HOSE has announced that TCX, the listed stock of Techcom Securities, will become a VN30 constituent on 3 August. The event creates a clear timetable for index-tracking funds, but it does not create a promise about the share price. For new investors, the key is to separate three moments: when the market receives the news, when funds prepare their portfolios, and when the new index basket takes effect.

The central point is straightforward: TCX's entry into VN30 is a time-bound change in technical supply and demand, not a certificate that the stock will rise. Reading the mechanics correctly keeps investors from becoming anchored to a single forecast of fund buying and directs attention to the evidence that will actually emerge.

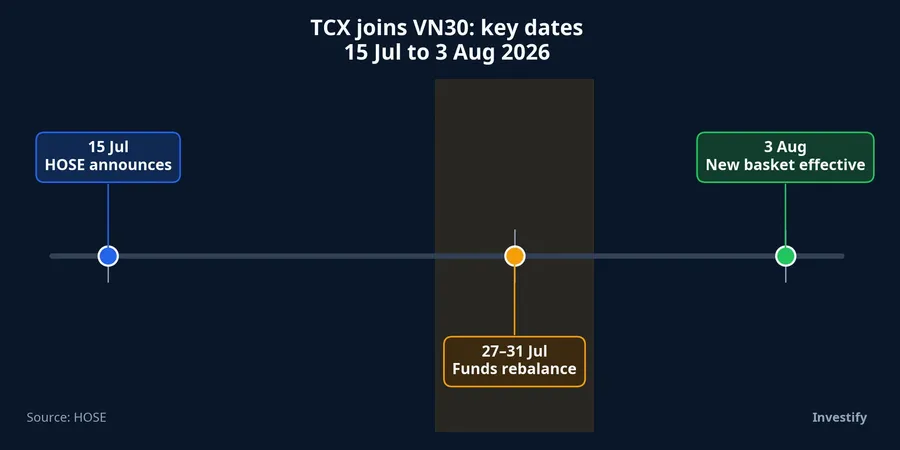

Three dates in one index event

On 15 July, HOSE announced TCX's addition to VN30. The new basket takes effect on 3 August. Those dates serve different purposes: the announcement tells the market what is coming, while the effective date is when the index begins to calculate with its new constituents.Báo Đầu tư

Between them sits the portfolio-rebalancing period. A report on the review schedule expects tracking funds to adjust portfolios from 27 to 31 July, ahead of the new basket taking effect.VnEconomy That is a window to watch, not a promise that every fund will trade at once or buy at one fixed price.

Think of VN30 as a published recipe. On 15 July, the recipe changes. Toward the end of the month, fund managers begin adjusting ingredients. By 3 August, their holdings need to be close enough to the new recipe that performance does not stray too far from the benchmark.

Tracking funds buy rules, not a corporate narrative

An ETF that tracks VN30 does not buy TCX because it has suddenly changed its view of Techcom Securities' prospects. Its job is to keep the portfolio close to the index. When a new name enters the basket, the fund needs to add it while adjusting other positions so that the entire portfolio moves toward the new weights.

That is why the phrase “funds will buy” can be misleading. A fund may split orders to manage transaction costs, cash balances, or subscriptions and redemptions in its own fund certificates. Buying too quickly can push up the stock and make tracking less efficient. Moving too slowly can increase the gap with the index once the new basket is in force.

The closing auction immediately before the effective date therefore attracts attention, but it should not be treated as the only possible outcome. Funds differ in assets under management, trading methods, outstanding certificates and cash balances. Actual transactions can be spread across sessions, especially when market liquidity permits it.

Large market value does not reveal the purchase size

TCX's average market capitalisation as of 30 June was VND 116,532 billion, placing it among the 20 largest companies on HOSE.Báo Đầu tư That explains why the stock has the scale to appear in the basket. It does not support a shortcut of multiplying market value by a fund's size to infer the amount a fund must buy.

Index weights are neither evenly divided among companies nor calculated by simply taking all listed market capitalisation. They also reflect free-float shares and weight limits. Each fund's required purchase then depends on TCX's market price at the time, its assets under management, the number of outstanding certificates and flows into or out of the fund.

That is why different pre-event forecasts can produce different figures without either necessarily being wrong. Their assumptions differ: which price they use, the date of the fund-size estimate, and the assumed free-float ratio. Before official weights and each fund's updated portfolio are available, any purchase estimate should be read as conditional, not as an order waiting in the market.

Price and liquidity need to be read together

On 15 July, TCX closed at VND 42,100 per share, up 0.36%, on trading volume of 1,935,700 shares. That was only a modest uptick, not a breakout. More importantly, it shows that inclusion news does not automatically produce a strong price gain on the announcement day.

Over the five sessions through 15 July, TCX averaged approximately 2,029,511 shares traded per session. Volume on 15 July was below that baseline. This is a useful reference for the rebalancing week: rather than watching only the board's red or green colour, compare shares matched with TCX's own normal level of trading.

A session with much higher liquidity but no price advance may show supply absorbing demand. Conversely, a quick price rise without a corresponding expansion in volume is not enough to conclude that index-fund money has arrived in force. This is not a formula for predicting direction. It is a way to avoid assigning one cause to a move that can also reflect the wider market, existing expectations and sellers.

The same news can still lead to different price paths

TCX closed at VND 45,000 on 3 July before falling to VND 42,100 on 15 July, a decline of approximately 6.44%. That sequence does not prove that VN30 inclusion is negative. It simply puts a necessary limit on a common inference: index news is one variable, not the whole explanation for price.

At least three outcomes are plausible during the rebalancing window. Expectations of fund buying may already have been reflected in the price before the announcement. Existing holders may take profits once the news becomes fact. Or tracking demand may appear but be matched by available supply. Current data are insufficient to apportion the contribution of each explanation, so attributing every move to ETFs would go beyond the evidence.

A compact checklist for new investors

First, follow the official weight applied by the index and by each fund. The weight indicates the technical demand to replicate the index; market capitalisation alone cannot do that. Next, compare trading volume from 27 to 31 July with recent averages, and watch the price reaction rather than building a conclusion from one isolated session.

Finally, keep the event in sequence. The 15 July announcement delivered information. The late-July window is when portfolios are adjusted. The new composition takes effect on 3 August. Those three points let investors read price action through a timetable instead of a sense of urgency.

TCX's VN30 entry raises its presence in index-tracking flows, and that is real. The stronger conclusion, that the price must rise because funds buy, is not guaranteed by the evidence available now. Until the effective date, the signals worth monitoring are the applied weight, liquidity against its baseline and the price response as trading occurs. Only by reading all three together can investors see how technical demand is being absorbed by the market.