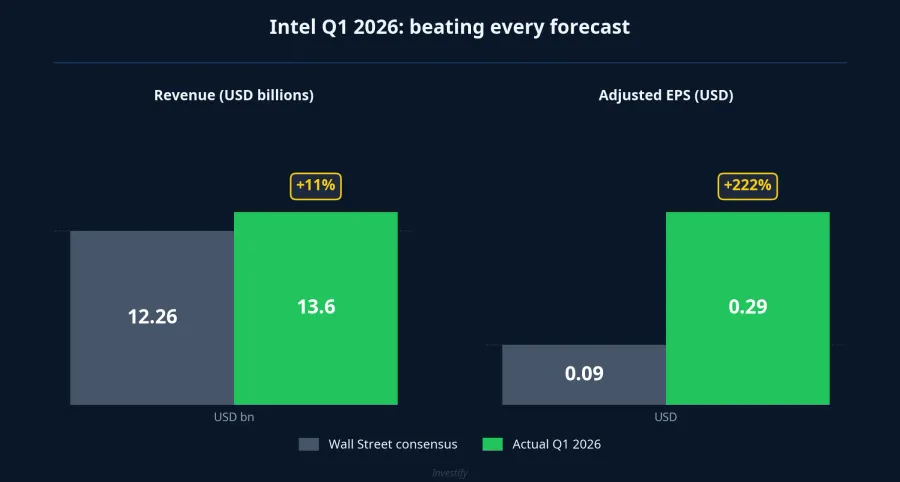

On the other side of the value chain, Intel reported Q1 2026 revenue of $13.6 billion against a consensus estimate of $12.26 billion, and adjusted EPS of 29 cents against 9 cents expected.CNBC Data Center and AI (DCAI) revenue climbed 22% to $5.1 billion, driven by demand for AI server CPUs.Intel Intel shares jumped roughly 20% in after-hours trading.Yahoo Finance

Q2 guidance is equally constructive: revenue of $13.8–14.8 billion and adjusted EPS of 20 cents, both above street estimates. CEO Lip-Bu Tan reaffirmed the AI-first playbook, with server CPUs and foundry services as the two load-bearing pillars. The server CPU market used to be dismissed as sleepy compared to Nvidia's GPU franchise, but agentic workloads have pulled CPU demand back into the conversation.

What's interesting isn't Q1 itself but the timing. Meta and Microsoft only announced their cost cuts in April, while Intel is already booking revenue from CPU orders placed for AI clusters in prior quarters. Cash flow to the supply side runs ahead of cash savings on the product side, because capex is an outbound order booked upfront, while headcount reduction is a drip of savings over time.

The cross-mechanism: one company's cost is another's revenue

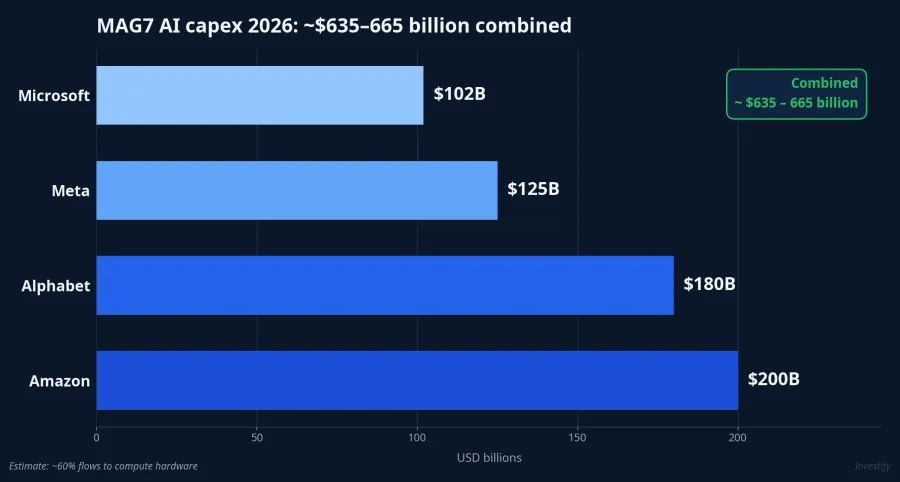

Line the three announcements up and the mechanism is unmistakable. Most of Meta's $115–135 billion 2026 capex, alongside Microsoft's comparable capex (estimated at $100–105 billion), flows straight into chips, servers, and data centers. Combined 2026 AI capex from Amazon, Alphabet, Microsoft, and Meta is estimated at $635–665 billion, with roughly 60% of AI data center cost landing in compute hardware.

The direct beneficiaries fall into four groups. Nvidia still leads with training and inference GPUs, holding the largest share of AI compute hardware. Intel and AMD split the server CPU and accelerator market, with Intel carrying an additional foundry leg. Broadcom supplies high-speed interconnect silicon for large AI clusters. And TSMC sits at the bottom of the stack — 2026 capex of $52–56 billion, producing most of the AI silicon for the entire ecosystem.

The question that matters for investors isn't "who wins AI?" — the entire hardware group is winning in this cycle — but rather when. Which side books revenue first, and which side follows. That's the framework that translates to the Vietnamese market.

Reading Vietnam's tech stocks through the same lens

The split between "capital-consuming AI product companies" and "infrastructure-selling companies" applies cleanly to the tech basket listed in Vietnam, even if the scale is nothing like US Big Tech.

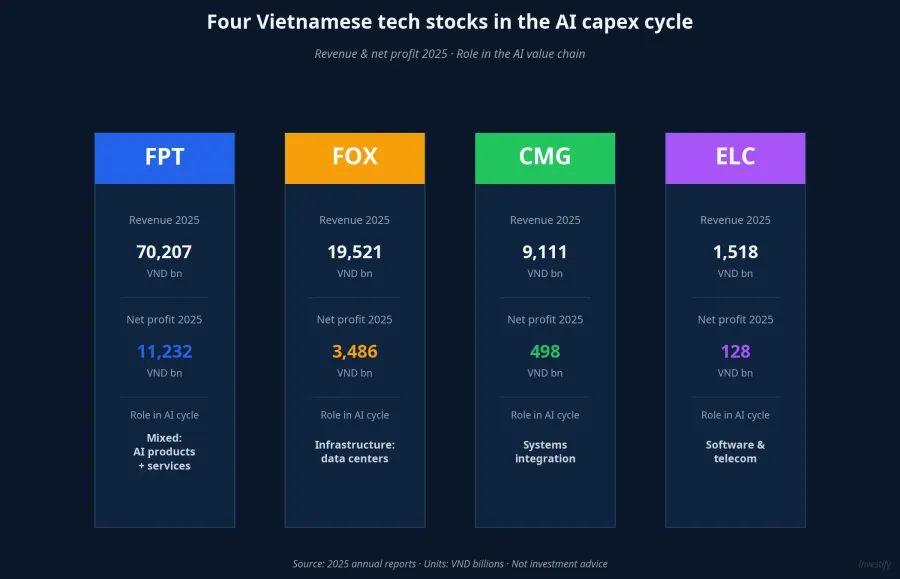

FPT carries a mixed role: it invests in AI factories and AI products, while also selling IT services to domestic and international clients. 2025 revenue came in at VND 70,207 billion with after-tax profit of VND 11,232 billion. Q1 2026 has already reported approximately VND 12,480 billion in revenue and VND 2,804 billion in pre-tax profit.Vietstock

FOX (FPT Telecom) leans toward the infrastructure supply side: 2026 capex plan of around VND 5,100 billion, mostly for data centers and cable infrastructure. 2025 revenue was VND 19,521 billion with after-tax profit of VND 3,486 billion, giving a net margin near 18%, one of the highest in Vietnam's tech universe.

CMG specializes in systems integration and IT services for government and financial clients. 2025 revenue was VND 9,111 billion with after-tax profit of VND 498 billion; free cash flow is negative thanks to heavy capex — the classic signature of a firm still consuming capital rather than selling infrastructure.

ELC provides software and telecom solutions for security, surveillance, and conferencing. 2025 revenue was VND 1,518 billion with after-tax profit of VND 128 billion; its investment cycle is long and heavily dependent on public budget allocation, making cash flow uneven.

The simple read: firms that have already shifted into selling infrastructure services (FOX with data centers, or CMG's signed IT backlog) will book revenue earlier than firms still spending on AI products (FPT's AI factory exposure, ELC's budget-dependent projects). The two groups aren't opposed; they're out of phase on the cash flow timeline.

Three signals to watch over the next 2–3 weeks

The "one side's cost is another's revenue" framework only holds if the capital actually flows, and May offers three checkpoints.

On May 7, Microsoft sends buyout program details to employees. The take-up rate is the real-world gauge of how much payroll is being freed — a high take-up confirms the "reallocate to AI" story; a low one forces Microsoft back to another tool.

Q1 reports from Nvidia, AMD, and Broadcom (expected late April to early May) will confirm whether MAG7 capex is flowing uniformly into the chip group the way Intel has already signaled. If all three show data center revenue beating estimates, the cross-mechanism has full data confirmation.

Finally, Q1 2026 results from FOX and CMG — typically released in late April or early May — are the litmus test for the Vietnamese read. If FOX reports accelerating data center revenue and CMG books a large contract backlog, the domestic "selling infrastructure" leg is squarely in the early phase of the cycle. Without that data, the framework is still a working hypothesis, not a conclusion.