The syndicated credit agreement for the HCMC-Trung Luong-My Thuan expressway expansion was signed on July 16. For an infrastructure project, a signing ceremony does not create revenue overnight. It does, however, clarify the route capital must take: banks make credit available, the project company meets disbursement conditions, and borrowed money is turned into completed construction work.Báo Đồng Tháp

That is the useful starting point for reading the CII story. The VND 27,094 billion facility makes project funding more certain, but it is not debt already sitting in full on CII's balance sheet, nor is it proof that profit will rise immediately. The proposition is straightforward: the agreement will be tested first by whether disbursement tracks construction, and later by whether the completed road can generate toll cash flow.

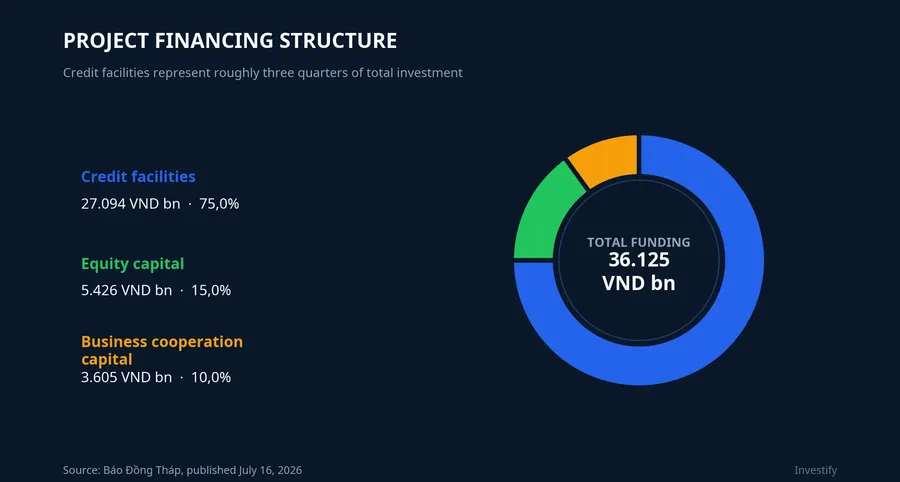

The project funding mix

The announced project cost is VND 36,125 billion, with no state-budget funding. Credit facilities account for VND 27,094 billion, equity capital for VND 5,426 billion, and business cooperation capital for VND 3,605 billion. That is roughly a 75%, 15% and 10% split, respectively.Báo Đồng Tháp

For a new investor, these are three different pockets of money. Equity is the capital that investors must contribute under their commitments. Business cooperation capital is money supplied under a cooperation agreement; it should not be treated as the project's charter capital. Credit, meanwhile, must be repaid with principal and interest. A large approved facility says that a funding framework exists. It says little by itself about project quality. The funding mix also shapes the order in which risk appears: equity and cooperation capital must be available before, or alongside, bank funding, while interest costs begin to accumulate once borrowing is drawn.

That distinction is why the VND 27,094 billion should not simply be added to CII's existing debt. CII's disclosure identifies BOT Sai Gon-My Thuan Expressway Co., Ltd. as the borrower for the construction investment, while the facility is the maximum amount under a borrowing plan approved by CII's board.CII It becomes recorded debt only as funds are drawn under the contract's conditions.

Borrower, controlling shareholder and obligations

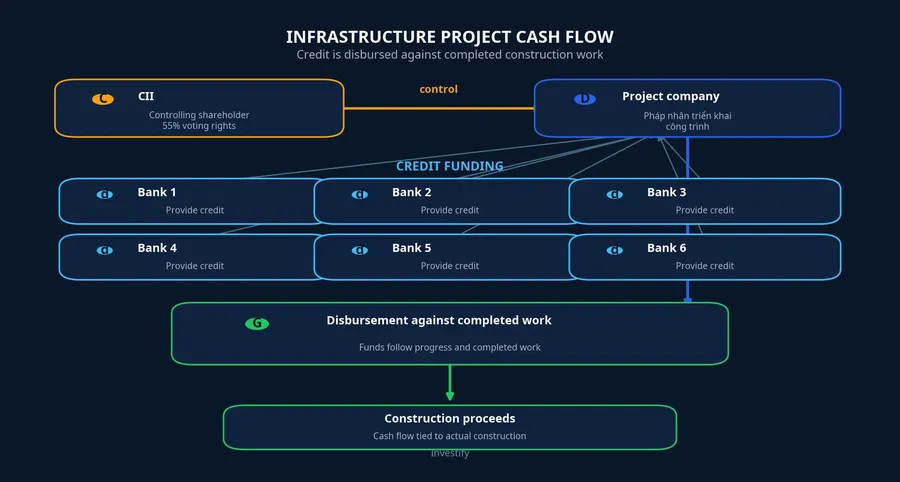

CII holds 55% of voting rights in the project company.Thị trường Hàng hóa The project's performance therefore matters directly to CII shareholders. Yet ownership does not answer every liability question. The project company is the legal borrower; CII is the controlling shareholder and may be affected through operating results, equity commitments, or guarantees if those commitments are disclosed.

Publicly available disclosures do not yet set out the interest rate, tenor, repayment schedule, collateral, or the scope of any CII guarantee for this facility. That gap means the facility size alone cannot establish that CII has assumed all of the project's obligations. When disbursement begins to appear in financial statements, investors should read the notes for debt, collateral and off-balance-sheet commitments. Those disclosures determine whether risk remains contained at the project company or extends to CII.

The cash-flow map illustrates the central point: funds do not move directly into CII and become shareholder value at once. Credit is extended to the project company and is meant to be disbursed against work volume and progress. If equity arrives as committed and borrowing follows completed work, project assets and debt are built in tandem. That is the expected structure for a large BOT project. It is why a quarterly statement is more informative than the headline facility: it can show whether debt growth is matched by construction-in-progress and whether funding costs are proportionate to the stage of the build.

New financing beside an existing debt base

As of March 31, 2026, CII reported VND 21,702 billion in borrowings and finance lease liabilities, including VND 4,808 billion short term and VND 16,894 billion long term.Thị trường Hàng hóa The project company's new facility exceeds that figure, but the two data points measure different states: one is debt already recognised, the other is a ceiling to be drawn over time. The comparison conveys project scale; it is not an arithmetic measure of CII's debt today.

The existing financial position still makes execution speed important. CII's first-quarter borrowing costs were VND 342 billion, up 14.6% year on year, while net operating cash flow was negative VND 243 billion for the same period.Thị trường Hàng hóaPhụ nữ Việt Nam These figures do not demonstrate that the new project will be ineffective. They do make funding costs worth watching while the construction has not yet added toll revenue. The relevant question is not whether leverage rises in isolation, but whether the new borrowing is producing a usable asset on schedule.

The construction site tests the quality of borrowed capital

At the signing date, the project already had physical activity: nearly 1,100 workers, more than 400 pieces of equipment and 67 construction fronts, with work output of approximately VND 1,500 billion.Báo Đồng Tháp That is constructive because disbursement against work volume matters only when there is completed work eligible for acceptance. It separates project financing from a large number in a board resolution.

Disbursement conditions still need to be completed. The Ministry of Construction has required the project company to provide adequate equity, while banks are to fund according to work volume and schedule; site clearance and materials supply remain issues to resolve.Báo Đồng Tháp If construction slows, debt and funding costs may grow before the asset produces revenue. Conversely, steady progress links borrowing to an asset that is actually taking shape. Neither outcome should be assumed from the signing alone. Completion statistics, rather than the financing headline, will distinguish them.

The more than 96-kilometre route is scheduled for completion and operation in 2028.Mekong ASEAN Until then, the central issues are capital, construction cost and interest expense. Afterward, traffic volume, vehicle mix, toll rates, operating costs and debt-service timing will determine the pace of payback. The existing route has at times carried more than 60,000 vehicles a day, but a peak observation cannot replace an average-traffic forecast over the whole concession life.Báo Xây dựng

Conclusion: watch capital become an operating asset

The credit agreement is progress in arranging funding, not the final proof of investment effectiveness. The constructive case for CII strengthens only if disbursement follows construction volume, equity arrives on schedule and funding costs do not outrun asset formation. When these conditions move together, the facility becomes capacity to complete a road.

That view changes only with concrete evidence: disbursement rising without comparable construction output, site clearance or materials pushing back the schedule, or financial notes revealing guarantees beyond what the market currently knows. In coming disclosures, three areas deserve attention: construction progress and output, consolidated debt and borrowing costs, and newly disclosed collateral or guarantees. Those signals will show whether the VND 27,094 billion facility is building additional value or merely enlarging the balance sheet.