REE has completed close to half of its full-year profit plan after six months. That is a constructive starting point, not a guarantee for the year. Estimated net revenue was about VND 4,900 billion, up 7% year on year, while net profit reached VND 1,398 billion, up 13%. Profit growing faster than revenue is a positive signal on business mix, but the third-quarter report will be the direct test of the remaining path.Người Quan Sát

The figures should also be read in their proper form: they are preliminary estimates shared by the company on July 10, not reviewed half-year financial statements. The more useful approach is therefore to track operating variables: power-segment efficiency, conversion of M&E contracts into revenue, and progress at the office and residential businesses. Those are the links that will determine the rest of the plan.

What profit outpacing revenue tells investors

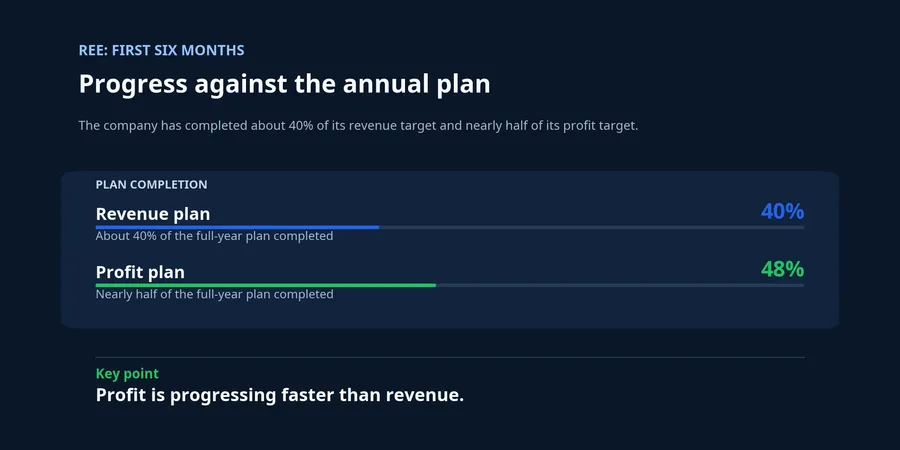

REE’s annual plan calls for VND 12,230 billion of revenue and VND 2,814 billion of net profit. The six-month result represents about 40% of the revenue target and nearly 50% of the profit target. The gap does not automatically mean margins will keep widening, but it does indicate that the first half was not simply a volume-driven revenue story.Người Quan Sát

For the remaining profit to reach the full-year accounts, REE must do more than maintain its existing operations. It needs to bring more M&E work through acceptance and keep the slower businesses from dragging on. This is more informative than looking only at the completion percentage, because identical completion ratios can be produced by very different operating quality.

Power is supporting results, but not in a straight line

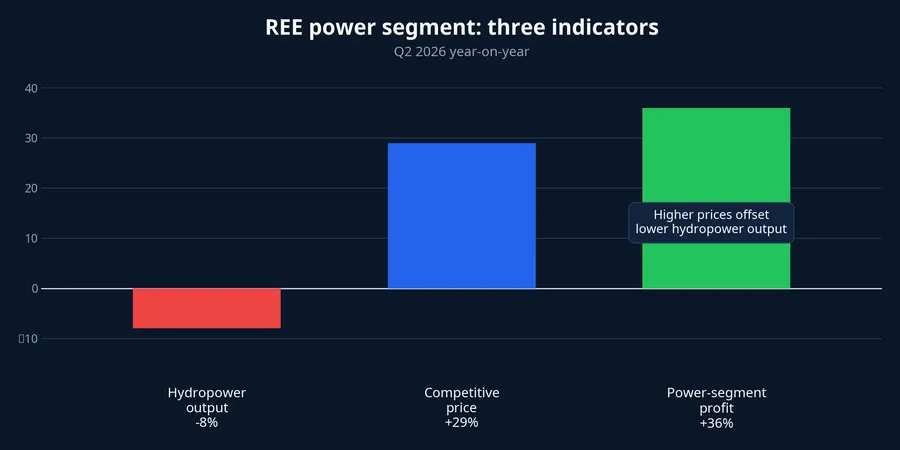

The second quarter shows why power is the key contributor. Power revenue rose 10% year on year and net profit from the segment increased 36%. Merchant hydropower output, however, fell by about 8%, while prices on the competitive power market rose by about 29%. The data suggest that better prices and the generation mix were able to offset part of the weaker hydropower volume.Người Quan Sát

That does not mean every following quarter will replicate a 36% profit increase. Hydropower output depends on hydrological conditions, and competitive-market prices can change. The more defensible reading is that the power portfolio can cushion the business when one operating metric weakens, not that every current condition can be assumed to persist.

Duyen Hai 1 has entered commercial operation and helped wind-power profit rise 15% year on year. This is an operating contribution, distinct from projects still awaiting their commissioning dates. Investors should keep that distinction clear: capacity already generating electricity and capacity targeted for operation do not offer the same degree of certainty for financial reporting.Người Quan Sát

New capacity is more of a base for next year

Duyen Hai 2 and Duyen Hai 3, two wind projects with combined capacity of about 128 MW, are targeted to begin commercial operation in the fourth quarter of 2026. The 30 MW Tra Khuc 2 hydropower project is also being completed. These facts matter for the scale of REE’s power portfolio, but a commissioning date does not mean all capacity contributes to an entire quarter.Người Quan Sát

Based on the company’s schedule, Tra Khuc 2’s units are expected to operate in late November 2026, December 2026 and early January 2027. Even if the timetable is met, the 2026 contribution may be limited to the initial period; the fuller benefit should come through in next year’s revenue base.VietnamBiz

This separates lower project risk from recorded profit. On-time commercial operation would be a positive operating signal, but generated output, selling prices, interest expense and recognition timing determine the earnings effect. The second-half question is not only whether more MW arrive, but whether those MW begin converting into cash flow.

M&E: a large order book is not revenue

The M&E segment presents another kind of signal. New contracts signed in the first half were worth about VND 5,900 billion, and work yet to be performed at the end of the second quarter was estimated at about VND 10,000 billion. That backlog provides visibility for subsequent activity, but it cannot be read as revenue or profit already earned.Người Quan Sát

In M&E, a contract must pass construction, acceptance and collection before it becomes revenue and cash flow. Project schedules, the volume accepted by clients and receivables discipline can all alter the recognition date. The contract figure is therefore useful evidence of workload, but the third-quarter report needs to answer a narrower question: how much of that workload has become an actual result?

It would be premature to assign all future profit movement to new contracts alone. Project execution, power pricing and the pace of the property recovery are parallel explanations that can affect consolidated earnings. The evidence is strongest on REE’s sizeable workload; the speed of conversion still requires confirmation in coming reports.

Offices and housing remain the offsetting gap

The existing office portfolio has average occupancy of about 90–92%, while e.town 6 is at about 58%. A newly completed building with lower occupancy does not erase revenue, but vacant space does not yet generate enough cash flow to absorb operating costs and depreciation as efficiently as a mature asset.Người Quan Sát

In housing, The Light Square has sold 8 of 45 units. That makes the timing of revenue recognition harder to forecast, particularly because property revenue is generally tied to delivery and recognition conditions. Water is a steadier offset: output in its operating areas reached nearly 240 million cubic metres in the first half, up about 7% year on year. Yet water cannot automatically cover a simultaneous slowdown in office leasing and housing, especially if power-project schedules slip.Người Quan SátVietnamBiz

Conclusion: a good base still needs to convert

The current thesis is that REE has delivered a positive six months, with better quality than a simple revenue increase because power and M&E have improved visibly. Hydrology, project timing, acceptance and occupancy are risks, but they do not reverse that view today. They would weaken it if the third-quarter report showed that power efficiency had not held, M&E workload was not becoming revenue, or new assets remained slower than expected.

For a new investor, the distinction is straightforward. A target, a signed contract and a project under construction are each useful leading indicators, but none is the same as booked revenue or cash generated. Reading the next report through that sequence helps separate operational delivery from expectation.

The next watch list is specific: power profit alongside output and selling prices, M&E revenue against backlog, occupancy at e.town 6, sales at The Light Square, and commercial-operation announcements for new projects. REE has a promising first half. The remainder of the plan will be established by operating milestones and real recognition, not by stated targets alone.