A mother and daughter took a 6.8-ly diamond ring to a store for a scheduled resale appointment, only to find the shutter down. VTC News reported the incident at Hoàng Thứ Jewelry in Ho Chi Minh City on July 18; other large jewellery and gem stores remained open, so it does not establish that all diamond trading has seized up. It does, however, put a practical question in front of any buyer: when cash is needed, who is actually going to pay for the stone?VTC News

The simple answer is that an intact stone and a complete invoice are not the same as liquidity. Converting the ring into cash depends on substitute buyers, the price they will accept, and when they will settle. If all three depend on one retailer, the purchase carries not only the characteristics of the stone but also the counterparty risk of the store.

A buyback promise is not a market

Liquidity does not mean that a seller once promised to buy an item back. A liquid asset has several independent buyers, a reasonably intelligible way to establish price, and a process that can close within the owner’s required time frame. Gold bars and listed shares carry price risk too, but their holders generally have more trading venues or more counterparties.

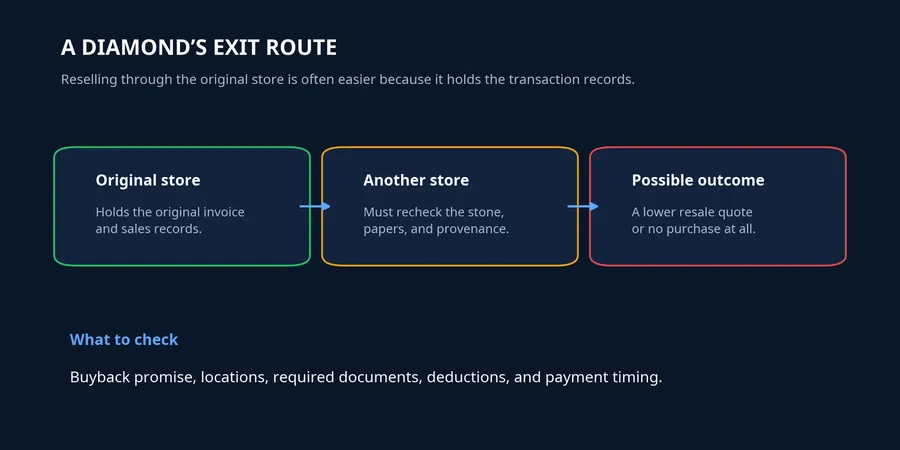

Retail diamonds in Vietnam work differently. Thanh Niên, citing the Ho Chi Minh City Fine Arts and Jewellery Association, reported that the wide variation in individual stones leads many businesses to buy back only products they originally sold. That design makes resale materially dependent on the original store, rather than on a secondary market with a common price.Thanh Niên

The reason is straightforward. A different store must inspect the papers, current condition, identifying characteristics, and provenance of the stone, then decide whether it can sell the item on. The original store has the invoice and transaction record; a third party must repeat that work and assume the risk of incomplete information. Its response may therefore be a lower quote or no offer at all, even when the diamond itself has not changed.

That does not mean every retailer rejects outside items or that every diamond has the same resale difficulty. Quality, documentation, brand, size, and current demand can all change the outcome. But when the resale route narrows to one address, that is a measurable counterparty risk, not a minor administrative detail.

This is also why a marketing phrase such as “buyback available” needs to be read as a contract term, not as evidence of a deep market. The useful questions are practical: which legal entity is obligated to buy, which branches can process the item, what documents are mandatory, what deductions apply, and whether payment follows immediately after inspection. A promise with narrow conditions can still be useful, but it should be valued for exactly what it is: one potential outlet, rather than an automatic right to cash.

When sellers outnumber buyers

The dependency can stay hidden while new customer demand is healthy. Inventory turns over and incoming cash helps stores handle exchanges and buybacks. Pressure becomes visible when many customers want to sell, while new buyers become scarce and previously repurchased stones cannot be turned back into cash quickly.

PJA said that resale demand accounted for more than 90% of its transactions and that exchanges had nearly stalled before it announced it would cease operations because of liquidity problems. This was a company disclosure, not a market-wide diamond statistic. Still, it captures the weakness in a buyback pledge: the promise works only while the promisor has funds and remains in operation.CafeF

Two prices need to be separated here. The invoice price is what was paid in a new purchase. The cash-realisation price appears only when someone agrees to buy at the time the owner needs to sell. The gap between them is the cost of exit, and it can widen as the number of substitute buyers falls.

Thanh Niên reported cases in which buyers offered 30–40% below invoice price for goods from closed stores. Another customer described contractual reductions of 20–30% for resale and 10–20% for an exchange. These are reported individual cases, not an average discount for the market; their value is in illustrating how deductions can differ sharply by terms, store, and circumstance.Thanh Niên

One brand publishes buyback rates of 85% or 90% of invoice price, depending on size, for intact natural diamonds with complete documentation. The conditions still determine the result: an item without certification, with damage, or in an excluded category may face deeper deductions or be rejected. A rate displayed in a policy is therefore not a guaranteed cash amount in every case.CafeBiz

A grading report identifies the stone, not the buyer

A grading report is still important. GIA explains that its reports describe characteristics such as colour, clarity, cut, carat weight, identifying features, and known treatments. That gives a potential buyer a basis for assessing the stone rather than relying solely on the seller’s description.GIA

But GIA also makes clear that a grading report is not an appraisal and does not state a monetary value. Put plainly, it answers “what stone is this?” rather than fully answering “who will buy it today?” or “how long until payment arrives?” Treating good documentation as a guarantee of liquidity conflates those separate questions.GIA

It helps to distinguish the advertised price, the contractual buyback price, and the realised cash price. The advertised price serves a new retail sale. The contractual amount can depend on the invoice, condition, holding period, and eligible locations. The realised price is what a specific buyer will pay, so it is directly exposed to demand and to that buyer’s available cash.

For a first-time buyer, the distinction changes how the purchase should be budgeted. A diamond can be meaningful as jewellery, a gift, or a long-held personal asset. It becomes a liquidity problem only when money needed for regular expenses or an emergency fund has been placed into an item whose sale depends on a single buyer. The point is not to dismiss the product; it is to avoid assigning it the same cash-access role as a deposit or a readily traded asset.

Check the exit before the purchase

For a purchase that may need to be held for years, do not ask only whether the stone is attractive or certified. Ask the seller, in writing, which entity must buy it back, where the policy applies, whether it uses invoice or market price, and how long payment takes after inspection. Those answers say more than a broad claim that the item “holds value.”

Keep the invoice, warranty card, and original papers, and verify the grading-report number through the issuer’s system. It is also reasonable to ask an independent retailer whether it would inspect or buy the product. If the original store is consistently the only possible buyer, the exit options are narrow.

One useful test is to request a same-day buyback quote before deciding to purchase. The aim is not necessarily to negotiate then, but to see the distance between a new-sale price and the cash that could be recovered. Money allocated to diamonds should be treated as long-term capital only if waiting to sell would not affect essential spending or an emergency fund.

The conclusion is not that every diamond is impossible to resell. The more accurate conclusion is that retail diamonds do not become liquid merely because they have a grading report or a buyback policy. The signals worth monitoring are the number of alternative buyers, the conditions for acceptance, and the time to payment. When all three rely on one retailer, counterparty risk is part of the stone’s effective price.