The 2026 AGM season puts an old question back under the microphone: when shareholders ask about the share price, how should a CEO answer? Across April 17–22, four people running four industry-leading companies gave four answers. Line them up and they collapse into two opposite camps.

Three leaders flatly refused to recommend. One called on shareholders to buy — and backed it with real purchases. A casual reader tends to feel let down by the first camp and energized by the second. This piece argues the opposite: the refusal to answer is the more credible governance signal, and Doan Nguyen Duc's call only deserves weight once you check one follow-up question.

Four answers from four AGM stages

On the morning of April 21 at the Hoa Phat AGM, chairman Tran Dinh Long delivered what has become his standing posture: "As long as I sit in this seat, I will never advise shareholders to buy Hoa Phat stock."Investify

The same day at the PAN Group AGM, Nguyen Duy Hung — who also chairs SSI — was equally brief: "Just like Mr. Long, I won't tell anyone to buy PAN stock."Investify On the morning of April 22 at the Vinamilk AGM, CEO Mai Kieu Lien answered a shareholder who complained about holding VNM for ten years and only breaking even: "A buy or sell recommendation is the last thing I should give. That is each person's own freedom."CafeF

Three leaders, three unrelated sectors (steel, agri–food, dairy), all market-cap heavyweights — VNM at VND 129,800 billion and HPG at VND 216,100 billion on the April 23 session — and the same answer. That is not coincidence.

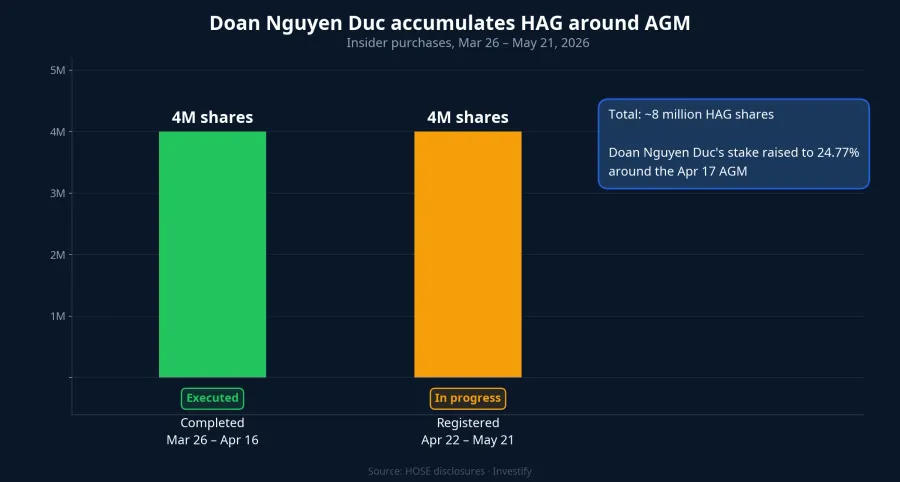

Five days earlier, on April 17 at the Hoang Anh Gia Lai AGM, Doan Nguyen Duc — known locally as "bau Duc" — chose the opposite path. He told shareholders directly: "If you buy HAG stock and lose money after one or two years, come find me and yell at me."Investify Some news reports added the line "Whoever has money, buy the way I'm buying."

Why "silence" is the standard, not evasion

You can think of it simply: a listed-company CEO should not advise shareholders to buy or sell their own stock. The answers from Mr. Long, Mr. Hung and Ms. Lien are not evasion — they are the governance standard that Berkshire Hathaway, Apple and Microsoft have held for the past twenty years. Three concrete reasons explain why.

First, legal exposure. Vietnam's 2019 Securities Law and Decree 155/2020 classify the use of public statements to influence a stock's supply and demand as a price-manipulation risk, especially when the speaker is a major insider.Investify A chairman issuing a buy or sell call from the AGM stage — where the press, analysts and shareholders all take notes — is creating deliberate price pressure. The more senior the insider, the stronger the duty to abstain.

Second, the ethics of shareholder relations. Shareholders arrive at an AGM with very different risk appetites and time horizons. A casual "you should buy more" can push someone near retirement into an oversized position; a "maybe consider selling" can knock a young investor out of a long-term holding that was actually well-suited. The CEO does not — and has no right to — know each attendee's portfolio. Giving a single recommendation to a mixed crowd is giving advice to the wrong address.

Third, CEOs do not know tomorrow's price. A CEO knows their own factory capacity, product pipeline and key personnel. But tomorrow's share price also depends on macro liquidity, relative valuation and market sentiment — variables no CEO controls. Saying "you should buy" asserts something the speaker cannot be sure of, or worse, leverages an information advantage to push one side of a trade.

Seen this way, "I won't recommend" is not the CEO ducking responsibility — it is the CEO fulfilling it: answering questions within their knowledge, and saying no to questions outside it.

Why Doan Nguyen Duc is the exception — and how to read it

Apply the three reasons above to HAG and the call sounds like it violates the standard. But put it in context and the signal structure inverts — and how it inverts is the part worth studying.

HAG has just closed a multi-year debt restructuring cycle. Doan Nguyen Duc did not only speak. He completed the purchase of 4 million HAG shares between March 26 and April 16, raising his stake to 24.77% — right before the AGM. Just after the AGM, he filed to acquire another 4 million shares over April 22 – May 21.Investify Roughly 8 million HAG shares, absorbed by the founder himself over about two months around the AGM.

HAG closed at VND 16,400 per share on April 22 — putting those 8 million shares at a tangible value, not a cheap promise. This is skin in the game in its original sense: the leader puts personal wealth on the line, sharing the downside with minority shareholders if the price moves against them.

Here is the structural difference. Mr. Long, Mr. Hung and Ms. Lien sit atop mature companies with long track records and deep institutional ownership; they do not need to manufacture stock appeal. Doan Nguyen Duc sits atop a company that has just emerged from years of eroded trust, where rebuilding credibility is genuine business work, not PR theatre. When he pairs "yell at me if you lose" with 4 + 4 million real share purchases, his words and actions point in the same direction.

This does not mean HAG shareholders should follow him in. A stock fresh out of restructuring carries a very different business-model risk profile from a 30-year blue chip. It means his call has internal consistency between word and deed. Whether that consistency fits your own time horizon and risk appetite is a question only you can answer.

A reading framework for retail investors at AGMs

From these four answers, retail investors can carry two default rules into AGM season.

When a leader refuses to recommend, treat it as the governance standard — not evasion. The next question worth asking is not price but operations: gross margin direction, working-capital turnover, the 12–24-month project pipeline, debt structure, dividend plans. These are things leaders actually know and are allowed to answer — and these are what determine the company's intrinsic value over the medium term.

When a leader calls for buying, ask three questions before deciding anything. (1) Is the leader buying alongside — at what size and price? — insider filings on the HOSE/HNX disclosure portal will tell you. (2) Why does the company need to rebuild trust right now? — just out of restructuring, a change in major shareholders, a recent price shock, or preparing a capital raise? (3) If action does not match words, the words are PR. A commitment without personal skin is a cheap commitment — and the market usually prices cheap commitments correctly.

These two rules do not replace your own judgment on valuation, sector and risk appetite. What they do is keep you from letting an AGM answer — whether a dry refusal or an impassioned call — push you into a trade your financial statements and prospectus do not yet support.

The 2026 AGM season still has many sessions ahead. Next time you hear a CEO answer the question "where is the stock price going?", listen to what they don't say as carefully as to what they do. That is usually the clearest governance signal on the stage — and often the most trustworthy one.