A securities firm can earn more interest from margin lending and still report a sharp profit decline. VIX Securities did exactly that in the second quarter of 2026: lending income improved, while its proprietary portfolio moved enough to pull net profit down to nearly VND 76 billion, a 94% year-on-year decline. Operating revenue also fell 32% to nearly VND 1,349 billion.VietnamBiz

The central point is not that margin lending failed. It was a growing income stream. The issue was scale and accounting timing: movements in a much larger proprietary book outweighed that steady improvement. For newer investors, the quarter offers a basic lesson in financial statements: a healthy revenue line does not, by itself, establish the quality of overall earnings.

The break came in the portfolio's net result

Financial assets recognised through profit or loss are updated to fair value at each reporting date. A rise in market value produces a revaluation gain; a fall versus the previously recorded carrying value produces a revaluation loss, even when the security has not been sold. That accounting treatment makes a securities firm's earnings more sensitive to market prices when it carries a large investment book.

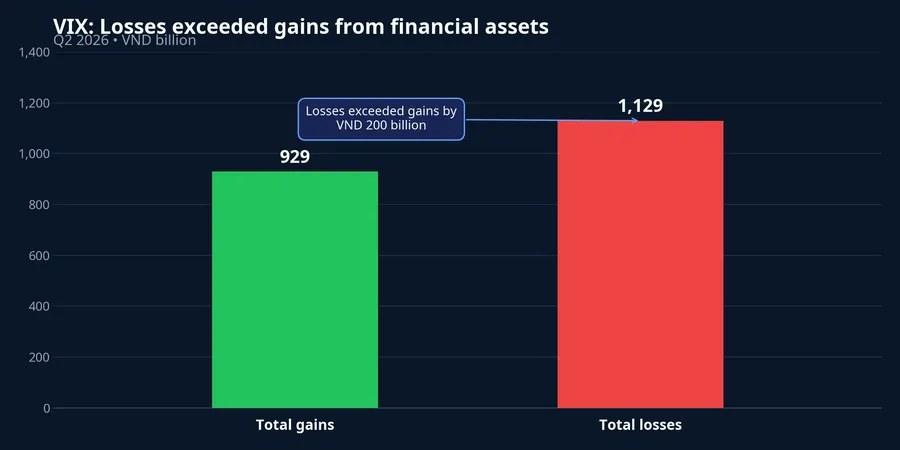

In the second quarter, VIX recorded VND 929 billion of gains from this asset group, down 45% year on year. The figure included nearly VND 176 billion from asset sales and about VND 653 billion of revaluation gains. Total losses on financial assets, however, reached VND 1,129 billion, more than four times the prior-year level, including approximately VND 1,090 billion of revaluation losses.VietnamBiz

That is why the gain and loss lines have to be read together. Netting them puts the financial-asset result at an approximately VND 200 billion loss in Q2 2026, compared with an approximately VND 1,435 billion gain a year earlier. The reversal worsened the pre-expense result by roughly VND 1,635 billion, far more than the improvement delivered by lending.Nhà Đầu Tư

The chart captures the point that a quick read can miss. VND 929 billion of gains is substantial, but it is not the final result of proprietary trading. Once losses exceed gains by VND 200 billion, the portfolio is reducing quarterly earnings. “Gains on financial assets” and “a positive proprietary contribution” are therefore very different conclusions.

Margin grew, but it was not large enough to offset volatility

Interest from loans and receivables was nearly VND 348 billion, up 62% year on year. Against roughly VND 214 billion in Q2 2025, the incremental revenue was about VND 134 billion.VietnamBiz Nhà Đầu Tư That is a constructive signal for lending income during the quarter, but it should not be treated as comparable in size to the VND 1,635 billion deterioration in the net financial-asset result.

The scale comparison avoids a common mistake. The additional lending income was only about one-twelfth of the decline in net financial-asset performance. Margin revenue normally accumulates with loan balances, interest rates and days outstanding. A single revaluation period, by contrast, can bring a meaningful change in a large portfolio's market value directly into reported earnings.

It is equally important to separate revenue earned during a period from the balance outstanding on the reporting date. At 30 June 2026, VIX loans and receivables stood at VND 13,958 billion, down VND 1,422 billion from the start of the year.Nhà Đầu Tư Higher interest income does not automatically mean that the end-period loan book expanded. One figure covers the whole quarter; the other is a snapshot. Together, they describe how margin lending generated income and how much capital was deployed at quarter-end.

A quarterly revaluation loss does not mean the whole book is underwater

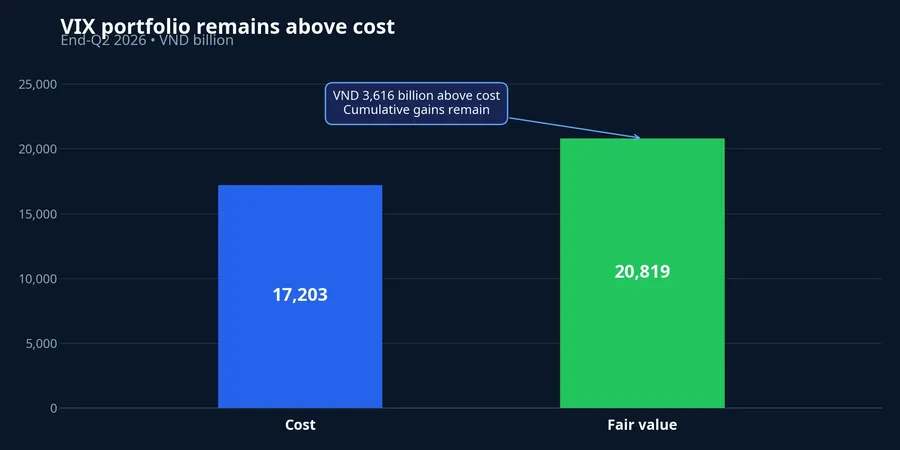

This is the part that calls for the most restraint. A revaluation loss in a quarter says that portfolio value fell from a previous carrying mark. It does not automatically mean every investment is below original cost. At the end of Q2, VIX reported VND 17,203 billion of cost and VND 20,819 billion of fair value for financial assets recognised through profit or loss.Nhà Đầu Tư

The VND 3,616 billion positive difference means the disclosed portfolio remained above cost at 30 June. Listed equities were about VND 2,218 billion above cost, while entrusted investments retained approximately VND 1,403 billion of unrealised gains.Nhà Đầu Tư Put simply, VIX gave back part of a previously recognised profit cushion during the quarter. The report does not support the conclusion that the entire portfolio had moved into loss.

Those statements can both be true. A portfolio can remain above cumulative cost and still fall enough in one quarter to generate a material revaluation loss. The filing does not disclose a complete holding-by-holding breakdown, so there is insufficient evidence to assign the move to one stock or claim a single driver. Market prices, portfolio mix and asset sales during the period could all have affected the result.

Earnings quality remains tied to the market

For the first half, VIX posted VND 214 billion of net profit, down 87% year on year. That represented approximately 7.6% of its roughly VND 2,800 billion net-profit target for 2026.VietnamBiz The pressure is not merely a target number. The remainder of the year requires a more stable proprietary result, materially higher income elsewhere, or both.

VIX raised charter capital from VND 15,314 billion to VND 24,502 billion, taking end-quarter equity to VND 32,695 billion.Nhà Đầu Tư More capital can support lending and investment capacity, but it does not create profit on its own. The eventual outcome still depends on capital allocation and the prices of the assets held.

The Q2 conclusion is straightforward: margin lending is a revenue buffer, not yet a pillar large enough to detach VIX earnings from proprietary-market volatility. That thesis changes only if the portfolio's net result becomes more stable in coming quarters, or if lending income grows large enough to absorb revaluation swings. The three indicators worth watching are total financial-asset gains and losses, end-period lending balances, and the return generated by the new capital.