Dien May Xanh is approaching a new role beyond its familiar storefronts: a company with its own shares for the market to value. Its public offering has concluded and its public-company registration has been recorded, but DMX shares are not yet trading on HOSE. That distinction matters because recognition of the brand alone will not determine what the standalone business is worth once trading begins.

The central case is straightforward. DMX has a retail platform broad enough to be assessed as a multi-chain ecosystem, rather than merely an electronics retailer. Yet a credible standalone valuation still requires more evidence on earnings, debt and transactions with MWG. The available figures point to the right questions; they do not yet justify settling on a valuation.

A completed offering is not a trading debut

DMX distributed more than 166.4 million shares out of the planned 179.5 million in its initial public offering. Its charter capital consequently rose to VND 12,677.22 billion.ĐTCK That is a capital-raising milestone, not evidence that investors can already buy and sell the shares on HOSE.

On July 10, the State Securities Commission recorded that DMX had completed registration as a public company. Earlier, it announced a July 6 record date for the central securities-registration process at VSDC.DMX DMX Those steps prepare the way for custody and trading, while the listing decision and first trading date remain separate milestones.

DMX is planning to list on HOSE in August 2026.Znews “Planning” is the operative word. Until HOSE announces both its decision and the first trading date, the plan should not be treated as an accomplished event, and the offering price should not be used to infer post-listing liquidity or an equilibrium market price.

For an F0 investor, these labels describe different things. An offering raises capital; public-company status places the issuer within the disclosure framework; central registration allows securities to be recorded and settled; listing and the debut create an actual secondary market. Collapsing them into one “DMX is already on HOSE” story masks the remaining execution steps and can create false certainty about when a market price will be observable.

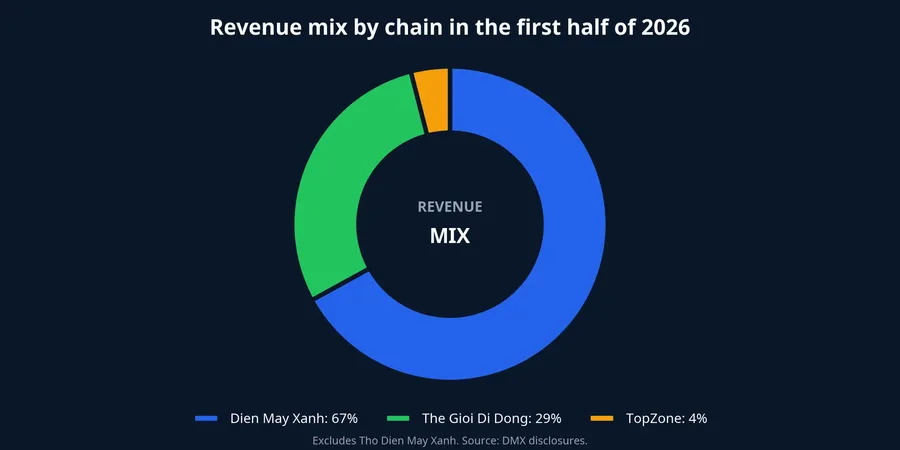

More than one retail engine

In an operating update released on July 10, DMX reported VND 65,279 billion in first-half 2026 consolidated revenue. That was a 31% increase on a comparable basis and represented 53% of its full-year revenue plan.DMX The important point is not just the growth rate: the number of domestic stores edged down from the start of the year while revenue rose, suggesting stronger productivity at existing locations.

The Dien May Xanh name may evoke televisions and refrigerators, but the DMX legal entity also operates The Gioi Di Dong, TopZone, Tho Dien May Xanh and EraBlue. In the chain-level revenue mix, Dien May Xanh accounted for 67%, The Gioi Di Dong for 29%, and TopZone for 4%; this excludes Tho Dien May Xanh.DMX Valuing DMX solely against electronics-retailing peers would therefore miss its handset and service businesses.

Consumer electronics contributed 43% of revenue, while information technology and telecommunications contributed 52%. Installment-purchase revenue increased 49% year on year and represented 38% of first-half revenue.DMX Put simply, consumer purchasing power and access to consumer finance are material inputs into DMX’s performance; this is not a business driven only by replacement demand for household appliances.

That breadth cuts both ways. A broad assortment can spread revenue risk when one category slows. But the importance of installment purchases also makes sales more sensitive to interest rates, loan-approval standards and consumer confidence. The report establishes that these factors coexist; it does not establish any one of them as the sole cause of growth.

Services and Indonesia need separate scrutiny

Tho Dien May Xanh generated VND 1,892 billion in revenue in the first half, up 47% year on year. Revenue from customers outside the ecosystem was VND 179 billion, or 10% of the segment’s revenue.DMX The after-sales operation has scale, but most of its current value is still serving the group’s own chains.

For investors, that distinction matters when assessing independent cash generation. Services can improve the customer experience and support merchandise sales, but they should not yet be treated as an external-revenue engine on a par with the core retail chains. Subsequent reports need to show whether the external-customer share is changing and what the segment contributes to profit.

EraBlue is DMX’s expansion arm in Indonesia. Its revenue rose 92% year on year in the first half, and it had 261 stores at period end.DMX Rapid growth signals expanding scale, but it does not automatically demonstrate that each store has reached a stable level of profitability. Investors should separate revenue added by new openings from productivity gains at mature stores.

Valuation must include the capital structure

As of March 31, DMX’s total debt was VND 22,158.89 billion, equal to 110.7% of equity. The revised use-of-proceeds plan prioritised repayment of bank debt.ĐTCK The offering therefore matters for more than charter capital: its practical effect should emerge in debt balances, interest expense and cash flow in subsequent reports.

A debt balance at one quarter-end cannot, by itself, settle the risk assessment. It must be read with inventory turnover, operating cash generation and borrowing maturities, details not fully available in the six-month revenue update. It would be premature to claim that the new capital has certainly repaired the entire financial structure before the next financial statements arrive.

This is where a financial-statement lens is more useful than a brand lens. Higher revenue can be valuable, but it does not automatically mean more cash is available to shareholders if inventory, receivables or financing needs grow at the same time. A second-quarter report can clarify whether the improvement in scale is translating into margins and cash conversion, or whether growth still requires a heavy balance-sheet commitment.

There is also the question of independence from MWG. A separate ticker does not mean the economic operations have fully separated from the parent. Related-party transactions, shared-cost allocation, dividend policy and minority-shareholder rights deserve close attention in disclosures because they determine which portion of profit truly belongs to DMX shareholders.

Conclusion: wait for evidence on the standalone business

DMX has notable operating evidence: growing first-half revenue, several business layers and an expanding market in Indonesia. But the evidence is not yet sufficient to lock in a standalone valuation. The appropriate framing is to wait for the listing decision, the first trading date and the second-quarter financial statements before reaching a conclusion on the quality of growth.

Three disclosures matter most: whether profit and margins keep pace with revenue; how far offering proceeds reduce debt and interest costs; and how transparently transactions with MWG are presented. These signals do not replace the brand. They are, however, what turn a familiar storefront into a comparable listed business.